Record-high emergency FHLB loans send alarm bells on bank funding stress: TBL Weekly #42

This year's third bank failure is here. Entering the "longer" phase of the Fed's hiking path plus $95 billion in QT is a toxic combo for cheaply levered players.

Welcome to TBL Weekly #42—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

After slipping on a pile of leveraged-short bananas last week that saw it tumble as low as $27,000, bitcoin has managed to reclaim the $29,000 level. Bitcoin still comfortably sits above its 200-week moving average, a key behavioral support level that has never declined. Bitcoin is a terrific gauge of how risk markets are doing more broadly—we will be monitoring it closely as tensions in credit continue rising, because bitcoin is likely to be the first to sound the alarm about any spillover of lower risk-taking into other risk assets:

Equity volatility is highly compressed. VIX has fallen below the 16-handle, a level not breached in 18 months—despite the extremely low equity volatility, the S&P 500 cannot get out of its stocks-in-a-box range that we’ve been highlighting here at TBL.

The last time that VIX was this compressed, the S&P 500 put in its all-time high. It sunk as low as the 9-handle in the last decade so it may have more room to fall and provide equities with the headroom to clear 4,200. However, we are approaching the top of the box range, which could be rejected and send equities lower. We are closing in on a spicy inflection point for this cycle. Rock? Meet hard place:

In early 2020, many investors watched equities rip higher despite no impetus whatsoever, fundamentally or technically—we now understand the source as central bank liquidity. As financial plumbing seized and signs of global growth sputtered to a halt, equities disregarded all of it. The current vibes aren’t quite the same, but the unique set of circumstances facing equities as credit markets are on the brink of turning imbues risk assets with their own eery, proceed-with-caution vibes all the same.

Houston, we have a problem.

