Dollar Challengers: Euro, Yuan, Gold, and Bitcoin

Four competitors lurk, but which is likely to emerge?

Dear readers,

Everywhere you look, it’s dedollarization. Headlines and narratives, of course. Because on the ground and within the banking system, it seems that all anybody wants is dollars. How realistic is dedollarization, though? Not very, especially when you look at the hard numbers. In today’s post, we’ll explore how hopes of a euro-, yuan-, or gold-centric monetary system are intangible. We’ll also explain how bitcoin adoption is the only competitor with promising, albeit early, momentum.

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

Dismissing the euro

Europeans are often offended when you refer to their currency as an experiment, but in a little over two decades, the euro trial has failed to bring about a core component of a reserve currency—a unified euro-denominated bond market. Readers of The Bitcoin Layer are familiar with our bias toward the fixed-income market’s role in greater capital markets, so the international investor’s choice between German and French government bonds leaves much to be desired from a market cohesiveness perspective. While 20% of global FX reserves are held in euro, relative to the 60% held in dollars and meager 3% held in Chinese yuan, the escape velocity of this share is as explosive as tortoise’s—this 20% is essentially unchanged since the euro’s rollout in 1999 and down from almost 30% in 2009. Additionally, the euro is far from conversations about how the world will dedollarize. Perhaps it has something to do with Europe’s inward facing problems, such as political dissonance in Brussels, an energy crisis, and an economy perennially trailing the rest of the world in growth. Hardly inspiring. Next.

Dropping the dollar…in 2010

Surely China is the competitor to pose the most serious threat. Right? Wrong. A public service announcement for those maybe under the impression that times have changed: the Chinese yuan is still not a fully convertible currency. This means that one may not, without the consent of Chinese state authorities, transfer yuan in or out of the country of China. A fully convertible yuan would threaten the Chinese government’s grasp on the exchange rate, something that would jeopardize the Communist Party’s control on the economy.

This was not supposed to happen—when China joined the World Trade Organization in 2001, it promised to internationalize its currency. Then, after the Great Financial Crisis of 2007-2009, China and Russia formed a pact to ditch the dollar in all bilateral settlement, something that was sure to set off the dollar’s demise:

What has happened since 2010? The dollar index has risen approximately 20% versus a basket of global currencies, and the Chinese yuan now makes up a whopping 3% of global FX reserves. Notice that the same headlines continue to recycle themselves every few years, and you’ll pick up on a trend: announcements of pacts of agreements to plan to achieve are not the same as physical transactions or allocated foreign exchange reserves.

Take China’s belt and road initiative, in which China is building out infrastructure across Eurasia and Africa that directly facilitates trade between China and the world, for example. As part of the initiative, China lends money to other nations in order to build these projects—initially, the loans were made in Chinese yuan, but borrowers were immediately swapping yuan for dollars to spend on materials and labor. Why? Yuan is largely useless on the global market. In a hilarious turn of events for proponents of the yuan-centric future, belt and road initiative loans are now predominantly issued in, you guessed it, US dollars.

But what about Saudi Arabia “considering” selling oil for yuan?

This consideration is not met with reality, as described by Javier Blas in a recent Bloomberg column:

Blas details how dedollarization, especially one that makes way for a petroyuan, is truly a myth:

Ask quietly in government circles in Riyadh, Abu Dhabi, Kuwait City or Doha about the petroyuan, and the response — even in the weeks following Xi’s visit to Riyadh — is unanimous: the petrodollar is here to stay. On a recent trip to the region, I didn’t hear a single official talking seriously about making preparations to introduce a new currency to the mix. The answers sound a lot like this: What’s in it for us? The greenback is freely convertible, the yuan isn’t; the dollar is liquid, the yuan isn’t. That’s the polite version; the more candid answers sounded even more emphatic about the absurdity of turning to a managed currency produced by an opaque and unpredictable financial machine.

What’s more, Saudi Arabia and the UAE both have currencies pegged to the dollar. Where does a non-internationalized yuan fit into this picture? It doesn’t, and as we stand today looking out over the next decade, the Chinese yuan poses no threat as the driving force of dedollarization.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

US bond market and technology cold war

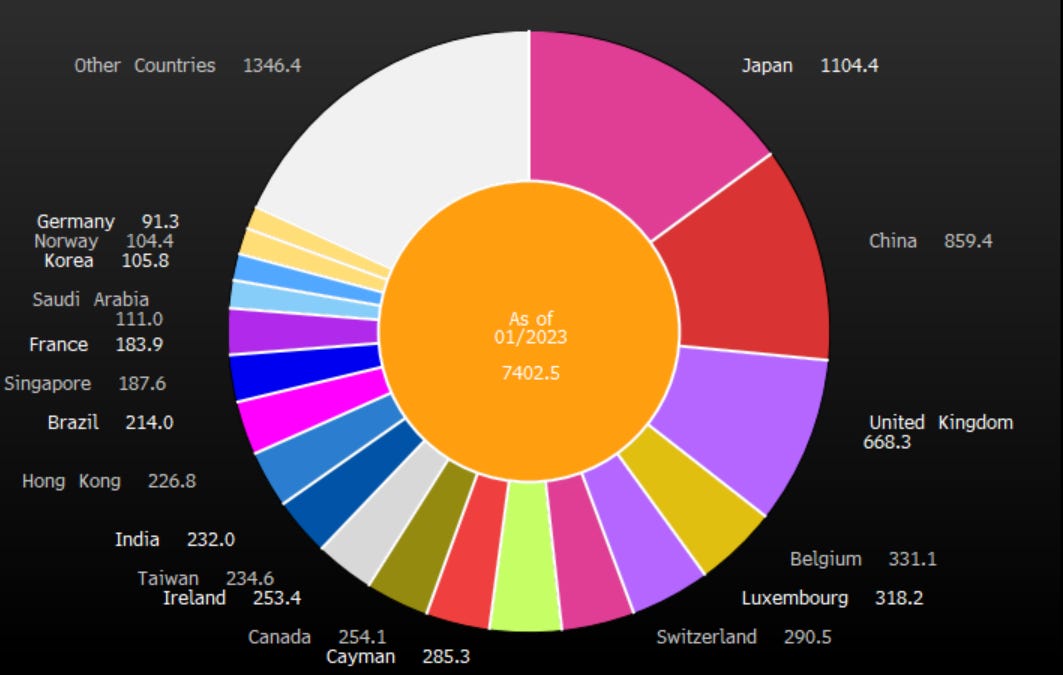

Foreign countries are not abandoning US government debt as the American fiscal picture spiral out of control—in aggregate, rather, holdings are up significantly over the past two decades. Here is a chart of the total foreign holdings of US Treasuries, up from $1 trillion in 2003 to $7 trillion today:

In 2003, we can see China’s $120 billion and Japan’s nearly $400 billion stockpiles:

Now, see how recent data shows a tripling in Japan’s holdings and a China adding to its holdings by a magnitude of 7x:

The US Treasury reserve asset complex is expanding rapidly over any modest time horizon, despite what fear mongering headlines and short-term trends might have you believe.

How does foreign ownership of Chinese bonds compare? About $500 billion in Chinese bonds are held by foreign investors. With over $7 trillion in foreign holdings of US Treasuries and over $12 trillion in total across the entire US bond market (including MBS and corporate bonds), the Chinese bond market is a blip on the fixed-income market radar.

What else would need to change in order for investors to flee US Treasuries for Chinese government securities? For starters, a resolution to the technology cold car currently underway between the two nations. In 2018, US companies were banned from selling software and hardware to ZTE, the Chinese telecommunications company, and ever since, the United States and Chinese governments have levied tariffs and bans on each other in a growing state of strife. In such a technology cold war and geopolitically uncertain environment, will nations choose China in the fight over the United States as a bet that China will emerge the world superpower, and will they make this choice by swapping US Treasuries for Chinese government debt? Probably not, and yet another reason that the entrenched dollar is unlikely to yield to another nation’s currency any time soon.

Is there any optimism on the fiscal side?

If the United States continues to run fiscal deficits exceeding $1 trillion annually as far as the eye can see, the situation becomes more pressurized as interest payments would start to swallow most of the incoming tax revenue. While US debt to GDP is likely to remain elevated, the US has seen a modest decline from 135% to 120% on this measure over the past couple years after pandemic assistance caused a 25% spike practically overnight in 2020:

It is possible for the US to bring its debt to GDP down, but neither party nor the two working together have been able to lower this measure since the 1990s. One can be optimistic while still recognizing the trends of gargantuan fiscal deficits.

Gold is old

Official holdings of gold, including central bank reserves, clocks in at $2 trillion. This amount falls short of the foreign ownership of US bonds ($12 trillion) and dwarfs foreign ownership of Chinese bonds ($500 billion), but it doesn’t capture the entire picture about gold and its role in the future of money. Gold is a physical commodity, and it doesn’t have any relevance as an international settlement tool. In fact, statistics don’t even exist for how much international cross border trade occurs in gold, because it simply doesn’t. Gold is still a crucial neutral asset for investors, but the world is unlikely to return to such a level of analog trade.

That leaves us with bitcoin

If the euro is a strong currency but regional at best, Chinese capital restrictions prevent the free flow of yuan, and gold isn’t realistically used in international settlement, that leaves us with bitcoin as the last contender to the dollar. And what you find out is that despite bitcoin’s $600 billion market value, which slightly exceeds foreign holdings of Chinese bonds but still remains shy of official gold reserves, the energy around the discovery of this neutral, digital commodity has already spread across the world. There are now over 50 nations around the world with a bitcoin adoption rate of 10% or higher, and a staggering 20 nations with an 18% or higher adoption rate:

Are you in desperate need of a bitcoin 101? Catch Nik in Los Angeles for “Bitcoin & The Future of Money” on April 29th for a bitcoin bootcamp to bring you up to speed!

Currently, the number of people estimated to have some long exposure to bitcoin is in the hundreds of millions—we estimate that bitcoin will see a billion users by the end of this decade. Bitcoin’s adoption trend calls into question any momentum the euro, yuan, or gold might have in challenging the dollar. The dollar remains dominant and entrenched, but the internet’s currency is just beginning to strengthen its running legs. Let’s see before how long it enters a full sprint.

Until next time,

Nik & Joe

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

The Bitcoin Layer does not provide investment advice.

Well thought out arguments. I hear a lot about dedollarisation, and the points presented in this article are good to keep in mind!

Great article! Good to know that greenbacks aren't going away...#TeamUSA