Stocks & bitcoin peer over a cliff as the US Treasury is set to refill its coffers

Who's going to buy all of this new debt? Everybody, to the detriment of every other asset class.

Dear readers,

We hope you had a safe, happy, and reflective Memorial Day weekend! As I write this I can finally say that the weather has warmed up for the summer here in New England, a welcome change that brings me closer to Nik’s always-sunny SoCal climate.

The US Treasury’s debt ceiling is close to being raised, again. With a deal now reaching the Senate for consideration before hitting the President’s desk, the question for you, us, and for markets is what happens next?

Well, one of the market’s constant streams of liquidity will stop flowing.

As the Treasury gets the go-ahead to refill its cash account by issuing T-bills, liquidity that was previously invested elsewhere flocks to the now higher-yielding set of risk-free government debt—bank funding and riskier assets like stocks and bitcoin facing the brunt of the outflows in the process.

Let’s analyze previous cycles, explain why liquidity gets drained, and how a negative market response may set up the Fed’s eventual pivot to rate cuts and QE.

Envoy is an easy-to-use Bitcoin mobile wallet with powerful account management & privacy features.

Set it up on your phone in 60 seconds then set it, forget it, and enjoy a zen-like state of finally taking your Bitcoin off of exchanges and into your own hands.

Download it today for free on the iOS App Store or the Google Play Store.

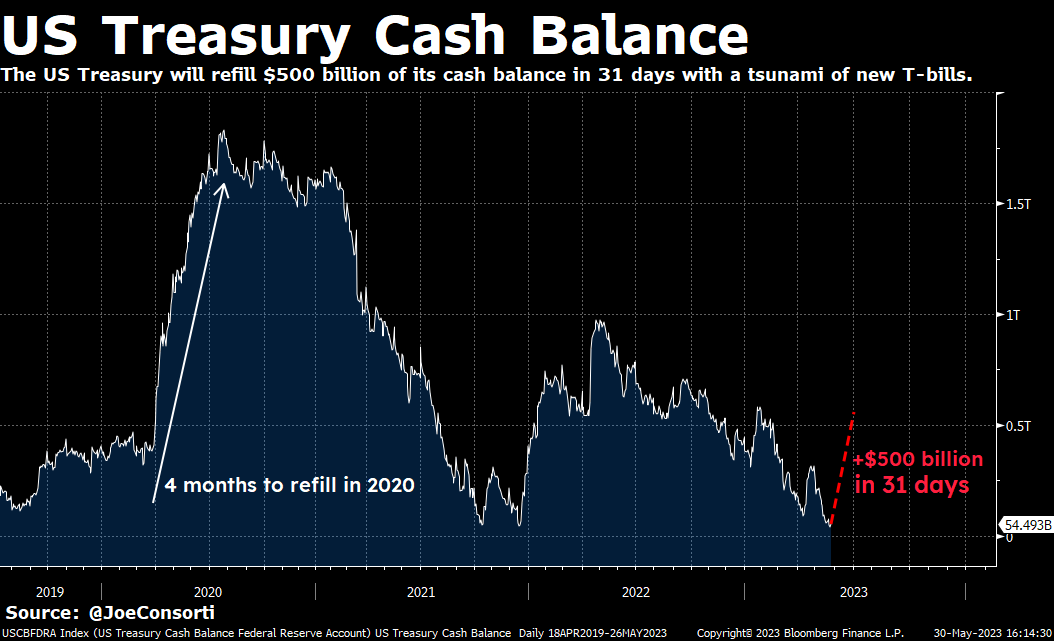

The US Treasury is expected to issue $1 trillion in bills, a form of Treasury debt that matures anywhere from one month to one year and its preferred method of funding, between when the debt ceiling deal is passed and June 30th. It will use roughly half of this funding for expenses and paying interest on existing debt, and the other half to top up its cash balance.

Ignoring the Ponzi-like dynamic of paying off creditors with new debt, the pace of the TGA (Treasury General Account) refill will be lightning-fast. A projected $500 billion increase in one month or less, which is on pace for the refill following the March 2020 market crash, and the refill that coincided with the December 2021 market top:

The timing of the TGA being refilled and drawdowns in the stock market is no coincidence. The two have a negative convexity with one another, with stocks and other risk assets falling as the Treasury’s cash balance rises and vice versa.

To understand why, let’s boil down what the TGA is. Think of the TGA as the US Government’s bank account, and a liability of the Fed, just as your deposits are a liability of your commercial bank. As the US government runs down its cash balance, it spends money into the real economy. When it refills its cash balance by issuing new debt and spending less, liquidity in the market falls because the government is a net borrower instead of net spender, leading to tighter financial conditions, and lowered risk-taking behavior observable in credit, stocks, and bitcoin.

Markets have been the beneficiary of a steady injection of liquidity thanks to the US Treasury spending down its cash balance over the last 12 months, but this is going to flip on its head once a debt ceiling deal is reached and Yellen has the go-ahead to fund itself by flooding the market with fresh T-bills. The bill issuance will remove cash from the system, both from public market investors seeking yield and directly draining bank reserves, exacerbating the impact QT is already having.

The US Treasury’s own estimates released on May 1st outline the roughly $1.5 trillion it expects to borrow over the next two quarters:

During the April – June 2023 quarter, Treasury expects to borrow $726 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $550 billion.[2]

The borrowing estimate is $449 billion higher than announced in January 2023, primarily due to the lower beginning-of-quarter cash balance ($322 billion), and projections of lower receipts and higher outlays ($117 billion).

During the July – September 2023 quarter, Treasury expects to borrow $733 billion in privately-held net marketable debt, assuming an end-of-September cash balance of $600 billion.

Calling back to the Ponzi-like dynamic of interest payments being funded with revenue from new debt issuance, the US Treasury itself stated above that its revenue elsewhere was low and its outlays (interest payments) were higher than expected—this is a problem the Treasury will continue to have in the years to come.

When the US Treasury issues new bills to refill the TGA, it’ll have a 5.25% coupon to match current bill yields—the rate the US is paying now averages 2.11%. The real problem was never the debt “ceiling”, but rather the fact that the cost of servicing its debt is 2.5x higher than outstanding US Treasury debt. As tax revenues continue to disappoint and rates on bills sit above 5%, the source of revenue that the US will have to increase issuance of is simultaneously becoming an ever-larger burden to pay down: