Pioneers: A Deep Dive Into Saylor's Strategy

The Bitcoin community’s opinion about Michael Saylor and Strategy ($MSTR), formerly MicroStrategy, seems to be just as volatile as the company’s stock. And honestly, I get it. I bought my first Bitcoin in 2014 and have closely followed the space ever since. Along the way, I’ve seen many heroes rise and fall. Eventually, skepticism toward any large player in the industry becomes natural—and rightly so. Remember: don’t trust, verify.

Before we dive into verifying Strategy’s plans together, TBL Pro readers, I want to acknowledge something about Michael Saylor. Whether you like him or not, agree with him or not, his willingness to lead from the front is undeniably admirable.

Recently, I listened to an interview between Tim Kotzman and Strategy’s CEO, Phong Le. While I haven’t fact-checked every statement, it seems clear that Strategy has consistently remained at the forefront of innovation for a long time. Innovation appears deeply embedded in the company's culture and DNA—and I'm almost certain that's largely due to "Mike," as Phong likes to call him.

But what truly defines a pioneer? At their core, pioneers venture into the unknown, driven by curiosity, vision, and determination. They challenge established norms, embrace uncertainty, and often endure significant setbacks. Not all pioneers achieve immediate success—many face failures, obstacles, and doubts. Yet, even during setbacks, pioneers adapt, learn, and pave the way for others. Ultimately, the legacy of pioneers is defined less by their successes and more by their courage to push boundaries and inspire progress, regardless of the outcome.

We’ll revisit this idea a few times, I'm sure.

As bitcoin's role in the global financial landscape evolves, understanding its potential impact on your wealth becomes increasingly crucial. Whether we see measured adoption or accelerated hyperbitcoinization, being prepared for various scenarios can make the difference between merely participating and truly optimizing your position.

This is why Unchained developed the Bitcoin Calculator – a sophisticated modeling tool that helps you visualize and prepare for multiple bitcoin futures. Beyond traditional retirement planning, it offers deep insight into how different adoption scenarios could transform your wealth trajectory.

What sets this tool apart is its integration with the Unchained IRA – the only solution that combines the tax advantages of a retirement account with the security of self-custody. In any future state, maintaining direct control of your keys remains fundamental to your bitcoin strategy.

Start with Why

To understand Strategy better and what they are trying to achieve, it helps to paint the bigger picture first before diving into the details.

I appreciate some of Simon Sinek's concepts, especially his principle of ‘Start with Why.’

The Wright brothers were true pioneers. Yet, if Polymarkets had existed in 1903, the odds would have been nearly 0% that they would achieve powered flight before Samuel Pierpont Langley. Simon Sinek argues that the Wright brothers succeeded where Langley failed because of their internal motivation—their Why.

While Langley was largely motivated by fame, prestige, and financial gain, the Wright brothers were driven by a deep, passionate belief in the transformative power of flight. Their unwavering sense of purpose inspired perseverance, experimentation, and innovation despite numerous setbacks. Unlike Langley, whose approach primarily focused on what (creating a successful airplane), the Wright brothers clearly understood their why—a vision of changing the world through flight.

Another example comes from Jocko Willink, an ex-Navy Seal who, in my opinion, embodies true leadership. If you asked him about the most important factor in successfully completing Navy Seal training, he would emphasize the Why. You must know why you're doing it. If your reasons are wrong, you'll quit along the way.

In my last article for TBL Pros, I distinguished between people who are Holding On for Dear Life and those who Hold Onto Decentralized Liberty. The difference between these groups lies in their Why. Why are you holding this asset? Is it for a quick profit, or to improve your life—and perhaps the lives of others?

I understand not all bitcoiners would agree with me, and I'm humble enough to admit if I need to reconsider my heroes, but I genuinely believe Michael Saylor chose this path because he sees Bitcoin as a solution to problems caused by manipulating the money supply. He views Bitcoin as the best proxy for money and believes humanity thrives under a sound money standard.

