U.S. Treasury Wraps Up Buyback Trials: What's Next?

With buyback trials completed, the U.S. Treasury is ready to unclog the “off the runs” from its debt distribution pipes. Dissecting the plan.

This guest post on the Treasury market is courtesy of Matt Dines, Chief Investment Officer at Build Asset Management. This is neither investment advice nor a solicitation for investment.

The U.S. Treasury recently completed trials for its debt buyback program that has been on the public’s radar since 2022. During the practice run over three weeks in April, the Treasury successfully executed on the repurchase of $600 million of its older “off the run” bonds from its primary dealers (the large bank wholesalers tasked with finding buyers every week for the Treasury’s new debt). These primary dealers are the key intermediaries that facilitate the movement of capital in the dollar-based global financial system. Once that blockage is cleared from dealers’ balance sheets, the steady and heavy flow of new Treasury debt on the horizon (driven by the relentless government deficits that show no signs of letting up) can proceed ahead as planned – or at least that’s the hope. With the initial trials completed, watchers now expect the program to ramp up to $30 billion in repurchases every quarter beginning in May. As this process unfolds, expect the downstream impact from this catalyzing event to be felt throughout financial markets in the quarters and years ahead.

In the current situation, think of the primary dealer like a retailer anxiously awaiting an onslaught of new deliveries from its most important supplier, while at the same time its store shelves and warehouses are already chock full of the supplier’s older merchandise that is not selling. Following the post-COVID glut of Treasury debt issuance and sharp rise in interest rates over the last few years, that is essentially the situation bond dealers face with their supply of old Treasuries. And for the foreseeable future, the supplier does not have the choice to let up on its production: Treasury debt issuance must continue to run heavy to fund existing spending commitments on healthcare, Social Security, defense, and the interest expense on already existing debt. Somehow the old inventory must be cleared out to make room for the new. At the current crossroads, the retailer and supplier have decided for the supplier to buy back its unsellable inventory at the current market price as their solution.

The last time the U.S. conducted a buyback program in the early 2000s it operated at a fiscal surplus (it took in more money than it spent). Under those conditions, the buyback program was a choice. This time around, the buyback program can be considered more like a requirement for maintaining business as usual. The financing for today’s buybacks will come from further borrowing as opposed to the fiscal surplus, which carries entirely different implications. Its cleanout of the excess “off the runs” will free up capacity in dealer balance sheets and money markets, paving the way for capital markets to elastically expand and absorb the incoming new issuance. Ultimately, that expansion will find its way through the financial system and into the private sector: households and businesses in the U.S. will have to adapt and deal with the repercussions over the years to come.

How we got here

Most of the “off the run” bonds causing blockage on primary dealers’ balance sheets were issued during the post-2008 era of heavy central bank intervention and zero interest rates. The arrival of the COVID-19 pandemic in early 2020 shocked markets and shifted the financial system onto a new course. The unprecedented wave of fiscal and monetary stimulus policymakers brought in its wake delivered the massive issuance of Treasury bonds at ultra-low coupons that has ultimately resulted in today’s glut.

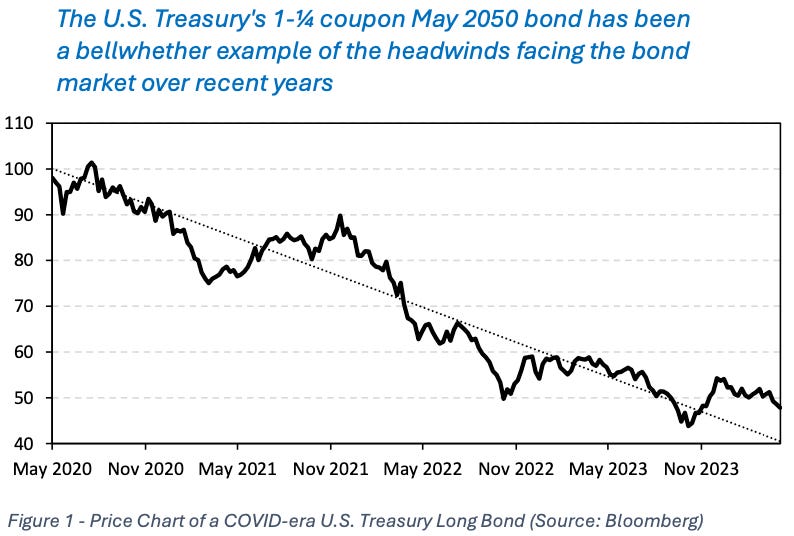

In hindsight, markets and the economy tried to tell policymakers that they had run into a major systemic boundary constraint: prices in the U.S. and other developed economies surged for the first time since the 1970s. While commentary fought over the use of the word “transitory”, bond markets followed through on the price level surge with a historic selloff of a magnitude seen on only a handful of rare occasions in the history of the United States. In an extreme example, the U.S. Treasury issued its 30-year bond at a 1 1⁄4 coupon in May 2020 (the lowest coupon on record for this auction). As a bellwether for the broader struggles in U.S. Treasury debt issued during this era, the price of that bond has consistently declined in recent years and has recently traded as low as 43 cents on the dollar. Several other Treasury bonds from this era have followed a similar course.

Those discounted bonds are now an impediment as the Treasury seeks to raise further debt from capital markets to fund itself in the coming quarters. As capital markets have reset to the new higher cost of capital under this new regime, those “off the run” bonds have found themselves out of favor: their associated coupons offer lower levels than the market now demands. Their increased volatility and declining prices also make them sub-optimal for use as collateral in the “repo” funding markets where large financial institutions go to finance their balance sheets on a short-term basis. These flaws mean bigger haircuts and more frequent collateral calls. While still technically counted among the perceived “risk free” assets at the core of the dollar-dominated system, the U.S. Treasury’s newer minted, higher coupon issues are a more favorable choice from both the borrower and lender’s perspectives. At the margin, no participant wants to buy or lend against the old debt while the new issues are readily available. The old bonds sit and gather dust on the shelves, which grow ever more expensive to inventory under the higher prevailing interest rates.

