Overtightening Talk & The "Soft" Pivot: TBL Weekly #17

Recapping the action in bitcoin and macro. Nik interviews Michael Saylor.

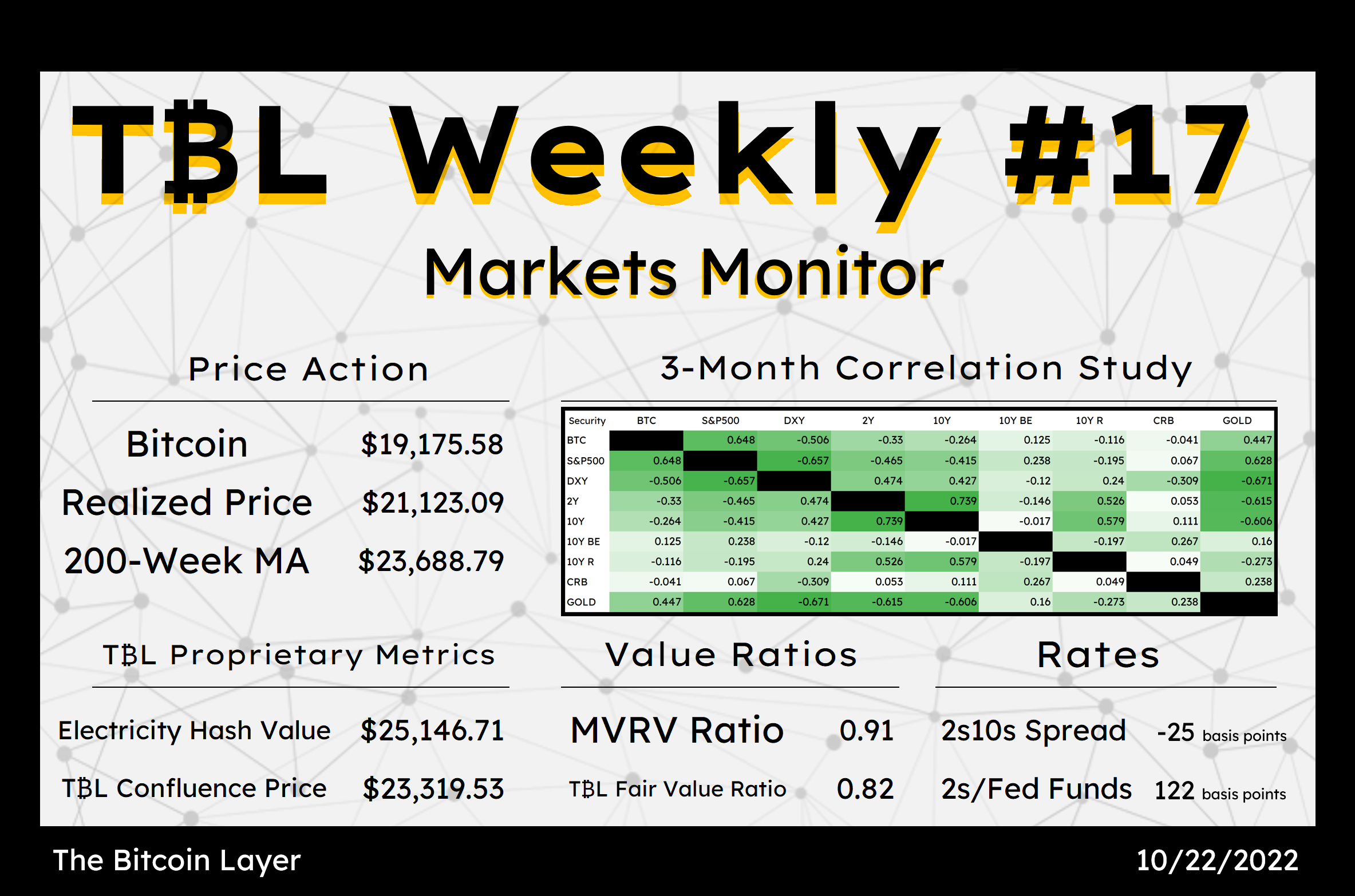

Welcome to TBL Weekly #17—here are your highlights!

Markets Analysis

Our monitor for the week ending Saturday, October 22nd, 2022:

Bitcoin has been below our fair value price for 97 days this year. A $400 billion market cap has been staunchly defended with relative ease, compared to the much larger S&P 500 index at $34 trillion in size. Can there be a deflationary impulse that drags down bitcoin? Of course, the likelihood of one remains as financial turmoil proliferates through England, Japan, and Europe. However, the resilience of bitcoin at this level cannot be understated. The ease at which it has and can continue to be defended at this level—thanks to its low liquidity profile—grows our confidence that this is the bottom price range for this cycle.