Another reason I think Saylor acts from genuine intent is his statement that he considers ‘burning his personal bitcoin’ to increase the value for all other bitcoin holders.

As Simon Sinek suggests, the right Why, combined with proper execution, results in profit for the company, ultimately increasing shareholder value. However, profit shouldn't be the primary goal. When the Why resonates, people naturally want to buy your products, use your services, or lend you their money. They want to be part of your vision, will remain loyal, and may even form a community around your company.

Volatility is Vitality

We’ve explored the Why. Now, let’s proceed to the How. Forgive me for being blunt here, but I think you'll get the reference:

‘It’s the volatility, stupid!’

Michael Saylor famously stated that “volatility is vitality,” highlighting how publicly traded companies often experience increased investor engagement and heightened stock demand during periods of significant price fluctuations. Strategy leverages Bitcoin holdings on its balance sheet specifically to introduce volatility into its stock, creating strategic opportunities.

Meanwhile, analyst Stephen Perrenod conducts comprehensive mathematical analyses of Bitcoin’s price movements. According to Perrenod, the beauty of Bitcoin’s volatility lies in its positive skewness—meaning that while significant volatility and downside risks certainly exist, Bitcoin historically experiences larger and more frequent upward price movements. Because of this positive skewness, among other favorable characteristics, Bitcoin stands out as the ideal asset for corporate strategic investment.

The options market plays a crucial role in driving greater investor demand, largely because options trading revolves around probabilities. Higher volatility increases the likelihood that certain strike prices will be reached before a given expiration date. Without delving deeply into option pricing and trading, the key takeaway is this: the higher the probability a strike price will be met within a certain timeframe, the more valuable the option becomes.

Highly valuable options attract traders of all types employing various strategies. Typically, however, assets with high volatility also suffer from low liquidity. Institutional investors usually avoid illiquid markets because they need to take substantial positions. Entering a market with insufficient liquidity can trap institutional investors if the trading volume dries up, especially if momentum turns against their positions, exacerbating their losses.

Yet, Bitcoin presents a unique opportunity by combining high volatility with high liquidity. With a market capitalization around $2 trillion, Bitcoin is large enough for institutional investors to enter and exit positions worth billions of dollars without significantly impacting the market price, provided the trades are executed strategically. Bitcoin's liquidity is further enhanced by its 24/7 trading availability, making it one of the most liquid assets in financial markets today.

Strategy is capitalizing on these unique merits. Although anyone could pursue this path, Strategy was among the first to recognize the opportunity and brave enough to commit fully to an all-in, Bitcoin-only treasury strategy, positioning themselves as pioneers on a new financial frontier.

Financial Engineering

You better refill that cup of coffee because you might need it. Next up: the What.

Michael Saylor is, as most of you probably know by now, an engineer at heart. And as I highlighted in the introduction, this engineering mindset permeates the entire company. For me, that explains the level of financial engineering taking place.

Without going too deep into the past five years, I want to emphasize the common thread in Strategy's evolution.

Before August 2020, MicroStrategy operated on a fiat standard. They were a successful Business Intelligence software provider holding about $500 million in cash reserves. Let's call that MicroStrategy 1.0.

The story behind why MicroStrategy transitioned to a Bitcoin Standard is well documented online. Enter MicroStrategy 2.0—it used all its cash reserves to buy Bitcoin.

Then, it realized it could borrow money to buy even more Bitcoin. If Bitcoin has an annual compounded growth rate of roughly 40%, and it could borrow at low interest rates (especially post-COVID, when rates were practically zero), this was a no-brainer. The company just needed the right type of leverage and chose convertible bonds. Remember the volatility aspect? Convertible bonds include a call option. If the stock price exceeds the conversion price, the bond can convert into stock. This makes the implied volatility (IV) of the stock critical. Higher IV increases the probability that conversion thresholds will be met, allowing higher conversion rates and thus higher value for common stock shareholders.

This is a key point. After some time, MicroStrategy was issuing convertible bonds with a 0% coupon rate and a 35% premium above the stock price at issuance. These bonds didn't consume cash flow due to their zero-coupon nature, and the premium allowed additional Bitcoin purchases. Those Bitcoin purchases further propelled the stock higher.

I should also mention the loan from Silvergate, which generated significant negative publicity around MicroStrategy’s potential liquidation risk during the 2022 bear market. In March 2022, MicroStrategy (through its subsidiary) took out a $205 million loan from Silvergate Bank, secured by its Bitcoin holdings. The loan was part of Silvergate's SEN Leverage program, primarily used to buy more Bitcoin.

However, after Silvergate Bank collapsed in early March 2023, MicroStrategy fully repaid the loan early, paying about $161 million—including a discount for early repayment—and retrieving the 34,619 Bitcoin held as collateral.

Ultimately, MicroStrategy emerged stronger due to the discount on early repayment. However, this episode highlighted the importance of carefully selecting leverage types. Although the Silvergate leverage ratio was conservative, unforeseen events—such as 3 Arrows Capital’s opaque arbitrage strategies with Barry Silbert’s companies, the collapse of Terra Luna's flawed algorithmic stablecoin, FTX’s deceptive selling practices, and Operation Choke Point 2.0 targeting crypto firms—created a perfect storm where even conservative leverage posed risks.

But again, wear that scar with pride as a tribute to pioneering.

On June 14, 2021, MicroStrategy announced its first at-the-market (ATM) common stock offering totaling $1 billion. Let's call this period, during which the company issued convertible debt and common stock at-the-market, MicroStrategy 3.0. In the 3.0 phase, it created two powerful levers to attract capital and purchase Bitcoin.

It's worth noting that MicroStrategy fully redeemed the 0.750% Convertible Senior Notes due 2025—issued in December 2020—by July 2024. Remarkably, these notes outperformed direct Bitcoin investment over the same period. Imagine that: investors who bought corporate bonds in December 2020 achieved better returns than if they'd bought Bitcoin directly. A bond-level risk profile with Bitcoin-level performance—absolutely phenomenal. This success laid the groundwork for the ambitious 21/21 Plan.

Announced at the end of October 2024, the 21/21 Plan consisted of three pillars:

$21 billion common stock at-the-market offering over three years.

$21 billion raised through fixed-income securities over three years.

Increasing annual BTC yield from 6% to 10% over three years.

This initiative was essentially an expansion of MicroStrategy 3.0, using the same financial instruments but at an unprecedented scale. One remarkable aspect was that the stock price didn't drop following this announcement. Normally, significant share dilution announcements negatively impact stock prices. But because MicroStrategy shareholders understood and believed in the Why, the price didn’t even flinch. It was epic.

In November 2024, Donald Trump won the presidential election, and Bitcoin, which had reverted to the mean during the summer, surged to the long-anticipated and desired price of $100,000. Consequently, $MSTR’s stock price rose above $500 per share, significantly increasing the implied volatility. With the considerable premium between MicroStrategy’s share price and its underlying Bitcoin holdings per share (mNAV), combined with the high IV, MicroStrategy managed to raise $20 billion of its total $42 billion target within just three months. Additionally, it revised its BTC yield target upward, aiming for a minimum of 15% in 2025.

Phase 4.0

The announcements of STRK and STRF, combined with the rebranding to Strategy, truly mark the beginning of a new phase for the world's largest Bitcoin treasury company.

These moves add two additional instruments to Strategy’s toolkit for navigating the digital asset frontier.

Interestingly, these latest announcements coincided with downward pressure on Bitcoin's price, impacting $MSTR as well. Strategy’s stock price had declined more than 50% from its highs by November 21.

Some investors are feeling significant pain; others are beginning to question the company's vision. Two more instruments? Is this really necessary? Why not stick to issuing convertible debt and common stock? Why change a winning formula? Isn’t Saylor over-engineering all of this?

If you read the comments on Lyn Alden’s question about the biggest threat to Bitcoin in the coming years, you’ll notice many believe Saylor will eventually spell the end of Bitcoin as we know it today.

