Bitcoin Sellers Exhaust Themselves As GBTC Outflows Slow: TBL Weekly #78

Welcome to TBL Weekly #78—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.

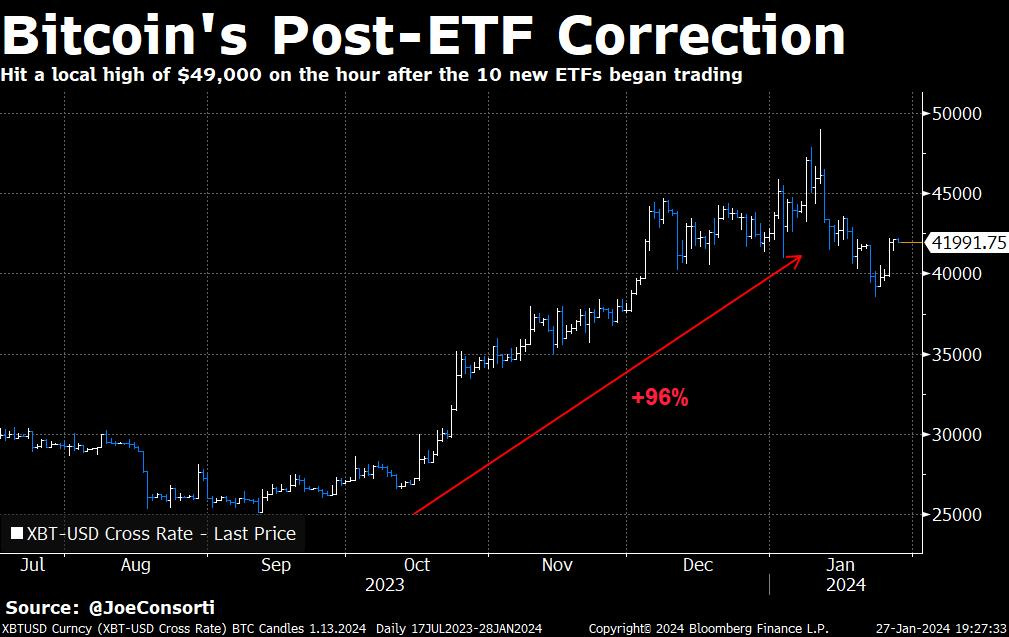

Bitcoin sellers have exhausted themselves, as its price has rebounded by $3,000 in a brief reprieve from its 5-figure fall from $49,000 over the last week. Bitcoin now sits at $42,000, and as Nik pointed out on Friday, its chart shows encouraging signs of an early bull market that started months ago:

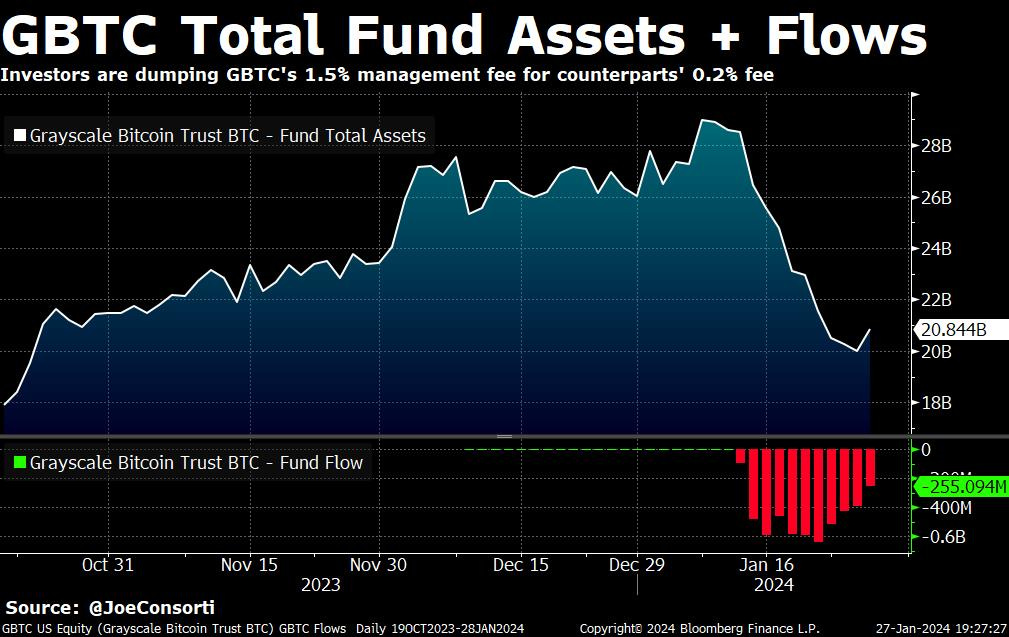

GBTC outflows are slowing down which has lent itself to bitcoin’s price rebound. Note the rounding bottom on net fund outflows in the bottom pane, declining from a high of more than $600 million in daily outflows to just $255 million on Friday. While we may not be at equilibrium for GBTC, where sellers and buyers negate one another and outflows stabilize, we have reached the point at which Grayscale’s bitcoin selling has been dwarfed by the market’s buying of spot BTC:

All 10 spot bitcoin ETFs have amassed $24 billion in trading volume since their collective launch. Ex-GBTC, $5.8 billion in funds has entered the 9 new spot bitcoin ETFs. These are encouraging early signs for the growth of a healthy and liquid market for these spot bitcoin-adjacent vehicles, and we expect the total AUM across all bitcoin ETFs to hit $50 billion this year:

The first estimate for Q4 GDP growth came in at 3.3%, beating expectations of 2.0% and slowing marginally from 4.9% in the prior period. Personal consumption also beat expectations and rose 2.8% in the first estimate for Q4. It is worth noting that GDP is not very forward-looking and doesn’t generally portend recession odds far in advance of one happening.

The Atlanta Fed’s GDPNow estimate for Q4 of 2024 now sits at 3%, up from the 2% estimate it started 2024 with:

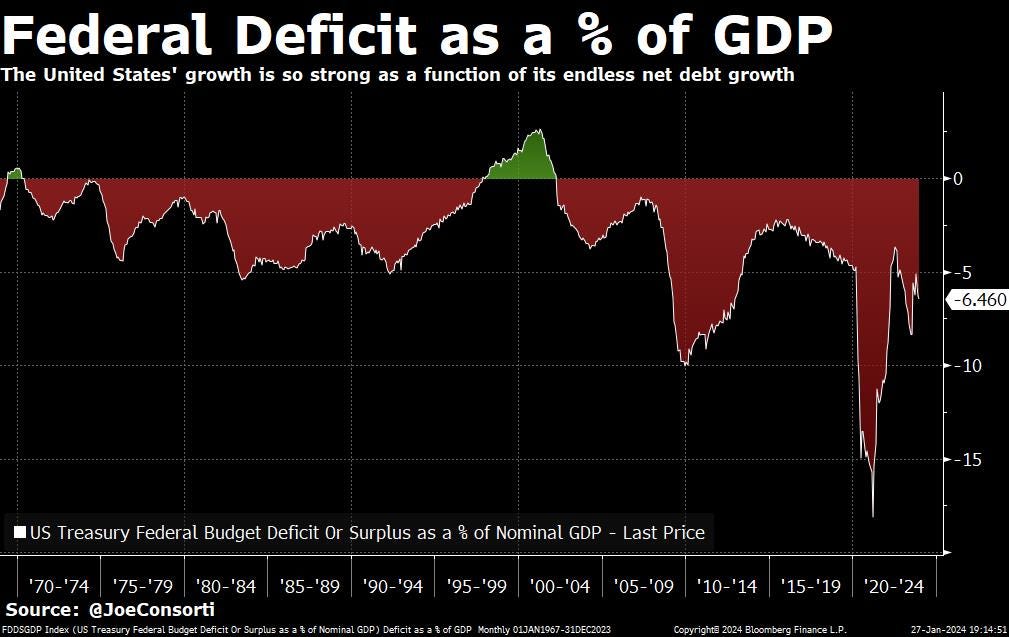

The economy is not just holding up, it is still booming by all accounts. Looking across consumers, credit, valuations, and asset prices—strength is the universal theme. There is a big asterisk to all of this. As GDP “beats” expectations and the economy flourishes from the outside looking in, we are increasingly dependent on evermore government debt to keep the machine chugging. The Federal deficit as a percentage of GDP widened to -6.46%. We have not had a period of positive real economic growth, above what we borrowed, since 2001:

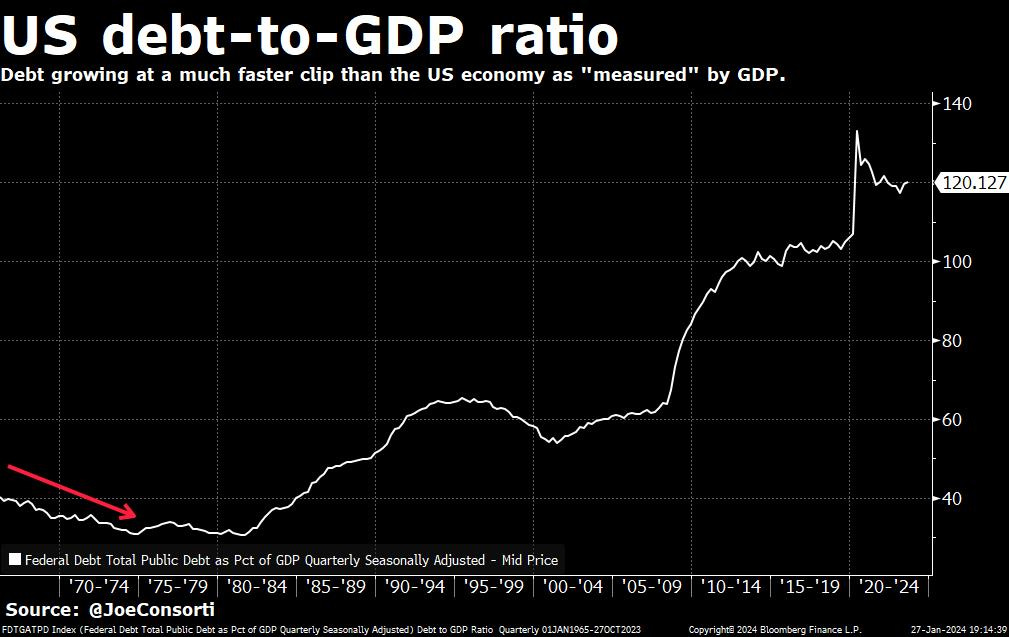

Note how reliant the US economy has become on perpetual public and private debt growth. After 2008 we don’t even have economic growth that exceeds our total debt load. Prioritizing GDP, a bad metric for economic prosperity that relies squarely on spending, has driven us to become wildly unproductive. As long as GDP growth is positive in nominal terms, we take on as much debt as we can, even with no intention of paying it down. To hell with real prosperity:

But as long as GDP stays positive in nominal terms so the US remains attractive on the stage of global trade, the synchronicity with which politicians and central bankers create and spend money won’t stop until the citizenry actually demands a change. And with the political landscape heating up headed into this year’s Presidential election, it is unlikely that either party address any of it. We are, however, watching the Texas situation closely and feel the charge of states standing up to the Feds.

Next Week

In the week ahead, we have an extraordinary amount of high-profile financial events, including the FOMC decision, Treasury’s quarterly refunding plans, monthly nonfarm payrolls, and ISM. We also have a QT day on the 31st, as Fed-owned securities mature. Friday’s letter and video covered some of the drama unfolding at the Fed/Treasury nexus, making every subsequent week an opportunity for further theatrics.

We continue to shed light on impressive economic numbers and all-time highs in stocks, all combining for some of the easiest financial conditions (expressed by implied volatility, repo stress, and other financial plumbing metrics) we have seen in three years. And herein lies the crux of the drama: money markets continue to price rate cuts, and the Fed already has us watching for QT adjustments at Wednesday’s FOMC. Why is there such a dichotomy? Credit markets are in incredible shape, with spreads screaming lower and issuance off the charts, but the Fed won’t move the market off a 1% rate cut this year. Perplexing, but our interpretation is that rates markets see a problem and are waiting for it to unfold, while risk markets are charging ahead as if there is no problem because at the moment none exists.