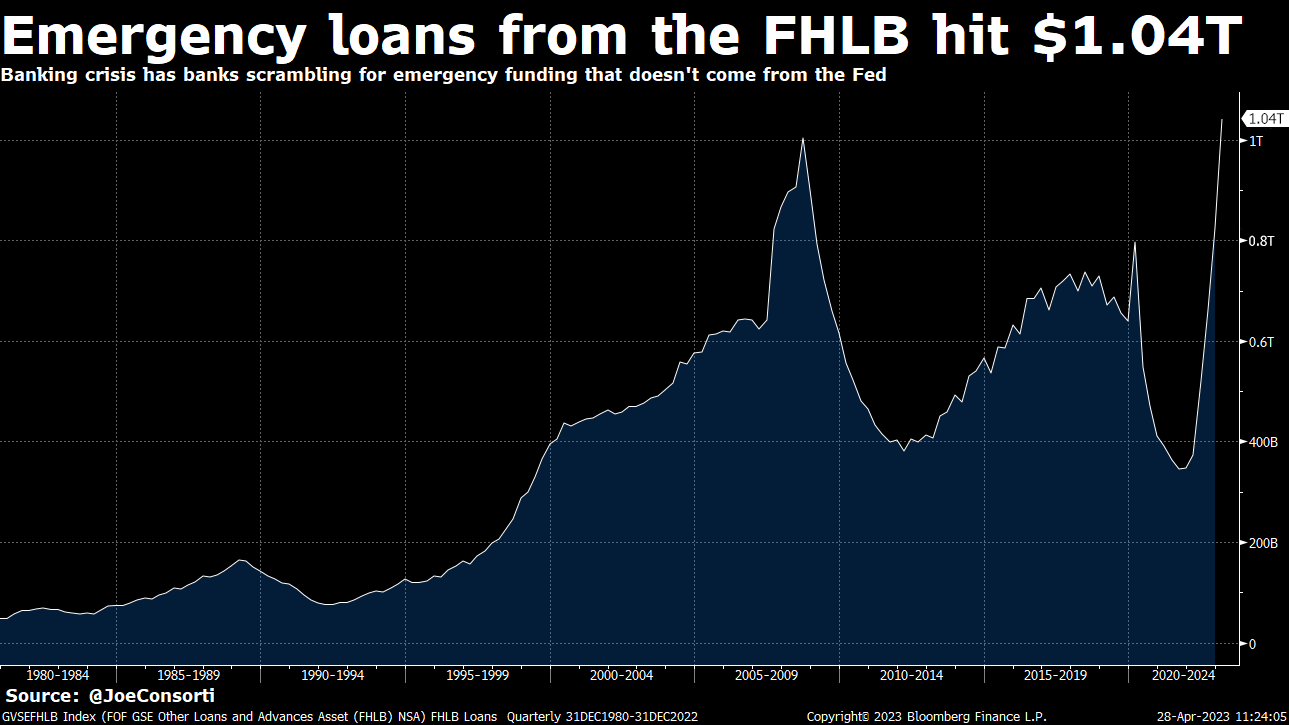

Advances from Federal Home Loan Banks hit an all-time high, according to some modestly lagging data (January to March), as banks rush to bolster liquidity by borrowing from the FHLB, which has less emergency-setting stigma than something like the Fed’s discount window. These emergency loans hit a record $1.04 trillion in Q1, the highest quarterly amount since the Great Financial Crisis.

While a great deal more lagging than weekly BTFP, discount window, and swap line data, it confirms that banks are still seeking emergency cash as funding stress worsens. The all-time high of $1.04 trillion serves to color the severity of the funding crunch banks are faced with:

Despite having a $30 billion liquidity rescue from big US banks last month, followed by borrowing $63.5 billion at the Fed’s discount window, $13.8 billion from BTFP, and $28 billion from Federal Home Loan Banks, First Repub; ic Bank is on the brink of failure. A total of $135.3 in liquidity infusions, and First Republic Bank still couldn’t weather the storm and is on the brink of seizure by the FDIC.

First Republic Bank being taken into FDIC receivership will mark the third large American bank failure this year.

A particularly unsettling fact about the latest bank failure is that First Republic was not a poorly interest rate-hedged bank with a flighty, primarily VC and tech deposit base: it’s just a regional bank that deals largely with wealthy clients. Not exactly the kind of failing institutions that the Fed had in mind when restricting credit.

This isn’t an instance of your flavor-of-the-week tech firm going under because rates are too high. Problems are now hitting regular banks, financial institutions that lubricate economic activity and growth for all of the United States. With how well-capitalized banks are in the wake of the 2008 financial crisis, this simply isn’t supposed to happen. Then why is it happening?

Bank runs can now occur in an instant, even at relatively well-reserved small banks. Present rapidly contracting reserves at these banks as the Fed conducts QT and increasing rates that are destroying the borrow-short-lend-long carry trades that encompass the entire business model of banks, and you have a toxic cocktail that will continue to mow down smaller financial institutions as long as the Fed keeps it up. Regardless of the number of emergency loan facilities created and drawn from, like we’re seeing with First Republic, even tens of billions of dollars aren’t enough to stave off failure for regionals.

The funding situation remains pressed for banks, which means it will continue worsening for businesses and consumers. Higher rates will continue rippling from banks to every borrower in the global economy, and while futile to pinpoint exactly when the tipping point will come, it’s going to get worse before it gets better.

HELP US get Nik’s book Layered Money into the hands of US policymakers!

That’s right, Nik is heading to Washington D.C. with Satoshi Action Fund to hand out copies of the Bitcoin book, Layered Money, to Members of Congress and staffers.

You can fund this Bitcoin book handout at our fundraising page—every $8 is one book in the hands of a policymaker.

Help us orange-pill Congress so we can have Bitcoin-literate leaders!

Stagflation fears emerge in macro, we aren’t buying it (yet)