I'm sensing that some shareholders may be losing sight of the What. I know this has been a long introduction to the actual topic, but sometimes that's necessary. Let's explore what all this means and what we should expect going forward.

Make Volatility Great Again

Let's examine whether these new additions to the toolkit are a net positive or negative. I wrote this lengthy introduction because, in my opinion, we need to revisit the How to answer this properly. Bitcoin remains the nuclear core of Strategy’s approach. Bitcoin’s volatility provides the energy required for the stock to enter price discovery. But what happens when Strategy dilutes its common stock? It creates additional supply to meet demand, ultimately dampening volatility.

Another key takeaway from the conversation between Jeff Walton and Richard Byworth is that many convertible debt buyers don't actually want directional exposure to Bitcoin. Institutions often hedge their positions to maintain delta neutrality. This means that when Strategy’s stock exceeds the conversion price, convertible arbitrageurs short $MSTR—not because they expect Strategy to fail, but simply to hedge excessive directional exposure according to their Black-Scholes models. They short $MSTR because their convertible bonds at those price levels will convert into $MSTR shares, and they need to balance their positions. The higher the stock price rises, the more they short, stopping only when the delta reaches 1.

This, too, dampens volatility. When the $MSTR price surpasses certain conversion thresholds, expect short interest to rise correspondingly.

And that's not even the whole story. There's also $MSTY—an ETF that employs a covered call strategy exclusively on $MSTR stock, providing enhanced income by capitalizing on the underlying stock’s volatility. This strategy further suppresses volatility.

Reduced volatility means less vitality. Yield strategies siphon energy from the stock.

Alleviating Pressure on the Common Stock

Michael and his fellow (financial) engineers—let’s call them Mikey Mike and the Funky Bunch—are observing this and recognizing the need to address the situation. They understand not all investors want full exposure to Bitcoin's volatility. Some prefer less exposure; others prefer none at all and are willing to accept lower returns in exchange.

Enter $STRK and $STRF. These new instruments directly address specific investor preferences. I imagine Mikey Mike and the Funky Bunch saying something along the lines of: “You want a 10% annualized yield but prefer to stay on a fiat standard? You don’t want any Bitcoin upside? You prefer a life of perpetual financial strife? Fine, we'll give it to you—just keep your fiat-focused strategies away from our common stock.”

Can you feel the good vibrations yet?

Indeed, these additions expand upon Strategy’s phase 3.0, allowing access to even more capital pools. That might actually be more important than solely maintaining maximum volatility in the common stock. However, I want to emphasize the importance of reducing selling pressure on the common stock. Strategy needs the common stock price to enter price discovery alongside Bitcoin.

BMAX

It's also worth mentioning the launch of the $BMAX ETF from REX, which invests in convertible bonds from Bitcoin treasury companies like Strategy, making these investments more accessible. Investors in $BMAX are likely seeking directional exposure to Bitcoin and thus probably won’t hedge by shorting the underlying stock. As more retail investors buy these convertible bonds through $BMAX, the dampening effect on volatility from arbitrageurs should be reduced.

Swiss Army Knife

With these new financial instruments, Strategy has essentially created the equivalent of a financial Swiss army knife, providing them with multiple tools to choose the most appropriate instrument for any given situation.

Capital structure

Let’s start with seniority across different instruments. In the event of a company default or liquidation, the order of seniority determines who gets paid first. Here's the hierarchy of claims from highest to lowest priority:

This hierarchy reflects the risk-reward relationship between the various instruments. Each instrument possesses unique characteristics, merits, and drawbacks, influencing every strategy that employs them.

Some instruments significantly impact common stock dilution, while others greatly affect the company’s cash flow. Some instruments are perpetual; others have specific expiration dates. Certain instruments expose investors to both common stock and Bitcoin, whereas others do not. Some pay dividends, others do not. Some stocks exhibit bond-like risk profiles, while certain bonds can deliver equity-like returns. Hence, my reference to a financial Swiss army knife. The diagram below highlights the distinct characteristics of each instrument.