Is a pivot upon us? Precarious liquidity conditions are pummeling global financial plumbing as bonds selloff and yields notch high after high. Fed officials have begun openly pondering overtightening, portending a potential pivot.

We wanted to start your Saturday off with some cheerful alliteration!

We don’t view yesterday’s shift in Fed speak as a full 360° pivot to dovishness. However, openly discussing overtightening risk and forecasting when it plans to slow its hikes through the Wall Street Journal is a step towards an eventual pivot. Let’s call this a soft pivot. The Fed is floating the notion of slowing its rate hikes, finding a ceiling for rates, and observing how the market will digest it. Its latest WSJ leak is a classic example of a central bank trial balloon, in which it tests a policy move by hinting at it and seeing how the market reacts. The full shift is a process that takes months to transpire, but we might have witnessed the first inklings of it yesterday:

We are now at the point in policy where we must be thoughtful. We need to do everything in our power not to overtighten…

We will perform a step-down, but not a pause, to 50 or 25 bps increments.

It is important that we slow our rate hikes.

San Francisco Fed President Daly

The Fed is ostensibly feeling uneasy with the rapid pace of rising Treasury yields. Saying “we must be thoughtful” is a logical tactic to quell public fear that the Fed senses restriction. Let’s look at how yields reacted, down slightly on the day after flirting with another cycle high. By itself, the latest daily candle could indicate a trend reversal, but the bearish nature of the overall chart makes such a call dangerous:

The Fed is also acutely aware that raising its policy rate forces other central banks to raise theirs in sympathy. Channeling Christine Lagarde, Daly addressed this:

We must consider synchronized global central bank tightening.

San Francisco Fed President Daly

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Now, here are your quick links to all of the TBL content for the week:

Tuesday

Stocks are calling the Fed’s bluff, but aren’t always the most reliable leading indicator.

The S&P 500 is testing its June lows, but refusing to puke in extraordinary fashion as we saw in 2008 following the demise of Lehman Brothers. As you can see below, stocks are following eerily closely with this 2008 price action.

So the question is: does the stock market unwind, or does the Fed pause beforehand to stave off financial market dysfunction, saving risk assets in the process?

Nik & Joe break it down in Tuesday’s Substack:

Deflationary bust for stocks, or Fed pause beforehand?

Wednesday

Nik sat down with Matthew Pines, a Managing Consultant at Krebs Stamos Group, and a National Security Fellow at the Bitcoin Policy Institute. In this episode, he delivers a comprehensive breakdown of the tension between China & Taiwan, as well as the boiling economic war being waged with US Treasuries at the center:

We will have much more China geopolitical content in the coming months as Xi Jinping continues to affirm his emperor status.

Thursday

As government bonds continue their precipitous selloff, pushing yields higher and threatening global margin calls, the UK and Japan have already intervened to stem the bleeding.

The absence of big buyers is palpable, and Europe looks to be next on the chopping block.

With Europe potentially forced to stop QT before it even starts, and the UK and Japan already abandoning monetary tightening, when will the Fed be forced to follow suit? And importantly: what does it mean for bitcoin?

Nik & Joe explore it in Thursday’s Substack:

Pumping the brakes on QT, global dollar shortage, honey badger don't care

Friday

Nik had the pleasure of sitting down with Michael Saylor, Executive Chairman of Microstrategy. Michael delivers an inimitable guest lecture on bitcoin’s role in demonetizing real estate. He delivers a comprehensive and scathing rebuke of real estate as a store of value and lays out his case for why bitcoin will demonetize it:

To remind our gym-goers, long-commuters, and auditory learners:

The Bitcoin Layer is available on Apple Podcasts, Spotify, and anywhere you listen.

Apple Podcasts: The Bitcoin Layer

Spotify: The Bitcoin Layer

Hop right into Michael’s episode here:

Have a great weekend everybody!

The Bitcoin Layer is sponsored by Voltage: provider of enterprise-grade Bitcoin infrastructure. Create a node in less than 2 minutes, just visit voltage.cloud

Really enjoy your content and market perspective.

Just curious if you considered adjusting the energy cost input of your electricity hash valuation to account for miners setting up where they can purchase electricity at a discount, given how important energy costs are to miner profitability?

A Compass Mining post in July suggested many miners are paying hosting providers $0.06 to $0.08 per kWh: https://compassmining.io/education/how-energy-inflation-is-affecting-hosting-rates/

Accounting for this might bring the electricity hash valuation more in line with other inputs to the TBL confluence price.

Keep the content coming guys, it's brilliant and so accessible. Personally, TBL has become my signal in a noisy noisy media-space.