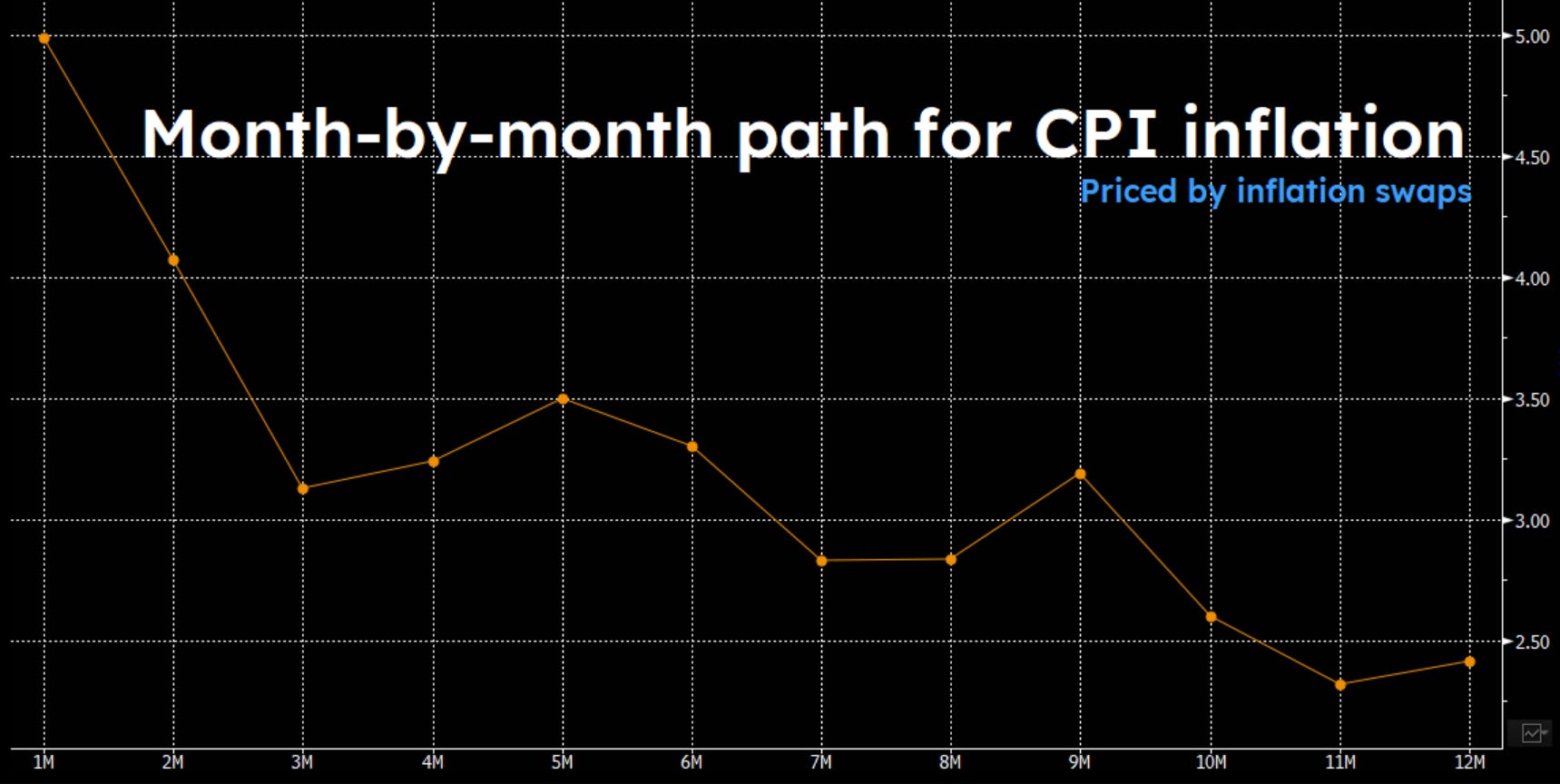

Core PCE, the Fed’s preferred measure of inflation, came in unchanged yesterday on both yearly and monthly resolutions, at 4.6% and 0.3% respectively. Flat inflation data adds to the idea that we could be poised for a minor upward hiccup on the disinflation path, but take a look at inflation swaps, which demonstrate the rate is expected to fall back to the 3% area within only a few months. We aren’t convinced inflation will hang around either:

The weekly jobless claims data has taken on elevated importance recently as it has materially ticked up week after week, now at 17-month highs and flashing a recession signal. People filing for unemployment and remaining on it are everything you need to know about the labor market: it IS unwinding. The percentage of states with continuing claims rising more than 30% has never reached its current level of roughly 18% and not gone on to spike to recessionary levels, per a ZeroHedge report. In other words, the labor market doesn’t gain strength from the state its in today, not until it violently unwinds in the form of a much higher unemployment rate. Continuing jobless claims lead the unemployment rate, and this steady rise in claims is the path you can expect the unemployment rate to take over the next few months:

Yesterday’s flat inflation data coupled with a steadily unwinding labor market have caused parts of the market to flirt with the idea of stagflation.

