Powell's soft pivot, rates reaction

Falling inflation is consensus, and the Fed's goals have now shifted from murdering inflation to achieving a soft landing

Dear readers,

The February FOMC meeting has concluded, and with it, a downshifted rate increase of 25 basis points and another round of Fed rhetoric to be digested by the markets.

Let’s unpack all of the relevant information, dissect the rates market’s reaction, and note the forward market implications as we approach the end of the Fed’s hiking cycle.

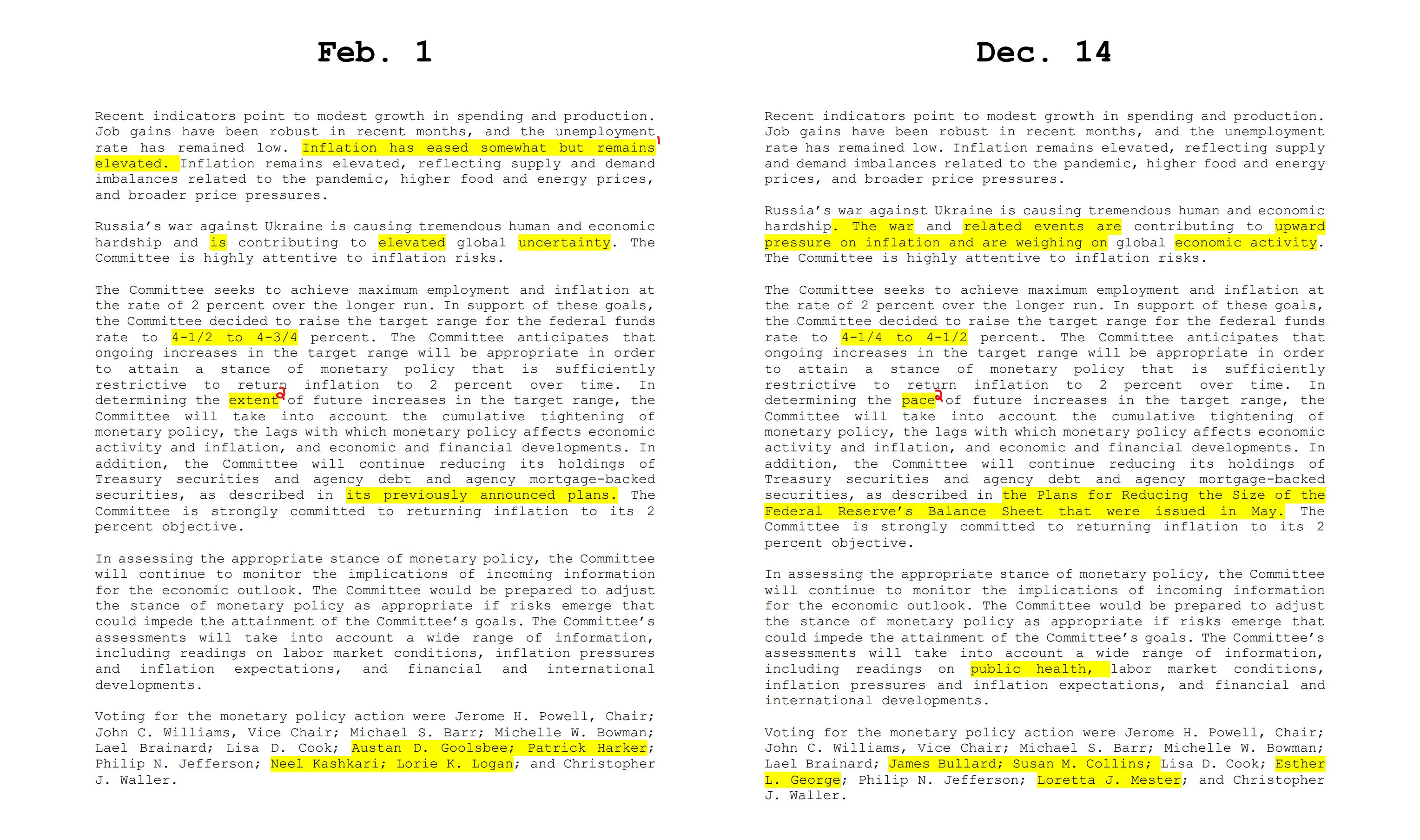

FOMC statement comparison

Allow us to summarize the changes made to February’s FOMC statement released today and the last one from December 14th—two of which are noteworthy for forward guidance:

1.

Inflation remains elevated… → Inflation has eased somewhat but remains elevated.

This is the first time that the Fed has acknowledged disinflation in its written remarks as a committee—only took them 8 months. Inflation near the 10-handle has been defeated, so aggressively that the whites of deflation’s eyes are starting to be seen in negative month-over-month CPI prints. As such, the Fed’s decision-making is now taking the risk of overtightening and unintended deflation into account.

2.

In determining the pace of future increases… → In determining the extent of future increases…

This is the kicker. The switch from the word pace to extent is all you need to take away from this FOMC meeting. As inflation has fallen so materially, the Fed recognizing it, has shifted from “how quickly can we hike?” to “how much higher do we need to go?”