Public-sector debt implications

From the Treasury’s perspective, clearing the dealer’s inventory problem should help their distributors absorb the future supply of new bonds that will be coming online in the auctions ahead. Presumably, they will then be able to distribute that new debt into their client base. Further supply of higher coupon Treasuries would also improve the overall quality of collateral supply in funding markets, directionally increasing the liquidity profile within the system. Just strike the rock with thy staff, as God instructed Moses in the desert, and hopefully the water will flow.

It is also worth briefly mentioning that the buyback transactions come at a fiscal tradeoff for the U.S. Treasury. As interest rates have risen since the target bonds for repurchase were issued, the Treasury is buying back old debt at a significant discount. Effectively, it will realize a profit on each debt issue’s round trip from selling high and covering their shorts at lower prices. From this positive contribution effect, the Treasury was able to reduce the government’s outstanding debt by over $90 million after buying back $600 million of existing debt at a discount. Initially, this program will have a slowdown effect on the growth of the Treasury’s outstanding debt.

But there is a downside in the longer term. As noted previously, the Treasury is now utilizing borrowed funds to buy back its existing debt. Because interest rates have risen, the Treasury is retiring debt carrying a lower total cost of interest and replacing it with new issues of higher coupons. If each Treasury that was bought back in the April trials was financed through borrowing at its same auction issue (or “rolled” in bond market terminology), this would add roughly $120 million in incremental interest costs for the federal government in future years. If the Treasury continues to fund itself via deficits refinanced at higher interest rates for the foreseeable future, those incremental costs of future debt service will continue to outweigh the immediately realized benefit from buying back its existing debt at a discount. Over time, that leads to a worsening financial position. But if the objective is to simply kick the can down the road (as is often the case), this trend can continue so long as a rising interest rate environment persists.

Medium-term economic and financial market impact

For near- to medium-term effects, look for an eventual return to expansion to both bank balance sheets and money market capacity as the buybacks scale up beginning in May. The new Treasury supply will increase the pool of available collateral in funding markets, which will ultimately seek to work its way through the financial system unless sterilized. Eventually the public-sector driven credit expansion will make its way into the private sector via increased growth in credit and lending.

These effects may already be presenting themselves. As has now been apparent in the economic data for several quarters, both nominal and real growth in the U.S. economy have shown a tendency to come in hot. Since the unexpected back-to-back negative GDP prints in the first half of 2022, final GDP numbers have exceeded survey expectations of professional economic forecasters by an average of 50 basis points per quarter. Recently, CPI data has demonstrated a similar trend with an unexpected pickup during the first three months of 2024. Alongside the hot GDP statistics, perhaps price levels are providing another indication that the public sector debt-driven flywheel is already gathering energy and momentum.

Major transitions in longer-term economic cycles are often difficult for policymakers to identify and adjust course against in real time. Relative to recent cutting cycles, expect the current environment to present a more challenging set of circumstances for policymakers to identify a proper calibration and policy mix than prior experience. Once an economic slowdown does eventually reveal it- self, look for a positively sloped yield curve to re-materialize as bond markets encourage further private sector credit creation to kickstart the economic engine into growth through the financial channel. That normalization could come from policy rate cuts from the Federal Reserve on the front end, further selloff in the long end, or some combination of the two. Appreciation for this unfamiliar and rapidly evolving dynamic between the public debt situation, the economy, and the broader financial system is a critical attribute needed from policymakers at this juncture.

In the quarters after a yield curve normalization occurs, markets and policymakers will find out whether their experience hitting the inflationary constraint following the COVID-19 fiscal and monetary policy deluge was a one-off event or the first encounter with the new normal. It will be difficult to know ahead of time how much of the upcoming growth in the U.S. economy will be attributable to a real increase (rising standards of living) or an overall rise in price levels (a follow-up wave in the inflationary dynamic). A conservative approach would hope for the former while preparing for the latter.

Today’s central bankers find themselves facing an unfamiliar environment remarkably different to what they have experienced throughout most of their careers. Contradicting the dominant trend of the past four decades, headwinds to achieving their stated 2% price stability objectives are now the norm rather than the exception. As the public debt situation continues to provide a root cause that threatens their stable price mandates, watch out for centrally-driven credit rationing policies to become an increasingly tempting tool in the technocratic framework (with China’s state-directed quantity targeting model offering an extreme end of the spectrum). In that direction, look for the technocrat’s price level-based definition of inflation that has dominated the central banking model in developed economies since the 1980s gradually cede ground to the monetarist’s supply-based paradigm and its associated prescriptions.

The recent economic data is suggestive of elevated growth potential and nascent demand embedded in the U.S. private sector relative to its competing developed markets. With the domestic banking system facing the continued obstacle of financing the U.S. Treasury’s deficits, watch for the ongoing trend of capital formation and economic growth facilitated through private market channels to continue. As the emergence of the private equity and credit industries has shown in recent decades, borrowers and lenders will continue to experiment with new solutions through trial-and-error while operating in a credit-driven framework that’s increasingly crowded out by the public sector’s excess. In this macro environment, do not overlook the continued emergence of Bitcoin as a novel, competing collateral base layer -- whose characteristics and properties uniquely achieve the needs and requirements between counterparties in facilitating lending transactions.

| A guest post by

|

Wow! Mind blown! Has this ever happened before (issue high interest rate debt to buyback lower rate, discounted debts)? The financial chicanery never ceases to amaze.