5 Most Important Drivers Right Now

A timely framework reset for the return of volatility.

Dear readers,

“Something will break” can be the most tiring phrase to hear around financial markets. These three words are often muttered to describe the dynamic in which the central bank tightens policy to the point that broken financial plumbing and asset writedowns threaten a systemic calamity. It is then assumed that the central bank pivots within days or even hours to save the day. This premise carries heavy assumptions in two forms: 1) the financial system is inherently unstable and is prone to calamity, not just isolated problems, and 2) the Fed is a willing lender of last resort. Not only are each of these assumptions warranted, they should anchor any multi-asset investment framework. Today, we’ll outline five of the most important governing factors in today’s investment landscape to help you find direction in a fast-moving and hectic macroeconomic environment.

River is the Bitcoin exchange of choice for the long-term investor.

Securely buy Bitcoin at the tightest spreads in the industry, have peace of mind thanks to their 100% full-reserve cold storage custody, and enjoy zero fees on recurring orders. Need help? They have US-based phone support for all clients.

Invest in Bitcoin with confidence at River.com/TBL

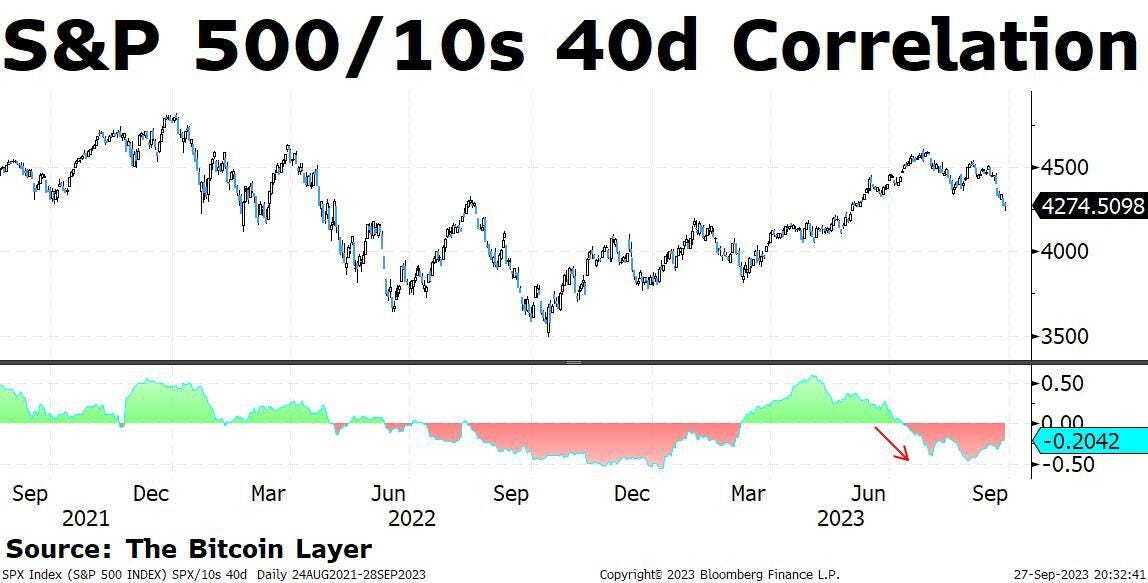

Where are we now?

Price action in risk markets as of late has been shaky, and late-day weakness as well as Friday weakness both demonstrate an unwillingness to warehouse risk by market participants at the moment. The S&P 500 is down 7% from the year’s highs, and its current drawdown has once again been driven by rising long-term yields. Remember that all of 2022 was characterized by rising yields which caused falling stocks—the past couple months have brought about an almost identical environment:

Before we talk about the driver (yields), failure at ~4,525 technically to us spelled doom, as market participants confirmed that the bullish countertrend of October 2022 until 4,600 this summer was a temporary bounce instead of the beginning of a new bull trend. The way in which equity markets traded over the past two weeks in particular does not inspire confidence, and in our opinion it quite emboldens the bears who now are in the driver’s seat and ready to capitalize on dismal sentiment.

On sentiment, we all know that the reason stocks are falling is rising Treasury yields. We’ll discuss what is moving yields higher shortly, but a break of 4.35% unleashed a wave of selling that might not conclude until a body bag is taken out. BTFP, the Fed’s relatively new facility which lets banks post Treasuries as par collateral even if impaired, might stop banks from writing down their books, but it doesn’t prevent losses elsewhere in the system:

This emergency mechanism is papering over only a fraction of the $1.5 trillion in mark-to-market losses on Treasury securities, but we bring bad news: the losses you see in the above chart don’t even begin to cover the losses elsewhere in fixed income, as corporate bonds and mortgage-backed securities suffer just as much from interest rate risk. Lastly, bring in the danger of leverage, and even a small move of 30 basis points higher in US Treasury 10-year yields can bring about the death of a market player.

Speaking of demise, somebody is getting absolutely bludgeoned in Treasuries and might not live to see another day. We have nothing on which to operate when it comes to a fund blowing up other than rumors and price action, but we can point you to recent worries from the Bank of International Settlements and other players in financial regulatory circles that the return of the great basis trade (arbitraging price differences between Treasury securities and Treasury futures contracts) is bringing a great danger to financial stability:

Contract data is lagging, so we don’t have evidence of any trade unwinds until next week, but it is worth watching this trade, which allegedly was a primary contributor to the September 2019 repo crisis. Don’t let the relatively small moves fool you—a half-percent increase in long-term Treasury yields in one month is a recipe for disaster. To use the most worn-out parable we know: something is breaking.

5 drivers in today’s market

How many different moving parts do we have to balance to understand today’s predicament? In our humble opinion, any answer other than “dozens and dozens” would be presumptuous—you’ll see that we aren’t including anything to do with China and its outsized impact on the global economy, Japan and its stockpile of US Treasuries as a tool to fight currency devaluation, or oil markets and associated geopolitics. What we present instead is a set of the main operating guidelines you must have to comprehend today’s moving parts. We are entering a more volatile regime than months past, so let’s go through the reasons why.