Back to the events of next week, both sides of the coin have their time to shine. The Treasury will announce increases to Treasury auction sizes, as well as the hit to money markets. How rates react to these sizes will be very indicative of the Treasury’s influence right now, which is seemingly at all-time highs given the consistent theme of fiscal dominance. We also have the Federal Reserve’s latest policy decision—another no-move meeting. The Fed has been on pause since its last rate hike in July 2023. It will be cutting rates by June 2024 and altering the pace of its QT program possibly by Wednesday. We are not exactly sure how terrified the Fed is about what will happen when RRP declines below $100 billion, but we’re getting the feeling that it must make a policy adjustment before something happens, in order to look less foolish when it does. In December, Powell bent the knee to the rates market. What surprise does he have for us on Wednesday, and how spooked is he by inflation trends that have fallen below his target?

From an economic data perspective, next week is a firecracker. Case-Shiller home prices, JOLTS job data, ISM, and unemployment all give the market tradeable prints, while our ultimate focus will be on ISM manufacturing data. ISM underpins our bearish read on the US economy, despite 3.3% GDP growth. The JOLTS jobs numbers, including openings, quits, and hires, are also a high-quality read on the labor market. Numbers of late have indicated a weakening number of overall job listings, alleviating wage pressures, which contributes to disinflation. Rising inflation was the cause of yield increases and rate hikes—the opposite is happening now, just not everybody sees it yet:

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are some quick links to all the TBL content you may have missed this week:

Monday

In this episode, we are joined by TBL Africa Correspondent Noelyne Sumba. Noelyne walks us through stages of bitcoin adoption in Kenya, Nigeria, and South Africa, citing a report that suggests Sub-Saharan Africa has one of the most active bitcoin user bases in the world. Finally, Noelyne shares with us her vision on how bitcoin is helping Africans fight back against corrupt governments and leaders.

Check out—PRO-BITCOIN Policies In Africa

Tuesday

Just 12 days ago on January 11th, 10 new spot bitcoin ETFs were launched. Among them was Grayscale, who wasn’t launching a product, but converting one with an almost decade-long track record under its belt and $28 billion in assets under management. Not two weeks later, the fund is $7 billion lighter.

Why? It decided to charge a 1.5% management fee, more than 100 basis points more expensive than its most expensive competitor. Additionally, its counterparts have waived their management fees for as long as a full year from launch. This has created immense selling pressure on bitcoin, as investors dump GBTC for lower-fee competitors and flee for cash after years under the thumb of an oppressive discount.

Why is Grayscale sitting idly by as a multi-billion dollar exodus from its largest fund is underway? That’s the operative question, indeed. Is this a game of high-level 4-D chess from Sonnenshein, or ritual suicide by woeful mismanagement and overestimation of investors caring about industry reputation?

Check out—Why Is GBTC Killing Itself?

Wednesday

In this episode, we are joined by Alex Thorn, head of research at Galaxy, to discuss how bitcoin ETFs work. Alex explains the mechanics of how and when ETF managers purchase and store bitcoin, why GBTC's high fees are clobbering its assets under management, and when he believes bitcoin ETFs will be on the menu for financial advisors.

Check out—How Bitcoin ETFs Work with Alex Thorn

Friday

A high-quality Swiss watch can have over 100 moving parts. Oftentimes, it can feel like the global economy has the movement of a complicated timepiece, with each individual part useless by itself, and those that can fully comprehend how every individual component interacts with the rest hard to come by. It lends to our overall approach here at The Bitcoin Layer—factor in as many moving parts as possible, knowing full well it still might not be enough to capture the panorama. Nevertheless, a week like this gives us so much to analyze that we feel like we are sitting next to the finest watchmakers in Geneva. We’ll start with the Fed, and end with why a bitcoin allocation has never been more important.

Check out—Imminent Yield Curve Uninversion

In this episode, Nik brings us a timely macroeconomic and financial markets update. Starting with the Fed's policy changes from the past couple weeks, we learn about the Treasury's battle with the Fed over monetary policy, how central bankers are planning for the next financial crisis, and what this all means for the investment case for bitcoin.

Check out—Central Bankers Planning For Next Crisis

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.