Inverse Dynamics

Something particularly fascinating is the inverse dynamics of demand between $MSTR and $STRF. Excessive dilution of $MSTR eventually leads to declining demand and a falling stock price, even if the proceeds are used to purchase more Bitcoin. At some point, further stock issuance ceases to be accretive, causing the share price to plummet. With $STRF, however, the fixed dividend—10% of a $100 share price—results in increasing yield as the stock price decreases. For example, if $STRF trades at $50 per share, the yield rises to 20% annually.

A higher yield would attract more buyers rather than fewer. Of course, pushing it too far can undermine credibility, making even a 20% yield insufficient to offset perceived risks—but the principle remains clear.

Nuclear Rods

These additional instruments will attract new capital. Jesse Myers created the iconic chart Saylor has been referencing frequently. Jesse recently updated this chart, posting it on X, clearly illustrating the role of $STRF and its targeted market—a notably large one. While convertible bonds address only a small segment of the fixed-income market, $STRK and $STRF will cater to a much broader audience.

In an interview, Saylor stated that his target is capturing 1% of the fixed-income market—roughly $3 trillion, or $3,000 billion.

The benefits of $STRK and $STRF could significantly energize Strategy’s nuclear core. Offering common stock at-the-market is accretive only when a substantial premium exists—typically during Bitcoin rallies. During Bitcoin consolidation or downturns, issuing common stock at-the-market is less favorable because premiums shrink or even turn negative. Yet paradoxically, such periods present optimal opportunities for accumulating relatively cheap sats. Strategy has faced criticism for buying local tops, partly due to limitations of previously available instruments.

When Bitcoin experiences prolonged consolidation, $MSTR's volatility also diminishes. However, selling $STRK and $STRF at-the-market allows Strategy to add Bitcoin to the balance sheet without directly diluting common stock. It's akin to adding more nuclear rods to a power plant without extinguishing the remaining volatility.

If executed effectively and timely, these strategies could allow $MSTR to consistently outperform $BTC.

However, there's an essential concern we must address—a genuine, critical issue that cannot be overlooked: How on earth do Mikey Mike and the Funky Bunch plan to sustainably pay all these dividends, indefinitely?!

Where Does the Yield Come From?

If you’ve navigated the rough seas of the crypto space, you've learned to always ask the critical question: where does the yield come from?

BlockFi provides a cautionary example. Initially, its product offered a BTC yield of 4.5%, but it later emerged that the yield originated from the GBTC premium arbitrage trade via other firms. We all know how that ended.

Something Has To Give

While discussing the merits of instruments like $STRF within Strategy’s overall approach, it's also essential to acknowledge their drawbacks—specifically, the obligation to pay a substantial annual dividend of 10%. There’s no such thing as a free lunch; something must inevitably give. Either common stock dilution increases or the dividend steadily erodes the company's (free) cash flow.

