Fed to keep hiking blindfolded, commodities suggest peak inflation.

After a decelerating CPI reading, disinflation is telling the Fed that its attempt to cool the economy is working.

Dear readers,

It’s hard to know what the Fed is going to do. Yet FOMC decisions affect every asset class. At The Bitcoin Layer, part of our job is to help you forecast the Fed, while still headlining that rates markets largely lead the Fed. This makes our efforts looking at the markets, which are looking at the Fed. Allow us to catch you up on today’s global macro situation.

Voltage helps you solve the biggest problem with Lightning nodes and scaling. No more headaches with maintenance, reliability, or uptime issues. Voltage makes running Lightning instant and now easier than ever. These radical improvements to Lightning empower startups and enterprise brands to bring incredible applications and services to market. You can also spin up a personal node and pay by the hour. Scale your infrastructure as fast as Lightning itself. Create a node in less than 2 minutes, just visit voltage.cloud

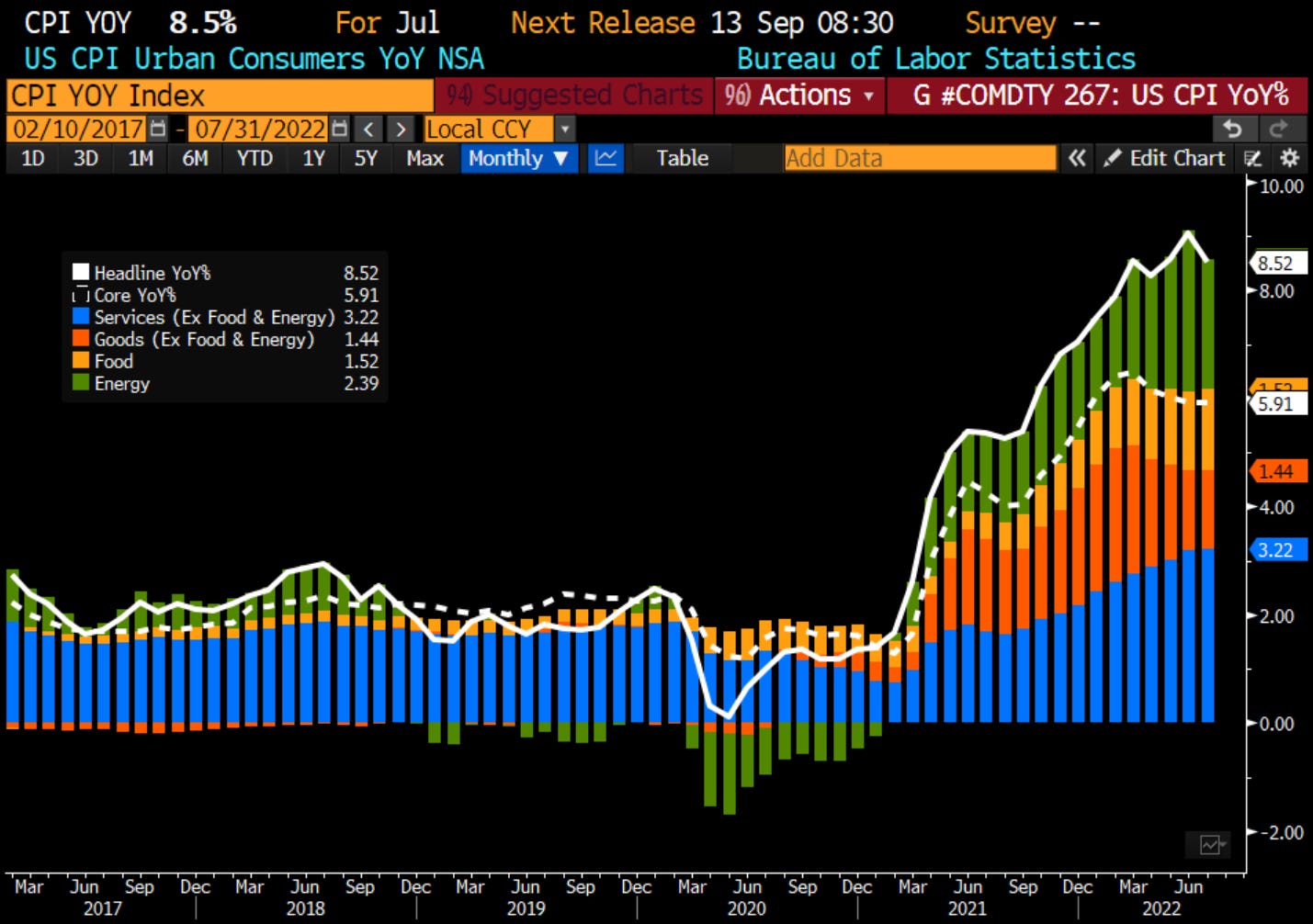

All Eyez on CPI

- Amazon.com Music")

The Federal Reserve claims to be a countercyclical institution, tightening during boom phases and easing during bust phases. But over the years, it has become procyclical—easing well into boom phases and tightening during bust phases. This drives the economy scorching and freezing instead of hot and cold, leading to an extremely volatile business cycle. This conundrum defines the current era, and the deeply inverted yield curve screams of policy error:

After a strong labor report implied a strong economy last week, all eyes were on CPI on Wednesday. The result was a still-blistering 8.5% year-over-year increase, but accompanied by a minuscule decline in the month-over-month level, indicating that inflation has indeed turned negative at the margin.

How will the Fed react? It is now balancing a very strong labor market and high annual inflation numbers with decelerating monthly inflation and swiftly correcting energy prices—which numbers should it listen to, and which numbers will it listen to? For now, nothing is as damaging to the Fed as 8.5% annual inflation. This is why we, and the money markets, believe the Fed will hike at least 50 basis points in September.

