Corporate default rates rise, Bitcoin slips on a banana peel: TBL Weekly #41

Rising borrowing stress is leading to defaults among corporate borrowers. Bitcoin pukes out ten-days-worth of leverage to move back under $30,000.

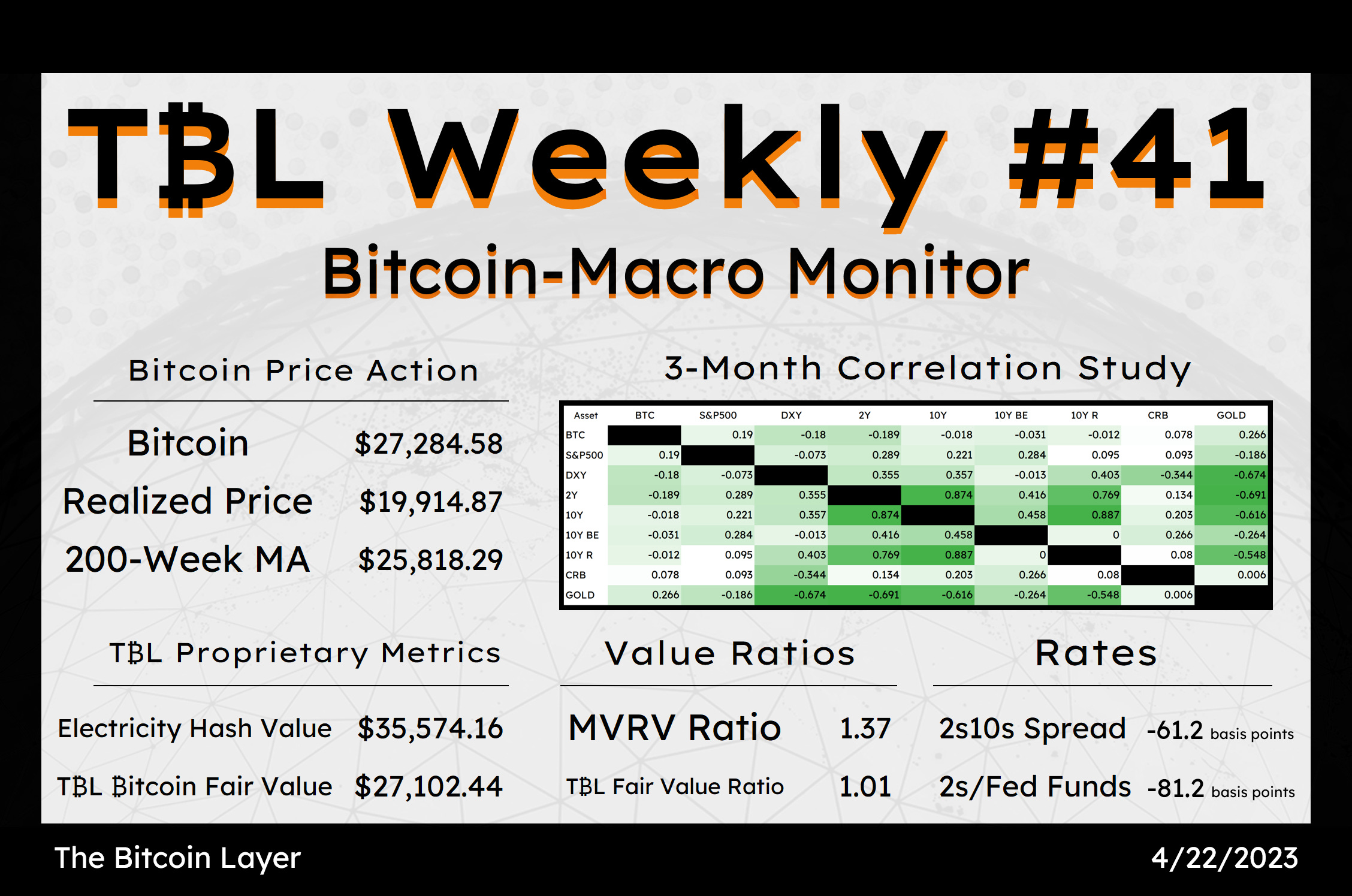

Welcome to TBL Weekly #41—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

Lending and credit creation are slowing for corporates

Key economic data this week was yet another mixed bag, rounded out by stronger-than-expected releases of S&P Global PMI survey data in both the manufacturing and services sectors. While the strong surveys surprised us, we are undeterred by the secular downtrend of economic weakness when looking at the data from 30,000 feet. Economic policymakers recognize the contraction too:

“If tighter financing conditions are a significant headwind on the economy, the appropriate path of the federal funds rate may be lower than it would be in their absence” — Lisa Cook, Federal Reserve governor

They are indeed starting to become a significant headwind for the economy. Businesses are finally digesting a higher cost of capital, after a several-month lag.

There was a slight rise in total US bank lending this week of +$14 billion up to a total of $12.089 trillion—still well off its high but now trending off its March lows, not deteriorating at a rapid, crisis-level pace just yet:

Headline lending is rising but conditions are rapidly souring under the surface. PacWest Bancorp is selling its lender finance division, as the regional bank reels from the collapse of SVB and the slow-motion bank run for regional banks that has ensued since. It has a $3 billion loan book, with revolving credit lines and loans to small businesses and commercial real estate firms. Last month, it had to shore up liquidity after 20% of deposits left, leaving it scrambling to find enough cash to meet its obligations.

This decline in credit and loan creation is translating into tighter lending conditions for US businesses and a deleveraging of the economy, either via repayment & downsizing or default.

In a subcomponent of TBL’s highly valued NFIB survey (small business optimism), we observe 9% of small US businesses that borrow frequently are reporting that financing is harder to get than last month—the highest amount of small businesses having rising difficulty getting loans since late-stage Great Financial Crisis in 2012:

Default rates are starting to tick up at the margin (light blue line), as credit spreads that lower-quality borrowers pay are widening, albeit to levels shy of last year:

Google has halted construction of its 80-acre San Jose mega campus spanning 7.3 million square feet of office space, with no plans to revive the project in the near future. This is not a good sign. The reasons cited are the diminishing need for physical office space, slowing ad sales (a sign of recession), and tighter financing conditions that make projects like this, which were greenlit in 2021 when rates were closer to zero, impractical and untenable. Google, like other rate-sensitive tech firms, has already eliminated 12,000 jobs, some 6% of its workforce, and will incur some $500 million in associated costs on its wider mission to cut back in-construction and already-operational office space.

Are you in desperate need of a bitcoin 101? Catch Nik in Los Angeles for “Bitcoin & The Future of Money” on April 29th for a bitcoin bootcamp to bring you up to speed!

Bankruptcies are beginning to occur at small, private companies—the average number of these firms filing for bankruptcy has spiked past 2020 levels:

And last but not least, consumer delinquencies are beginning in earnest as well. When bank lending dried up, it was only a matter of time before the domino effect of tighter credit reached businesses and consumers. We are now witnessing both face the harder-financing music rather quickly, as US banks wrote off $3.4 billion in bad consumer loans and credit in the first quarter of 2023, up 73% from the quarter previous:

The cracks are beginning to appear. In our credit-based economic world, lower loan growth means lower economic growth. Lower growth is corroborated by commodity prices, all of which remain in their secular downtrend signaling falling global demand and economic activity.

As inflation in the UK remains above 10%, there is a decidedly different tone in the United States, where inflation may uptick next month by a few tenths of a percent, but again, the secular trend is still down—as an illustration, the upper bound of the Federal Funds rate is now neck and neck with inflation, both sitting at 5%.

The narrative for markets has now shifted from ‘how high will the Fed take it?’ to now that inflation is decelerating on schedule, ‘when will the Fed perform maintenance cuts?’—maintenance cuts are when the Fed cuts rates as inflation falls so that real yields don’t rise too much, leaving no more than a 1.5% to 2% gap between its policy rate and CPI inflation.

Judging by rates’ close on the week and Fed Funds futures pricing in definitively one final 25-basis-point hike at the May 3rd FOMC, it’s safe to say that we will get one more for the road. Then, we’ll experience an on-hold period, allowing the economy to deleverage until we reach a breaking point in the labor market or real economy that forces the Fed to move rates in the other direction.