Calculation

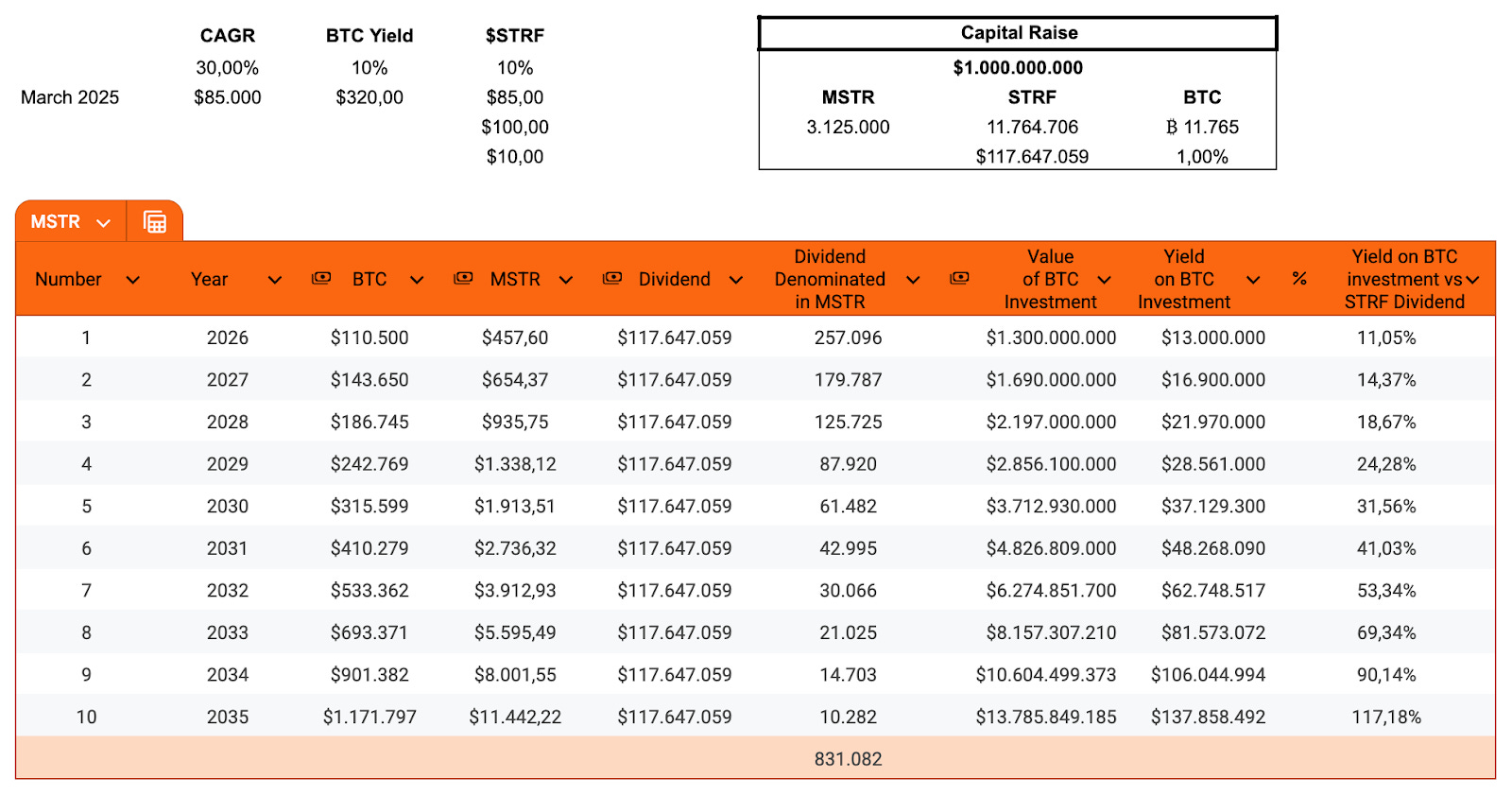

Because we can't predict the future, my calculations are guaranteed to be wrong with over 99.99% certainty. These calculations are not meant to precisely predict outcomes but rather to illustrate a method of thinking about managing future dividend obligations. Some readers might view my assumptions as overly bullish, while others may accuse me of betraying Bitcoin's ethos for my bearish outlook. I'll let you be the judge.

I'm assuming a Bitcoin CAGR of 30% over the next 10 years, a BTC yield for Strategy of 10% per year, and a potential yield of 1% per year on purchased Bitcoin in the near future. For other parameters, I've used the current prices for $BTC, $MSTR, and $STRF as of late March 2025.

With a target of raising one billion dollars, Strategy could acquire roughly 11,756 BTC. This would cost them approximately 3,125,000 shares of $MSTR or about 11,764,706 shares of $STRF.

Two key insights emerged from this analysis. If Strategy opts to pay all dividends by selling common stock at-the-market annually (the payout is quarterly, but I simplified it to yearly for clarity), they would need to sell a total of approximately 831,082 $MSTR shares over 10 years—just 26% of the shares they'd have otherwise sold through standard common stock ATM raises. This significantly benefits shareholders by reducing dilution.