On the slowing side, generic gasoline is now down 28% from its highs in June. This will eventually show up in the annual numbers, but it has already started on a monthly basis. The energy subcomponent of CPI declined over 4% in July. Observe this dynamic of commodities leading CPI inflation more clearly with copper:

Copper is a great bellwether for the economy (Dr. Copper) and correlates with CPI. Given that current inflation is driven in large part by energy, it’s logical to presume that it will soon fall back down as copper and energy commodities are signaling.

Potentially peaking inflation has led markets to believe that a 50 basis point rate hike is now warranted versus 75 basis points, but the market will see another CPI release before the September FOMC meeting. A lot could change before then. What we know is that the Fed wants desperately to keep hiking rates. What we also know is that the rates market won’t let them get away with it forever.

Two-year yields declined quickly after the CPI release, signaling that the markets believe a Fed pause is on the horizon for Q4 2022 or Q1 2023. For clarity, that’s a pause, not a pivot. A pause is an in-between step between hiking and cutting that the Fed will use to allow markets to digest higher rates before deciding on where next to take the policy rate. A pivot to lowering rates would only come after a deep recession or stock market crash—all we have seen so far is modest disinflation and stable credit markets. Remember: a pause is not a pivot.

Restrictive Fed policy

Slowing inflation indicates that the Fed’s tightening is working and the economy is decelerating. Will the Fed stop at the right time or overshoot into restrictive territory and cause a deflationary event?

There is a very conceivable scenario in which the Fed overextends itself with rate hikes given the perceived strength of the economy and pushes the terminal rate far beyond what the economy can stomach. Remember, the anticipated 50-75 basis point hike in September would be the first time since 1979 that the policy rate would surpass the last cycle’s terminal rate. We will watch the inversion in the Treasury yield curve to signal the Fed it has gone too far. But when will the Fed receive the signal? It remains single-minded on CPI.

Until next time,

Nik & Joe

This post was sponsored by Voltage, provider of enterprise-grade Bitcoin infrastructure.