The Party Hasn't Even Started: TBL Weekly #81

Bitcoin's correlation with the S&P 500 tells us that its hallmark bull run has yet to kick off.

Welcome to TBL Weekly #81—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.

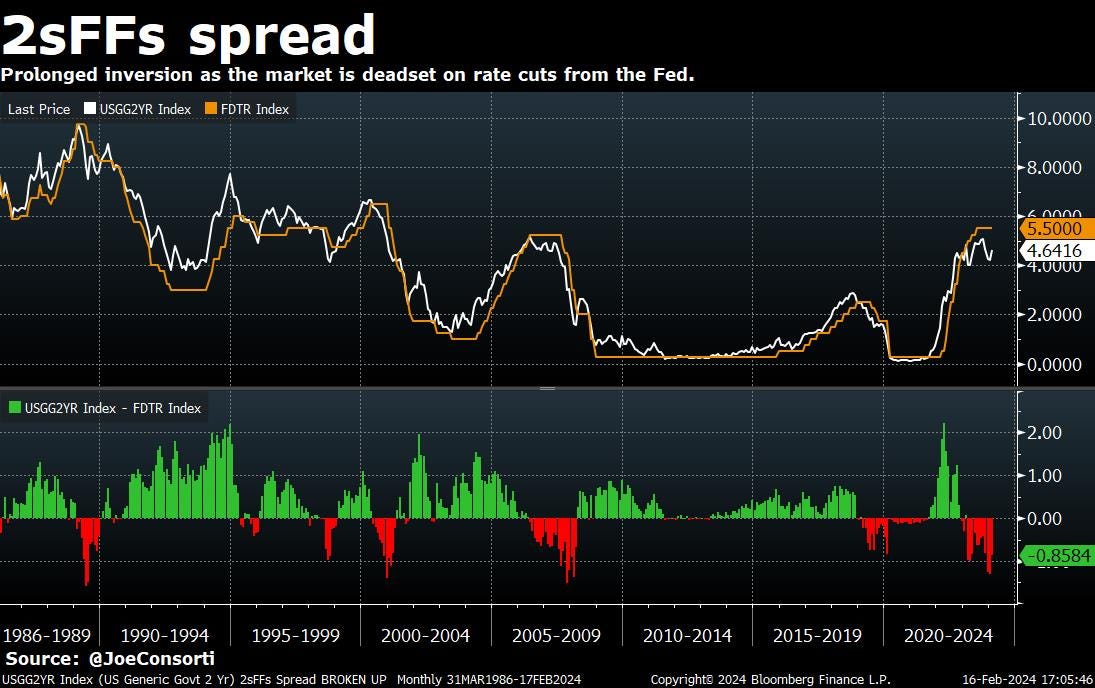

Good morning everybody! The spread between the 2-year US Treasury yield and the Federal Funds target rate has long been our favorite measure of where the market believes the Fed should take rates versus where the Fed has them set. Twos have yielded less than Fed Funds for a total of 14 months now, which is notable because this is the same length of time that 2sFFs was inverted in 2007 before the Fed cut rates, and twice the length that it was inverted in 2019 before the Fed cut rates.

Put simply: despite stubborn core CPI, mixed but still-strong economic data, and a record-low unemployment rate (however many asterisks it comes with), the market is insistent about rate cuts. Core goods and core services were the two parts of CPI that deflated in January, indicative of a waning consumer—perhaps rates are sensing that we’re on the precipice of the first tangible slowdown of the cycle and that’s why they’re unwavering in ‘camp rate cuts,’ despite strong outward-facing headline data:

The S&P 500 ended the week still on its most prolonged rally in recent memory. During the 2020 and 2021 rally from sub-3500 to 4750, stocks had a few bouts of correction in between to take a breath before climbing higher—compare that to what the S&P 500 is doing now, which is an absolute moonshot, and it’s hard not to say that we are due for a correction. The below chart maps bank reserves and the S&P 500. This chart is not meant to display a direct correlation—banks don’t use bank reserves to buy spoos. This chart is meant to show how overextended US equities are relative to the natural level of risk-taking that should be taking place in US financial markets, represented by bank reserves. To be most specific, as the quantity of Treasuries owned by the Federal Reserve increases, it forces banks out of one asset (Treasuries) into another (reserves) in order to make the system more capable of taking risk outside of Treasuries. Through this mechanism, higher reserves are meant to correlate with risk-taking, even if banks are not taking reserves and outright purchasing stocks. Even though reserves have slightly increased this year, a chunk of it has been driven by falling RRP usage, potentially the cause of an altered evolution of this relationship of late. Overextended is the word of the week:

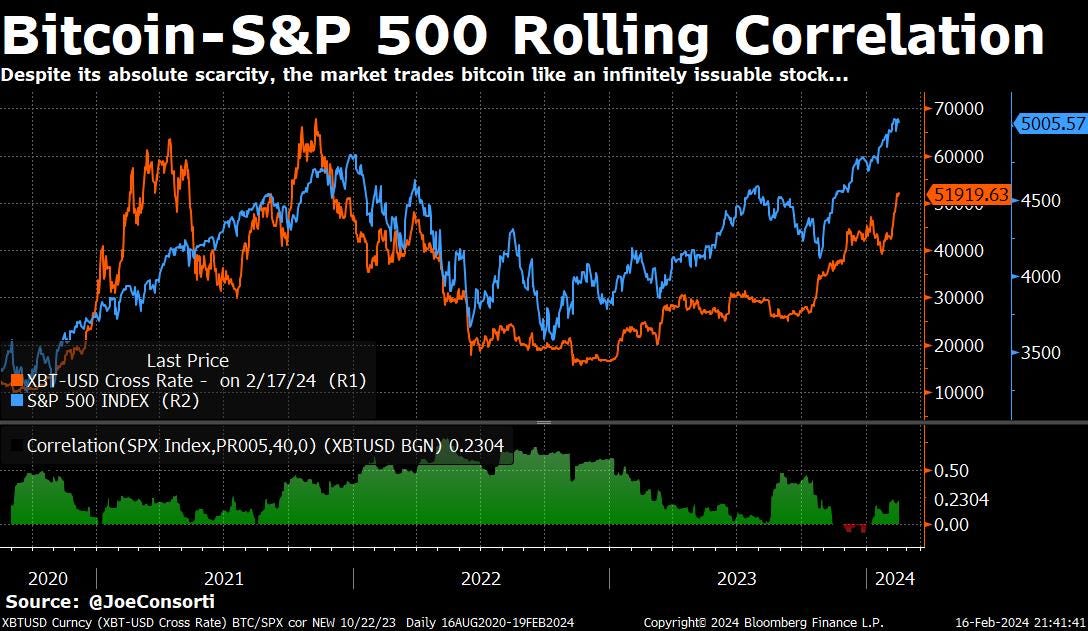

The 40-day rolling correlation between Bitcoin and the S&P 500 has risen to 0.23 from briefly negative at the end of 2023. This rising correlation marks a departure from the typical pattern seen the onset of bitcoin’s hallmark bull runs. Its correlation with the S&P 500 tends to decline as bitcoin’s percentage gains during bull runs far exceed traditional risk assets—even though bitcoin has roared past $52,000, this divergence in traditional correlation patterns tells us that the bulk of bitcoin's hallmark run, when it pulls away from the pack, might still be on the horizon for this cycle. With the halving just around the corner and ETFs currently buying 10 times the amount of bitcoin that will be issued every day after the next halving, bitcoin still has plenty of room to explode if the marketwide risk-taking impulse stays intact:

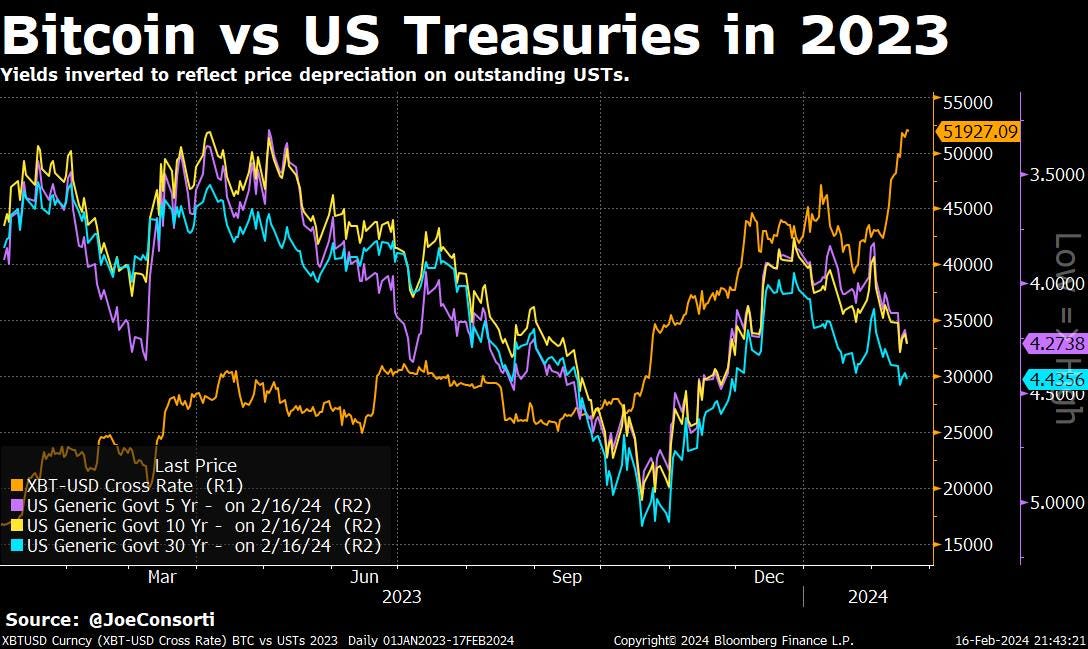

These next two charts offer some 30,000-foot perspective of how well bitcoin has done relative to US Treasuries this cycle. A little bit of fun to close out your morning. Here’s bitcoin versus US Treasury yields, inverted to reflect the secular sell-off they’ve had over the past two years since the Fed started its tightening campaign—this chart demonstrates how impressive the rally has been of late despite rising Treasury yields:

The second chart is bitcoin denominated in the total return of US Treasuries with a 10-year maturity or longer. The ratio between the two is hitting a fresh all-time high every day, currently sitting at 16.44. With ETFs now hitting the street as the Fed fights the inflation monster and devalues outstanding Treasuries in the process, you can bet that people who’ve been burned by the Fed these last two years are now looking at the brand-new suite of instruments int heir brokerage account that lets them gain exposure to this asset. As drawdowns wane with each cycle, capital will continue to shift out of the old and into the new:

Next Week

In the Presidents’ Day-shortened week ahead, we look mostly away from economic data, which will be thin, toward how risk assets respond to yet another round of pushed back Fed easing. Read: higher rates, however temporarily. With June several months away—when we are expecting the first cut—banks and other market participants will be forced to deal with 5%+ funding rates for another few months. Loan loss provisions are on our mind of late, therefore anything affecting banks’ ability to fight to see another day grabs the outsized proportion of our attention.

What are some of the factors that affect how banks fund themselves? The foremost factor is the performance of the bank’s assets. Rising interest rates can damage value, but the threat of future defaults matters much more. So anything that drives such a dynamic is worrisome, such as another round of office building liquidations. Another factor is the quantity of wholesale funding in the system—cash available to finance Treasury positions in the repo market. If money market funds are flush with cash, banks shouldn’t have too much trouble financing auction takedowns. That is, however, unless the Treasury is issuing securities faster than the market can take them down. This won’t cause failed Treasury auctions, but it could cause bank funding issues and spills in other riskier markets. The market handled another QT week (15th was a QT day) with jitters, but not unscathed.

