Is the US Fed At War With European Banks?

Examining the thesis that Jerome Powell's Fed is trying to regain control of its monetary policy away from Europe.

Dear readers,

How far is he willing to go? And does the motive stretch beyond inflation fighting? Today’s post presents the crossroads at which Jerome Powell finds himself today. A rapidly slumping housing market, the Senate Banking Committee Chairman reminding Powell of the Fed’s other mandate, and indications of a Yellen-led US Treasury market intervention all have us monitoring the money markets for signs of the end of tightening. But are there larger, geopolitical forces at play?

Voltage helps you solve the biggest problem with Lightning nodes and scaling. No more headaches with maintenance, reliability, or uptime issues. Voltage makes running Lightning instant and now easier than ever. These radical improvements to Lightning empower startups and enterprise brands to bring incredible applications and services to market. You can also spin up a personal node and pay by the hour. Scale your infrastructure as fast as Lightning itself.

Create a node in less than 2 minutes, just visit voltage.cloud

Today’s topics

I spoke with Tom Luongo last week and found his theory surrounding the reverse repo rate adjustment of June 2021 and the Fed’s European attitude shift compelling.

His theory will be pushed to the edge, as the Fed has in no way officially relinquished its role as the world’s central bank.

The US housing market is in really bad shape and will undoubtedly stay so with mortgage rates at 7%. The Democrats are now calling for the Fed to remember its employment mandate as it becomes crystal clear just how much pressure higher rates have on the economy.

Wall Street versus Euro Zombies

Our readers overwhelmingly subscribe to the mosaic theory—only by building a mosaic of different opinions, theories, and analysis can one even begin to process changes in the economy and financial markets as they happen. With so much noise, your job as the reader is to find the signal. And that means having range.

Some of you reached out to express just how much you value the analysis of geopolitical thinker Tom Luongo. I had to find out for myself.

Luongo is a political analyst and says he is “not a bond guy,” more focused on connecting the dots. His underlying thesis is that Jerome Powell’s Fed is finally, after decades, attempting to claw back control of dollar monetary policy away from the City of London and other European banks, which have used LIBOR markets to subvert the Fed.

Readers of Layered Money will be familiar with the Fed’s ECB central bank swap line introduced in December 2007, following the initial break between LIBOR and Fed Funds in August 2007. Luongo suggests that the days of the Fed being the backdoor life support of historically LIBOR-dependent European banks are over. And more specifically, they ended in June 2021.

His evidence for this begins with the Fed’s under-the-radar repo rate adjustment announced at the June 2021 FOMC meeting.

Reuters gives us the story:

June 16 (Reuters) - The Federal Reserve on Wednesday gave relief to money market investors that have been struggling to find high-quality short-term assets by raising two key short-term rates.

The Fed raised the interest rate it pays banks on reserves held at the U.S. central bank at the end of its two-day policy meeting. It also lifted the rate it pays on overnight reverse repurchase agreements, a tool used to set a floor on short-term interest rates. The technical adjustments are aimed at keeping its key overnight benchmark interest rate from falling too low.

The rate on reserves - known by the acronym IOER - will rise by five basis points to 0.15%. The rate paid on reverse repo operations, which gives financial firms a place to temporarily park cash in exchange for a return, will increase to 0.05% from zero.