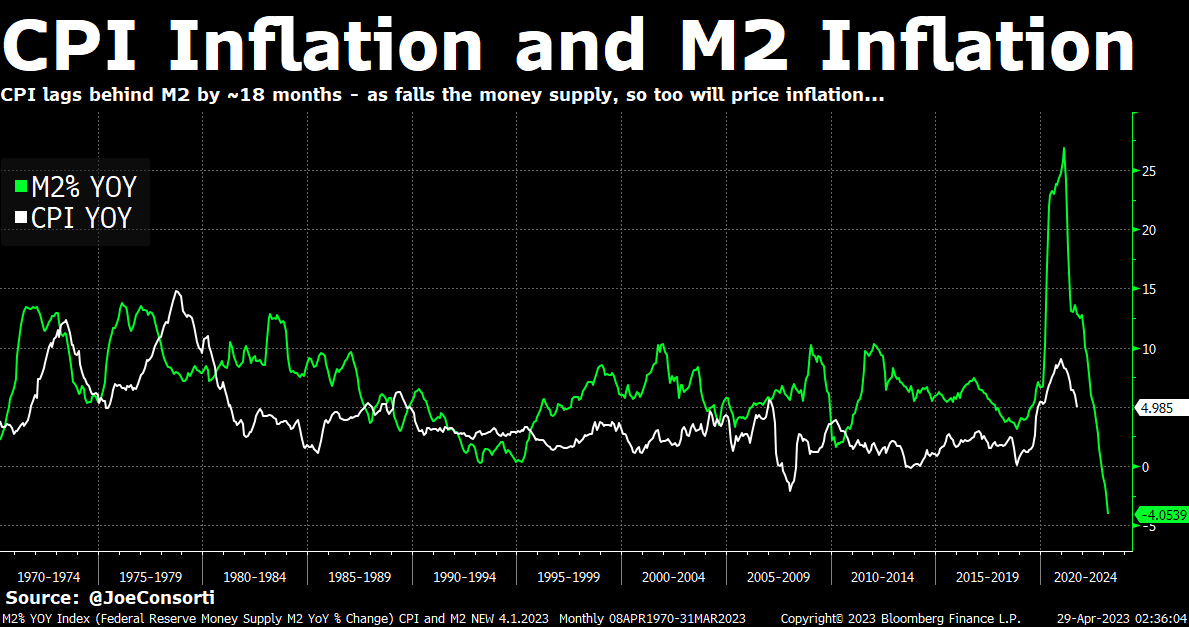

The totality of data doesn’t have us convinced that any perceived stubbornness in inflation will be anything other than a transient phenomenon. The secular trend for consumer and producer prices is still down, following in line with the rapid negative growth of the US dollar money supply. We always maintain our data dependence and will adjust our outlook as new price inflation reports come out, but for now, we maintain that monetary deflation will be followed by commensurate price disinflation:

The Week Ahead

In the week ahead, we look to the FOMC meeting on Wednesday for just how seriously the Fed is treating yet another bank failure, but we also will receive a chunk of top-tier economic data, including ISM Manufacturing, ISM Services, job openings, and payrolls. This will be our first genuine look at the economy in April, and it will give us a real sense if all our recession talk has true merit for Q2:

Don’t forget to join us for live coverage of the FOMC decision on Wednesday!

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are your quick links to all of the TBL content for the week:

Monday

In this episode, Joe breaks down how weak 2022 tax receipts contribute to the already-stressful funding situation for the US government as rates remain elevated and a gargantuan maturity wall is on the horizon. He also discusses how assets will behave, and why the US Treasury market is behaving strangely heading into the deadline.

