Credit stress ebbs, Fed pause rally is here, the downturn is just beginning: TBL Weekly #38

Welcome to TBL Weekly #38—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

Banking stress is falling for the time being

Total deposits at both small and large US commercial banks fell by $84 billion this week as the bank runs continue—falling $300 billion throughout March. Banks, who use deposits to create credit for consumers and businesses, have a lower proclivity to extend new credit as their deposits dry up—this credit destruction is a huge aid for slowing down inflation, and is no doubt helping the Fed achieve that:

This week we saw yet another huge inflow into money market funds, as investors leave bank accounts for the superior yield and safety in liquidity of MMFs. They saw ~$64 billion of inflows this week, totaling $304 billion in the past three weeks. This is a flight to safety:

Banks borrowed less from the Fed’s main emergency loan window this week, tapping the discount window for $88.1 billion, down $22 billion from last week. It is encouraging that banks are borrowing increasingly less from the discount window, but this is only one aspect of the funding picture:

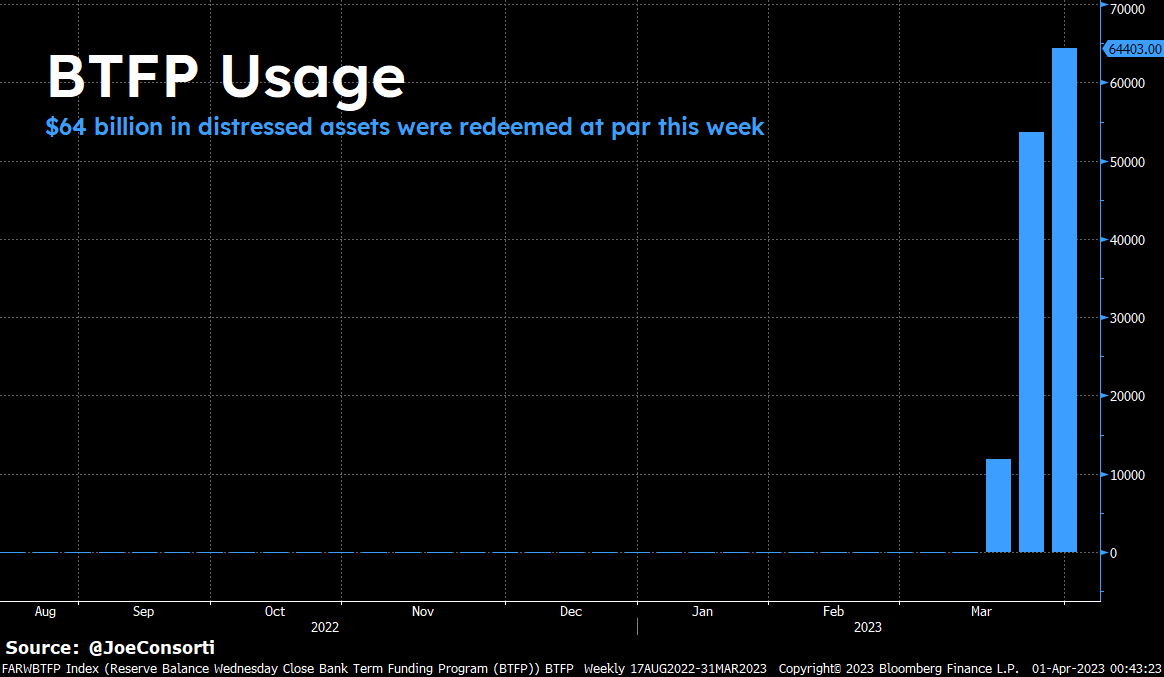

Usage of the new BTFP facility for emergency loans rose $11 billion from last week to $64.4 billion—a paltry increase compared to last week’s, but still, a sign that there are some banks out there in dire straits and borrowing cash against their distressed assets at par value to temporarily recoup their losses and stay in business:

And finally, on the global front, $55 billion was borrowed from the Fed’s foreign USD repo facility this week—this is noteworthy because not only is the facility rarely used, but the limit that a single counterparty can borrow is $60 billion. It’s reasonable to assume that this borrowing is not many, but a single distressed foreign bank:

All told, the Fed's balance sheet fell by $28 billion this week, a sigh of relief after the last two weeks of expansion that undid the majority of QT. Less liquidity is being siphoned from the Fed, meaning these emergency loan facilities are doing their job in bringing down aggregate levels of credit stress within the banking sector.

Though these facilities have tided over the crisis, banks will still extend less credit to one another, and ultimately to the real economy. This funding shortfall in the interbank market is exactly what the Fed has been cultivating since it started raising rates last March and practicing QT last June—banks backing off from one extending credit to one another so that they slow loan and credit creation to people in the real economy and bring down inflation. The success of the Fed in containing the fallout of distressed banks without having to cut the policy rate gives them all the more reason to hold it here for an extended period of time.

The ‘longer’ phase of ‘higher for longer’ is here.