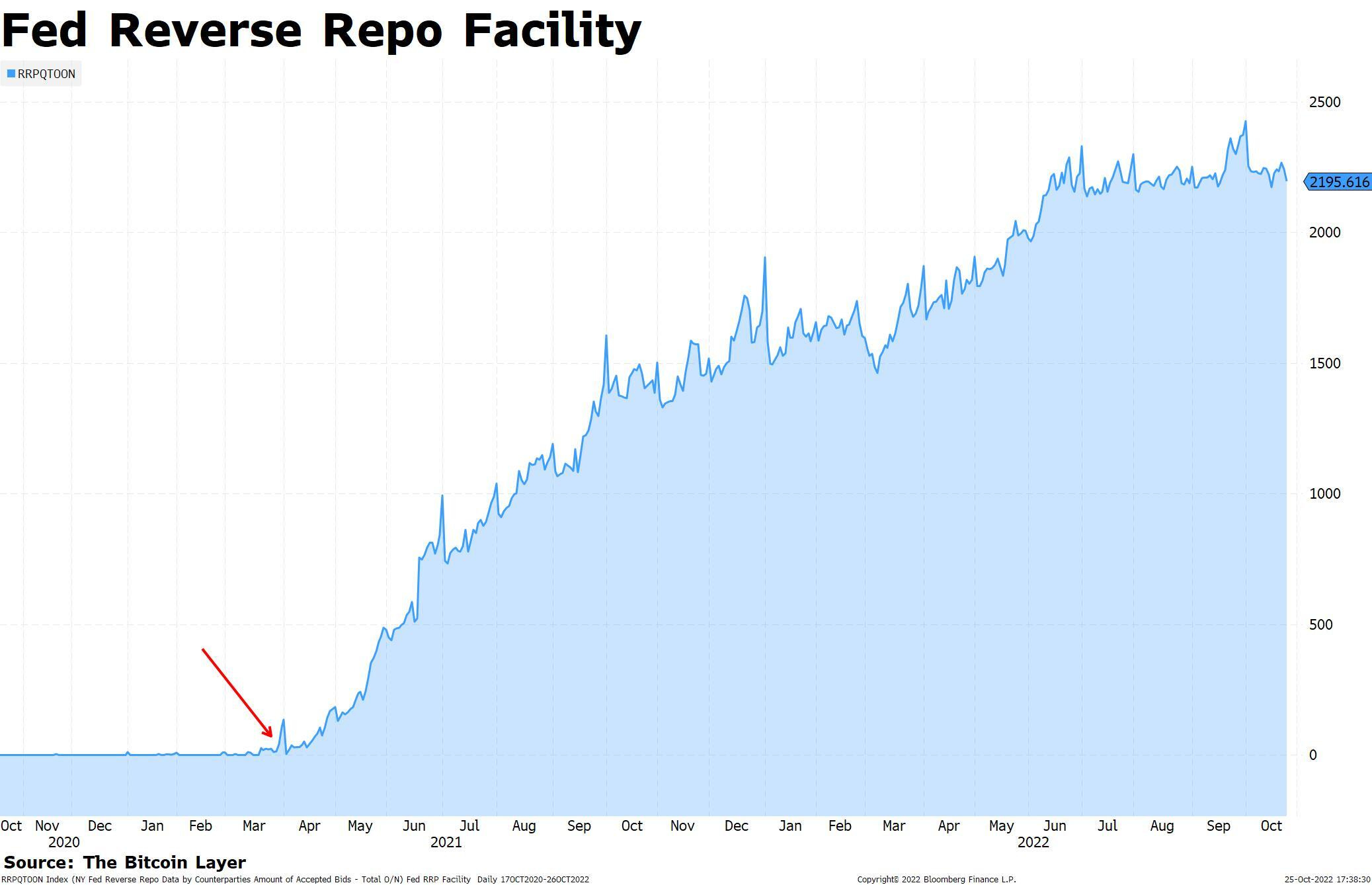

This might have seemed innocuous, but Luongo believes this was the beginning of a war of European banks led by Powell’s Fed—and the mission was to drain the European banks of access to easy LIBOR-based funding. The Fed raising the rate it offered to money market funds, which can easily toggle between short-term instruments in order to find the best yield, drew money out of the LIBOR markets and toward the Federal Reserve onshore dollar market. This is confirmed by the following chart of balances held at the Fed. Where did this money come from? June 2021 is indicated with an arrow:

Powell also said a firm “no” to pressures from Europe and the ECB to make part of the Fed’s mandate environmental in nature. Luongo believes this was another indicator that the Fed (influenced by its member banks, which are the large US commercial banks such as JP Morgan, Bank of America, and Wells Fargo) was ready to play hardball with Barclays, BNP Paribas, and Deutsche Bank:

Take a look at what happened to the dollar index, again with June 2021 marked. Straight up:

And the euro, straight down:

Why did this happen? He says that those “most vulnerable to massive rate hikes are in Europe” and that “Jay Powell is the new sheriff in town.” Luongo believes Powell’s ultimate goal is to “drain offshore dollar markets and allow the Fed to regain control of its own monetary policy.” Part of this is doing away with the Fed put entirely. Lastly, Luongo admits that he never imagined the Fed would get to 3% once the hikes began, as well as admitting that his current 6% Fed Funds prediction is slightly dramatic but meant to express the point that Powell is here to crush Europe.

Lender of Only Resort

The problem with Luongo’s theory is that it hasn’t really been tested. Yet. Today, the global economy stands in precarious but not disastrous shape. Stock markets are not collapsing. Christine Lagarde, President of the European Central Bank, has already started asking for “coordination,” basically a plea to the Fed to stop trashing the euro by way of higher dollar rates. If Powell continues to raise the finger (the one between the index and the ring) across the Atlantic, the basis for a newfound anti-Eurodollar Fed exists. I’m sure that the Fed wants a system less dependent on Eurodollar funding and less susceptible to Fed-swap-line-backstopped European banking crises. But I cannot see behind the veil of the inner power politics between the World Economic Forum, the White House, Congress, each party, the Fed, US banks, and European banks. The only way we’ll know if the Fed regime changed in June 2021 is by judging its response to the next financial crisis in Europe. For now, Powell is talking a big game.

The Tides Are Turning

Some imagine that Powell can go all the way to 5% and beyond, but the shifts in interest rates started on Friday with this headline, and continued to see follow-through today:

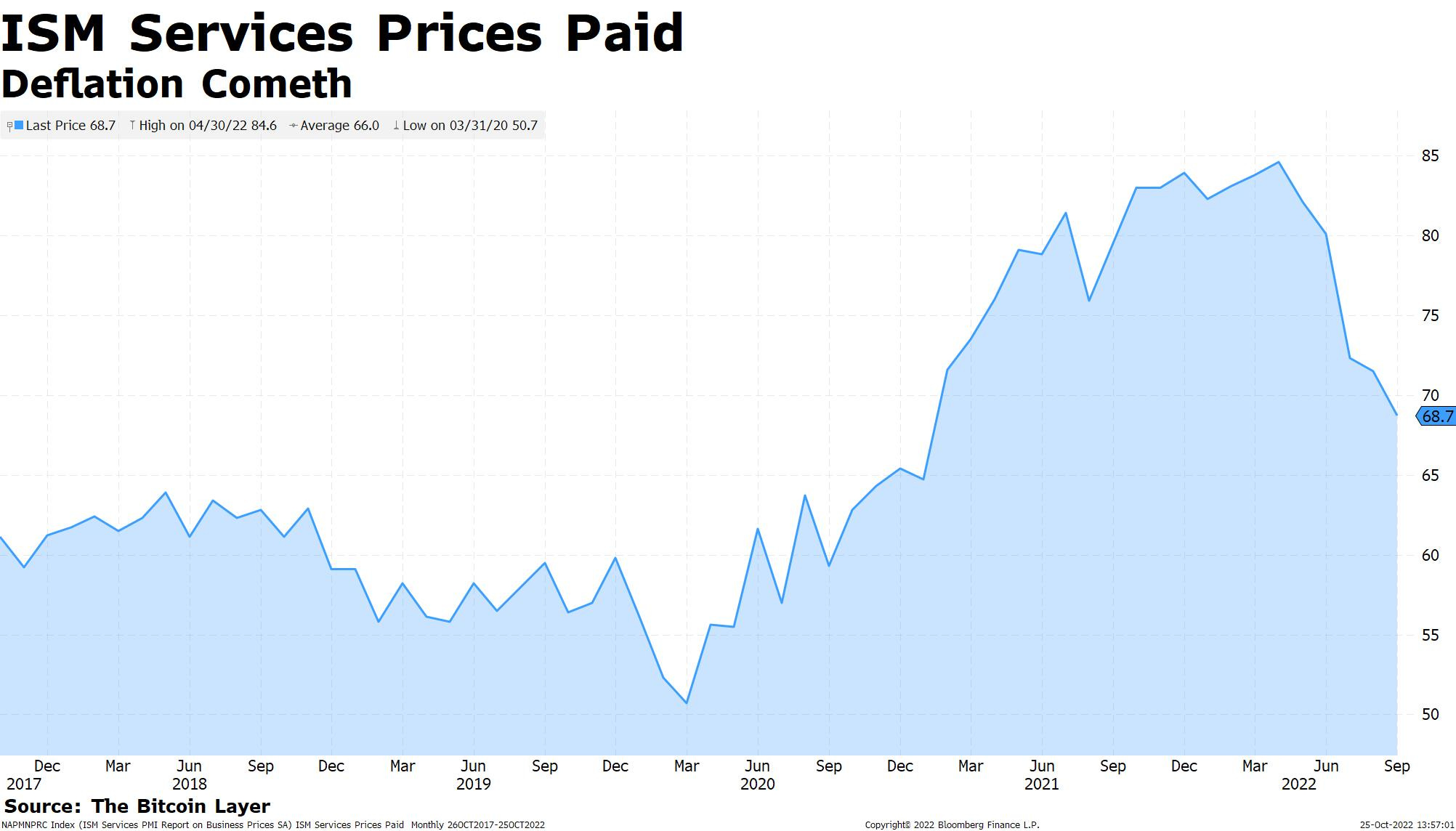

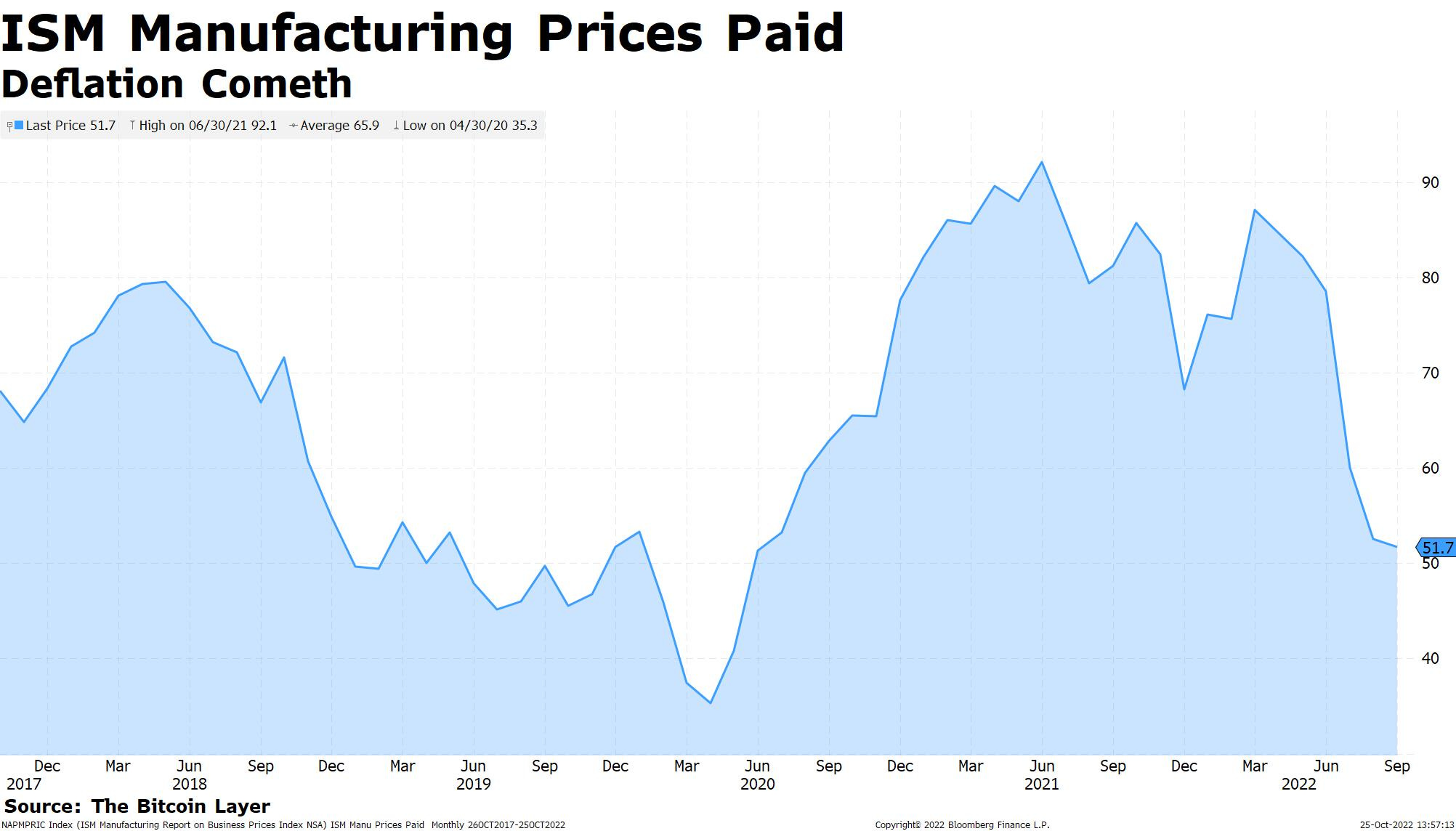

Leading with a cycle approach to monetary policy prescription, we must take into account the disastrous housing market, PMI surveys well into contraction territory, material disinflation in both ISM (services and manufacturing) “prices paid” components, and an increasingly loud political response to unpopular rate hikes. Take a look at the slowdown in input costs for US businesses since the beginning of the summer:

In very plain language, people on both sides of the political spectrum are getting hit by expensive mortgage financing, and politicians are now boisterously reminding the Fed that it must look out for the health of the US workforce in addition to fighting inflation. All the Fed has to do in order to pivot its language is to rediscover its currently secondary mandate.

Coming into an election, we can expect more of this, and readers should remember that this type of politics swings both ways, as the right was a very vocal critic of rate hikes toward the end of the last hiking cycle:

Slow it down Jay, says the choir. Ease the grip, cries Europe. Will Powell succumb to the cycle and the Fed’s inherent position as global central bank, or is he a genuine shift in the world order, driving the United States into more of an isolationist approach to global finance as it has recently with regard to strategic technology and Chinese geopolitical relations?

What I Am Watching

The US Treasury looks like it might launch a buyback program, and maybe as soon as November. It will have to work together with the Fed to execute, and the impetus might have been the Fed’s QT itself. Does this also put the Fed in the crosshairs?

Bitcoin is above $20,000, stocks are on a little tear, and global rates are starting to curl over. We remain convicted in our view that slowing growth and inflation will contribute to easier policy and supported risk assets. We’ll cover both of these topics and look at some charts in tomorrow’s video.

Until next time,

Nik

The Bitcoin Layer is sponsored by Voltage: provider of enterprise-grade Bitcoin infrastructure. Create a node in less than 2 minutes, just visit voltage.cloud

Nik, does the Fed line to the Bank of Switzerland run counter to the Luongo narrative?