As for bitcoin, all of the leverage that was present in its rally that sent it above $30,000 has been purged from the market. In just 10 days, $1.8 billion worth of futures contracts came into the market and helped fuel bitcoin’s rally, then slowly deteriorated and sent bitcoin’s price right back down to square one:

Here is another look at the price action that looks like Bart Simpson’s hairline—note the massive short liquidations 10 days ago, followed by $45.8 million in long liquidations just 10 days later:

The Week Ahead

In the week ahead, we look to our trusted S&P CoreLogic nationwide housing data, which is now showing an estimate of a small annual decline for the first time 2012, when housing prices finally turned positive after a half-decade of turmoil. Let’s say that a different way—the housing market, which has seen monthly price declines for almost a year, is about to transition to annual declines for the first time in a decade. FOMC members might have their head in the sand, but we don’t. Annual home price declines are terrible preconditions for the wealth effect, consumer spending, and the country’s employment scene—don’t forget that 25% of the US economy is related to the housing market.

We will mostly look past the lagging 1Q GDP data and instead focus on the weekly claims data, which has shown a consistent rise in the joblessness scene in April. The week will go on without any Fed speakers, bless our ears, as the FOMC enjoys a quiet period before convening the following week. The market has essentially already locked in the next rate hike, and any drama in the markets will most certainly come from non-Fedspeak, non-data sources.

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are your quick links to all of the TBL content for the week:

Monday

Joe sits down with Seth and Bitcoin Q+A from Foundation Devices. They break down the mass exodus of bitcoin from exchanges, why more people are starting to take an adversarial approach to how they purchase and store their bitcoin, the serious risks posed to keeping your bitcoin on an exchange, and simple cold storage options that you can start TODAY with nothing but your smartphone.

Check out—Exchanges Are Not Safe | Protecting Your Bitcoin 101

Wednesday

Everywhere you look, it’s dedollarization. Headlines and narratives, of course. Because on the ground and within the banking system, it seems that all anybody wants is dollars. How realistic is dedollarization, though? Not very, especially when you look at the hard numbers.

In Wednesday’s post, Nik explores how hopes of a euro-, yuan-, or gold-centric monetary system are intangible. We’ll also explain how bitcoin adoption is the only competitor with promising, albeit early, momentum.

Check out—Dollar Challengers: Euro, Yuan, Gold, and Bitcoin

Thursday

Nik walks through the runs through the popular alternatives to the US dollar, and explains how each of their drawbacks precludes them from displacing it as the world's main reserve currency, while bitcoin holds a lot of promise for the future.

Check out—The US Dollar Isn’t Going Away

Debt ceiling doomsday is almost here, again. For the 7th time this decade (seriously), the US government is approaching its proverbial debt ceiling, when the choice will have to be made to default on its debt obligations to global US Treasury holders or raise the roof by a few trillion dollars more.

While we all know that this is a sham and the inevitable decision will be to raise the non-existent limit, weak April tax revenues and a looming maturity wall are piling onto the funding stress for the US government, and intensifying the marketwide liquidity drain that will soon turn into a headwind for asset prices. Joe breaks it down.

Check out—A tax day for ants causes more stress for the US Treasury as debt ceiling D-Day nears

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our bitcoin and macro recap—have a great weekend everybody!

Passport is the Bitcoin hardware wallet you already know how to use. With a gorgeous design and familiar interface, Passport makes it easier than ever to self-custody your Bitcoin. No more sitting at your computer or squinting at tiny screens. Passport seamlessly connects to your phone, empowering you to quickly view your balance and move Bitcoin in and out of cold storage.

See what best-in-class Bitcoin storage feels like at thebitcoinlayer.com/foundation

& receive $10 off with promo code BITCOINLAYER

The Bitcoin Layer does not provide investment advice.

https://youtu.be/qQ_0OJzz81M Your thoughts on the increased fixed income offsetting reduced lending? It seems that income is a small percentage in comparison the loan creation which is exponentially leveraged.

this week's guest on Market Huddle youtube channel brought the fact that - sure lending is decreasing, however, higher rates are providing a higher income to savers. I for one as a recently "semi" retired individual am focusing on fixed income and dividend stocks. Our local bank, State Bank of Southern Utah, recently offered 1 year CD's at 4.25%. This is at least helping to offset the truly run away inflation we are experiencing.