Check out—The Debt Ceiling Doomsday Is Approaching

Tuesday

We take a pause from our cycle approach to focus strictly on prices. Prices tell a story, so let’s examine what markets are telling us. From our vantage point, it’s time for caution. Nik took a fresh look at all of the weekly candles to craft a story heading into next week’s FOMC meeting and next month’s dogfight over the debt ceiling—using only the pictorial representation of buyers and sellers going at it in the market. We end with a grand takeaway.

Check out—Sell in May and go away? A chart pack.

Wednesday

In this episode, Joe discusses how the credit crunch is progressing in the form of further bank failures as the Fed continues QT, bank lending gradually slowing, both as they derisk and fewer businesses demand loans due to higher rates, and how we are entering the phase of businesses defaulting and going bankrupt.

Check out—Crunch Continues: Lending, QT, Businesses & Bank Defaults

Thursday

We take a break from your regularly scheduled programming to bring you a different kind of analysis.

In such a volatile macro landscape, it’s hard to soar above the clouds at 30,000 feet and view bitcoin as anything other than a high-beta risk asset that is beholden to the everchanging backdrop of Fedspeak, economic data, and the market cycle.

Bitcoin is a macro asset, but it is also the first verifiably scarce commodity and imbues all citizens of Earth with property rights, regardless of whether or not their country of residence honors such basic human freedoms. Let’s take a step back from the macro investor’s chair and observe how bitcoin is advancing in its own right.

Check out—Bitcoin Is Swallowing The World

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our bitcoin and macro recap—have a great weekend everybody!

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

The Bitcoin Layer does not provide investment advice.

Nik,

Thanks again for the great content. In reading TBL, The Informationist, Lynn Alden and more I've come to the conclusion that we know the problem, and the answers, but we don't hold the power. That's why I'm so happy to hear that you will be going to Washington as we need credible people like yourself to educate our elected officials. Thank you for doing that, and yes, I'd like to support your efforts by buying books for my elected officials, Senators John Hickenlooper and Michael Bennet, and Representatives: Ken Buck and Brittany Pettersen.

But I have to ask myself, and your followers, what can I/we do beyond sponsoring a book? My answer is to correspond frequently with my elected officials. So today I drafted a letter that I am sharing below with the hope that we can start a "correspondence movement". Please feel free to share this letter with anyone and encourage them to copy or edit as they see fit to start a "correspondence movement". We are not powerless!

Here it is:

Dear Mr. Bennet,

I'm sure everyone would agree that "good decisions/legislation" requires good information.

This week we are witnessing the failure of First Republic Bank (14th largest bank in the nation) despite 130 billion in capital infusions since the SVB failure in March.

These failures are just symptoms of the structural problems/disease inherent in our monetary system, and there is no more pressing issue before congress than understanding the problem before legislating a solution.

While this link (https://open.substack.com/pub/jameslavish/p/interest-rate-risks-are-collapsing?r=exxlp&utm_campaign=post&utm_medium=email) will give clarity on “interest rate risks” and how they have underscored the insolvency of those banks (and many more to come), the real problem is excessive debt/leverage in our system (public and private).

Here is a link to the Congressional Budget office’s own report that graphicly shows the “discretionary” spending that congress just passed for 2023 https://www.cbo.gov/system/files/2023-03/58890-Discretionary.pdf . How does congress sleep at night knowing that the CBO projected deficit for fiscal year 2023 (based on the first 6 months of data) is going to be 2 trillion dollars.

This type of fiscal deficit comes in the form of debt shouldered by the US tax payer. To be blunt, we are quite literally being monetarily enslaved by our elected officials.

Congress is about to engage in the perennial “debt ceiling” debate, and yet everyone knows that the ceiling will be increased. Why? Because not doing so will initiate a melt down of the world financial system. Such is the burden of being the “world reserve currency” and “world reserve asset”.

Currently there is no choice but to raise the ceiling; however, there is a choice about changing our future fiscal behavior so as to avert the impending debt spiral that is/will destroy our nation.

My first ASK: Please make sure any raising of the debt ceiling is tied to a real budget to constrain/reduce spending. This is the only way out.

My second ASK: Fall on your own sword, be brave, and do what is in the best interest of your constituencies even if that might jeopardize your re-election.

I am asking even as I remind you that you work for us.

Sincerely,

Mark R. Link D.D.S.