However, dividend obligations are perpetual, meaning this advantage diminishes over time. This is where the yield on the initial purchase of 11,756 BTC becomes critical. Saylor has indicated in recent presentations, including those directed at government officials, that he expects future yields from Bitcoin holdings. According to my calculations, in ten years, the yield from this purchased Bitcoin would exceed 100% of the dividend obligation.

I’ll elaborate on the near future in the next section, but if this logic holds, Strategy could initially manage dividend payments through limited common stock dilution—approximately 75% less dilution than with standard ATM stock issuance. After about ten years, as the industry matures with robust, conservative yield offerings and asset prices rise, the yield from the initial investment should fully cover perpetual dividends.

Yes, a 30% CAGR will naturally decrease over time due to diminishing returns, and maintaining a consistent 10% BTC yield indefinitely will be impossible.

But even if you adjust the numbers, it might take 12 to 15 years for the yield on the investment to be high enough to pay for the dividends entirely.

Transition Phase

One of the most important skills of a successful entrepreneur is setting and evaluating priorities—this is where Saylors laser focus becomes crucial. Currently, Bitcoin is transitioning from "magic internet money" into a recognized industry asset considered essential for personal portfolios, corporate treasuries, and national reserves.

Nobody knows precisely how long this phase will last, or even exactly when it began. Did it start in 2020 with publicly traded corporations adopting Bitcoin treasury strategies? Was it 2021, with El Salvador making Bitcoin legal tender and adding it to their national reserves? Perhaps 2024, with the launch of spot ETFs? Personally, I'd argue it definitively began in 2025, when the USA officially created a Strategic Reserve and sought a budget-neutral approach to further acquisitions.

This transitional period represents the last significant window of opportunity for deploying accumulation strategies like those offered by $STRK and $STRF. These strategies only make sense while Bitcoin’s CAGR significantly exceeds the promised dividends in dollars. Eventually, this transition phase will end, and the CAGR will inevitably diminish.

The critical question is, what should Strategy focus on during this transition period? Should it prioritize developing yield-generating strategies for its Bitcoin holdings to reassure investors about future dividend obligations? Or should it instead focus on acquiring as much Bitcoin as possible now, trusting that future cash flow solutions will arise? Of course, Strategy must consider these issues now to accurately price preferred stock and other instruments at realistic yields that attract current investors without jeopardizing future sustainability. Perhaps merely having a clear plan for future yields is sufficient at this stage, without needing immediate resource allocation.

Inventions

In the "Saylor Series," a series of podcasts featuring Robert Breedlove and Michael Saylor, Saylor discussed the inherent difficulty in inventing new technologies, especially regarding timing. If memory serves, he used the example of a fighter jet. You might aspire to build and invent a fighter jet, but it's futile without the invention of critical components like turbine engines, aviation kerosene, or specific aluminum alloys. Without these underlying technologies, your invention can't materialize.

Applying this analogy to the anticipated and highly desirable yield on Bitcoin holdings, dedicating excessive resources in 2025 might similarly prove premature—or perhaps 2024 would be more apt, given the previous administration’s regulatory challenges. A pro-Bitcoin administration could swiftly change the landscape, ushering in deregulation and creating a friendlier environment.

My point is: who can accurately envision what a company holding over 500,000 BTC might achieve in ten years? Just as it's challenging to anticipate the capabilities of a future fighter jet when critical components haven't yet been invented, today's Bitcoin yields and dividends might similarly evolve unpredictably. Consider that the Rolls Royce Merlin V12 engine in a Spitfire produced roughly 2,000 horsepower, while today’s Pratt & Whitney F135 engine produces the equivalent of 40,000 horsepower for the F-35 fighter jet.

AI and LP

Strategy emphasizes its focus on two pivotal technologies of this era: Bitcoin and artificial intelligence. The company is actively pivoting from traditional Business Intelligence (BI) towards AI-powered enterprise analytics. In a conversation between Preston Pysh and Paolo Ardoino, Preston asked Paolo about issuing Tether via the Lightning Network using the Taproot Asset Protocol. Paolo responded by highlighting the necessity for technology capable of supporting 50 billion AI agents within a decade. In his view, only peer-to-peer payment channels could handle this volume, as machine-to-machine transactions are expected to vastly exceed human-to-human transactions.