Now the question has shifted to: how long can the Fed maintain 5 - 5.25% Fed Funds? With inflation still in the 6-handle, it will keep Fed Funds steady as long as it can without unwinding the labor market, creating devastation in the real economy, or contributing to dangerous disruptions in financial plumbing and bank funding.

Following a knee-jerk reaction to the Fed’s pause rhetoric, rates gave back most of their post-FOMC meeting gains. Now, we’ll get a chance to see just how intensely the “flight to safety” crowd wants to force the Fed to cut rates, not just hold them:

Rates similarly may have gotten out ahead of their skis last week with expecting solely cuts from here on out. Now, there is a 50/50 chance that the Fed hikes by 25 bps in May—a sentiment that has been echoed as reasonable by Fed speakers:

For those new to The Bitcoin Layer, the foremost piece of our macro analysis framework is the US Treasury market, which we refer to broadly as the rates market. The Fed attempts to influence front-end rates by setting its own policy rates—but when front-end rates diverge from the Fed’s path, it has lost its ability to set policy effectively.

The 2-year US Treasury yield has fallen below Fed Funds by ~100 basis points. The Fed has lost control of rates and further hikes would be futile or even damaging:

The Fed pause rally is here in full force

The Nasdaq has risen 20% since its December low and is officially in a new bull market, with the S&P 500 not far behind. Every time the Fed’s hiking cycle shifts from rate increases to an on-hold period of no hikes for many months, risk assets have a healthy rally. And after a long while, it’s finally here:

Liquidity dictates asset prices, and the expansion and contraction of the Fed’s balance sheet has been an accurate proxy for the direction of those asset prices. With several billion dollars of emergency lending expanding the Fed’s balance sheet in the past few weeks, risk assets are soaking it all in and appreciating accordingly—the punch bowl, whether the Fed intends for it to be back, is back in the eyes of the market:

What’s the most porous liquidity sponge of all, tracking the tide near 1:1? Bitcoin.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

This risk rally is transitory, the credit contraction has only just begun

Yes, we invoked the word ‘transitory’. We promise we will use it more accurately than Jerome Powell and Janet Yellen did regarding inflation.

We’ve entered a period where the mere shift from aggressive hiking to stopping hikes is spurring risk-taking behavior—even though the policy rate is still at an elevated, unaccommodating 5%.

This has been the case during every instance of a Fed pause—we knew that this would happen because we looked ahead. Now, let’s look ahead once again.

Now that we’re in this transitory risk-on rally, where will the cycle turn next? Firstly, the new bull market across major equity indices can be misleading, in that many will see the equity performance as a sign that good economic times are ahead, and this simply is not the case.

The credit cycle downturn is just getting started. The passthrough of tight monetary policy has only just hit the banks. Once it hits the banks, then it moves to consumers and businesses in the form of higher credit card rates, higher mortgage rates, and tighter loan standards for commercial real estate and businesses. These things take time. The contraction of credit in the real economy and subsequent growth slowdown are the next steps after the current bank funding crisis.

ODL, a monetary and credit aggregate that excludes currency and money market funds, is down $434 billion in March to $15.26 trillion. As stated previously, fewer deposits in the hands of banks means less funding for new loans and credit—this rapid deterioration of money and credit is very disinflationary.

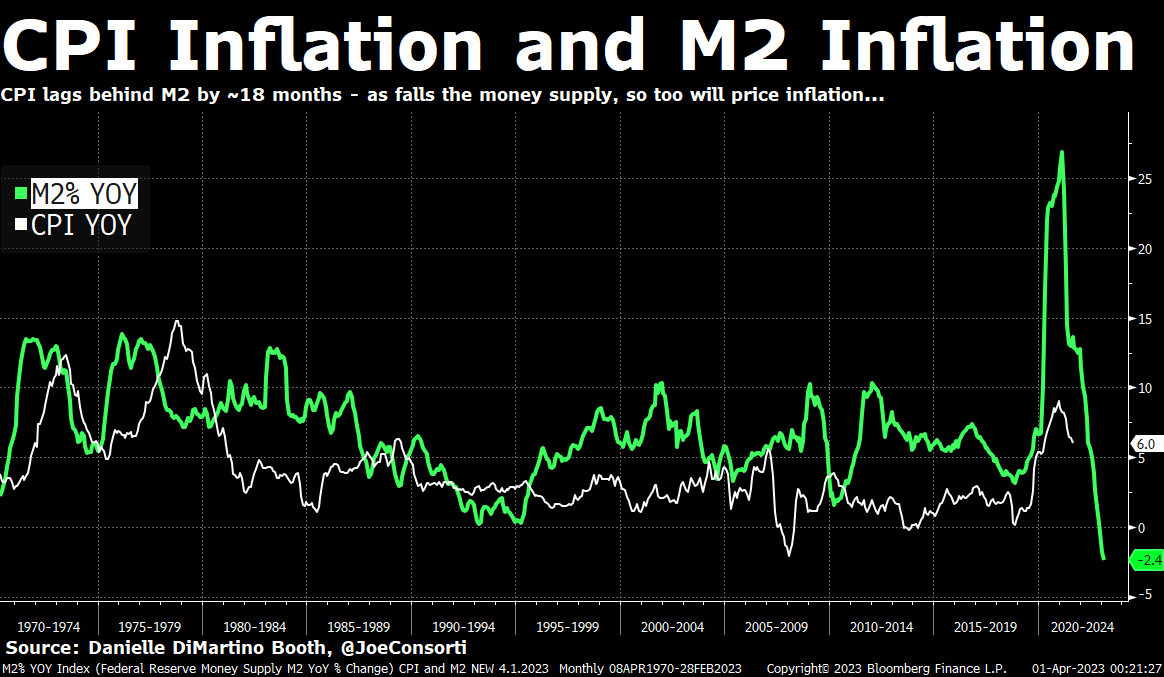

The M2 measure of money supply fell -2.4% year over year, which is the biggest deterioration of US dollars since the 1930s. It takes roughly 18 months for CPI inflation to catch up to the expansion and contraction of money and credit. As M2 and other monetary aggregates collapse, price inflation will soon follow:

When cuts come, it will not be bullish. While a lower discount rate is supportive of equity valuations and the underlying companies, the Fed cuts because something in financial markets, the labor market, or the real economy has deteriorated suddenly to a point where a swift reversal to easy policy is warranted. When this happens, even as the Fed cuts, equities react negatively to the pandemonium and fear in the real economy.

The ‘longer’ phase of ‘higher for longer’ is here, and the goal is to restrict credit. The result is a credit crunch, a deflationary force. When the credit crunch does come, it will hit less creditworthy businesses first, which will be visible in the credit spreads charged to these high-yield borrowers. After businesses, it’s consumers, visible first in housing and then initial jobless claims and unemployment. But first, all eyes on HY spreads, which are modestly elevated but not flashing any ringing sirens at the moment:

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Learn bitcoin’s basics, how to use it, and why we need it. For a live-education experience and introduction to bitcoin and Lightning Network, catch Nik in Los Angeles for “Bitcoin & The Future of Money” on April 29th.

Here are your quick links to all of the TBL content for the week:

Monday

In this episode, Nik sits down with Stacie Waleyko, an open-source developer and educator in the bitcoin space. She takes us under the hood of the Bitcoin protocol, explains what BIPs are and how they are used to submit new ideas about how Bitcoin should be improved, and exciting developments happening in Bitcoin development.

Check out—

Don't Like Bitcoin? Come & Change It | Open-Source Bitcoin with Stacie Waleyko

Tuesday

Banks are capital allocators. They take in deposits and use them to purchase securities and write loans. But what happens when banks stop dealing with one another and instead they go to the Fed for their funding needs—as has been the case over the last three weeks? They back away from extending credit to consumers and writing loans to businesses and property developers—a credit crunch ensues.

With bank failures tightening loan standards for commercial real estate, rising office vacancies cutting off revenue, and a maturity wall approaching when developers will either have to refinance at a staggeringly high rate or default, the stage is set for a crash in America’s commercial real estate market, again.

Check out—Commercial real estate is the next victim of the credit crunch

Wednesday

In this episode, TBL's Energy Correspondent Max Gagliardi returns to the show to discuss the petrodollar with Nik amid news surrounding the transition away from a US dollar-based global oil trade. Max also delivers a variety of different takes on energy, including gas versus oil and the future of natural gas from a geopolitical perspective, and how the American political landscape affects the energy industry.

Check out—The Future of The Petrodollar | Max Gagliardi

Thursday

In the most recent episode of the never-ending backstop, some banks are closing and others are squandering. But Nik’s eyes have drifted elsewhere—JPMorgan’s CEO Jamie Dimon will be deposed under oath as part of a lawsuit filed against JPMorgan for enabling Epstein’s sex trafficking, as reported by the Financial Times. He also discusses liquidity headwinds.

Check out—

Jamie Dimon to be interviewed under oath in Epstein sex trafficking case

Friday

In this episode, Joe sits down with Joe Carlasare, an advisor at Amundsen Davis and our TBL Legal Correspondent. Joe delivers an excellent discussion about Binance's recent lawsuit from the CFTC, the potential for additional suits by the SEC and DOJ, Justin Sun's various crypto fraud cases, the Ripple x SEC timeline, the recent Well's Notice served to Coinbase, and why it's much easier to cut off banking partners if you're trying to kill crypto than going after individual companies.

This a can’t-miss discussion. Enjoy!

Check out—Operation Chokepoint 2.0 Is Strangling "Crypto" | Joe Carlasare

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our bitcoin and macro recap—have a great weekend everybody!

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

The Bitcoin Layer does not provide investment advice.

Power week, enjoyed the technical aspects of Bitcoin with Stacie a lot! Bitcoin the technology is just as exciting as its ramifications as a bearer asset & disrupter to payment networks.

Learning so much with these posts. Thank you!