A final factor for banks to discuss today is the quantity of deposits in the system, another way to fund activity outside of wholesale repo. Deposits can decline in search of higher yield, which can be available via money market funds. In this way, retail funding (deposits) transforms into wholesale funding (repo), but the transition can affect some banks more than others. With so many excess reserves in the system via QE, the balance between reserves, RRP, T-bills, and deposits means that one participant or another is always subject to balance sheet disruption when QE is reversed, especially smaller players. More boring economic weeks, including those also without major Treasury auctions like next week, end up being opportunities to focus on monetary mechanics. We tend to do that a lot, so that no matter the calendar we can provide value to you, the reader:

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are some quick links to all the TBL content you may have missed this week:

Monday

In this episode, Michael Howell, CEO of CrossBorder Capital, returns for a rousing discussion on his global liquidity framework. He talks about why 2023 played out according to his framework, why the end of Q1 could get dicey for financial markets, and while the bull market rages on and the party continues, why dancing near the door is your best bet.

Check out—Debt Monetization Is Coming, Hard Assets Are The Hedge | Michael Howell

Tuesday

After a year of tumult followed by a year of choppy upward price action, we stand before you after a multi-month rally and present our case for why $100,000 bitcoin in 2024 is not as absurd as it first sounds. Moreover, it is a possibility sooner than you might think. At The Bitcoin Layer, we don’t have to be shy about a bullish setup we haven’t seen since 2016, when the CME was about to launch bitcoin futures and developers were working on a Segregated Witness upgrade to bitcoin’s protocol that would allow for the launch of Lightning Network. Today, we’ll look at bitcoin’s cycle, effects of the Fed, institutional flows, bitcoin derivatives markets, and on-chain analysis to determine just how bullish the current setup appears.

Check out—$100k Bitcoin Is Closer Than You Think

Wednesday

In this episode, Nik speaks with Alyse Killeen, founder of Stillmark and investor in bitcoin and Lightning Network companies. We learn how Alyse is currently approaching the Lightning Network ecosystem, including her thoughts on stablecoins on Lightning, how Lightning has reinvented the design and user experience of bitcoin, and how this cycle's approach to second layer solutions differs from the past.

Check out—Growth On Bitcoin & Lightning Is EXPLODING | Alyse Killeen

Thursday

Bringing it back to the fundamentals for bitcoin can feel foreign to some—without coffeehouse adoption or any cashflows to speak of, most don’t associate bitcoin with the term fundamentals. Many couldn’t even articulate what underpins its value. Something about decentralization, we imagine.

But this type of thinking around bitcoin as purely a speculative asset is now ancient. A more sophisticated analysis recognizes $1 trillion in market capitalization and deduces that bitcoin’s value comes from those willing to mine it and those willing to purchase it: a desire to trade computing power or bank deposits for bitcoin transformed the digital collectible to a full-blown commodity, and what people assume its value to be when they send or receive it defines, more than anything, what it is worth. In on-chain analysis, we call this realized price, a metric distinct from the market price that just soared above $50,000. Bitcoin’s realized price is also on the move, and it’s the strongest signal of all. I’ll explain what that means, with some closing thoughts on rates.

Check out—Pent-up demand sends bitcoin soaring past $52,000

Friday

In this episode, Nik is joined by Matt Dines, CIO of Build Asset Management. Matt walks us through the latest in the troubled banking sector, including how commercial real estate losses will trickle down throughout the world. We also take a look at some long term charts of the dollar and US Treasury yields to understand the United States position under perpetual deficits and sky-high debt levels. We conclude with Matt's opinion that the last excuse to buy bitcoin at asset managers is now gone.

Check out—A Global Banking Crisis Is The Endgame

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.