If Paolo’s vision materializes, who provides the channel liquidity required? Revisiting the fighter jet analogy, perhaps a robust Lightning Network is akin to the turbine engine, AI-driven agent transactions are the jet fuel, and a pro-Bitcoin administration represents the critical aluminum alloy needed for construction.

Ten years from now, Strategy might be among the largest liquidity providers for its own AI agents—and potentially for numerous external AI agents—charging a modest 1% fee for BTC collateral in its channels, facilitating settlement across various digital assets. With this model, the company could easily generate sufficient earnings and cash flow to cover the perpetual dividend obligations of their $STRF and $STRK preferred stock.

Closing thoughts

While rereading this article, I realized I’ve primarily highlighted the positive aspects of this strategy without adequately addressing potential downsides. Reflecting on why, I concluded that it stems from my personal conviction and expectations regarding Bitcoin. Let me explain.

If Bitcoin realizes its potential to significantly shape the future of finance—thanks to its unique properties and characteristics—the annual growth expectations outlined are entirely reasonable. Under such expectations, I believe the latest additions to Strategy’s toolkit are indeed beneficial. They attract larger pools of capital while preserving maximum volatility in the common stock.

However, to be clear, if Bitcoin does not deliver the anticipated growth, Strategy will inevitably struggle to meet its dividend obligations. A lower-than-projected stock price would force the company to issue excessive common stock, resulting in substantial dilution and negatively impacting the overall strategy. Should Strategy ever need to liquidate some of its Bitcoin holdings, it would, in my opinion, mark the beginning of the end.

This leads us back to the pioneering spirit mentioned earlier in this article. What Strategy is undertaking is undeniably bold—and not every pioneer succeeds. It experienced significant success since implementing its Bitcoin treasury strategy. Many companies in its position would consolidate and diversify to secure that success. Yet, "safe" and "secure" are words rarely found in a pioneer's vocabulary. Companies fixated on the What might choose stability, driven by profit and immediate shareholder value. In contrast, companies motivated by a compelling Why, driven by a vision for the future of finance and technology, will likely double down.

As I see it, Strategy will either become one of the most influential companies on the planet or fail spectacularly—there probably isn't much middle ground. Either way, I firmly believe Strategy will be remembered as true pioneers.

Written Sources:

https://x.com/Croesus_BTC/status/1899161281820516828

https://substack.com/home/post/p-159597512

https://coincentral.com/blockfi-review/

https://www.calamos.com/blogs/voices/2025-outlook-global-convertible-market

https://www.strategy.com/press/microstrategy-is-now-strategy_02-05-2025

https://www.strategy.com/press/strategy-announces-21-billion-strk-at-the-market-program_03-10-2025

https://www.strategy.com/press/strategy-announces-proposed-strf-preferred-stock-offering_03-18-2025

https://x.com/LynAldenContact/status/1904207442893787141

https://x.com/Croesus_BTC/status/1902401860914356359

Video Sources:

As bitcoin's role in the global financial landscape evolves, understanding its potential impact on your wealth becomes increasingly crucial. Whether we see measured adoption or accelerated hyperbitcoinization, being prepared for various scenarios can make the difference between merely participating and truly optimizing your position.

This is why Unchained developed the Bitcoin Calculator – a sophisticated modeling tool that helps you visualize and prepare for multiple bitcoin futures. Beyond traditional retirement planning, it offers deep insight into how different adoption scenarios could transform your wealth trajectory.

What sets this tool apart is its integration with the Unchained IRA – the only solution that combines the tax advantages of a retirement account with the security of self-custody. In any future state, maintaining direct control of your keys remains fundamental to your bitcoin strategy.

| A guest post by

|

Great article, this is the best breakdown yet I've seen of MSTR's overall strategy. Thanks for writing it!

Very nice Johan. Its a fun company to think about