The Fed Is Planning To Force Healthy Banks Into Loans They Don't Need: TBL Weekly #77

Welcome to TBL Weekly #77—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.

Good morning, everybody!

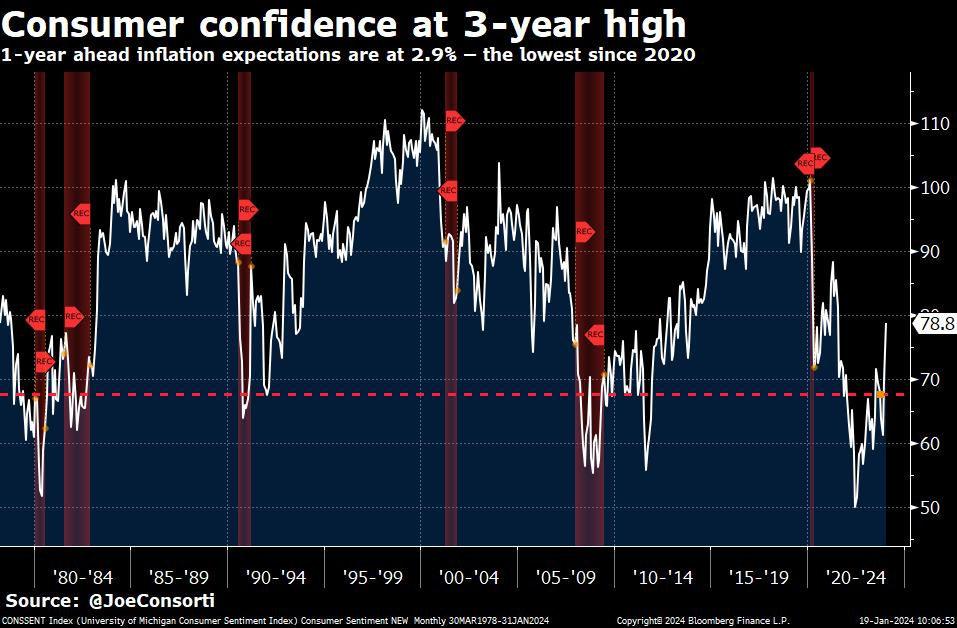

Consumer sentiment, as measured by the University of Michigan, soared to a 3-year high yesterday morning off the back of renewed economic confidence:

This data clashes heavily with the prevailing narratives of high prices that continue accelerating and high interest rates. Yet, interestingly enough, the two main reasons cited for the surge in economic confidence were the expectation that both price inflation and interest rates would fall in the coming year.

Year-ahead inflation expectations came in at 3.01%, down to their pre-pandemic level. Even though they are higher than where the Fed would like them to be, they are now anchored in familiar territory for the first time in three years:

We know that consumers’ excess savings from pre-pandemic are wearing thin and that credit card debt is at or near all-time highs, but it seems that Powell’s rate cut portending has spurred hope across all markets that looming refinancing of revolving credit will be saved by lower rates in the coming months.

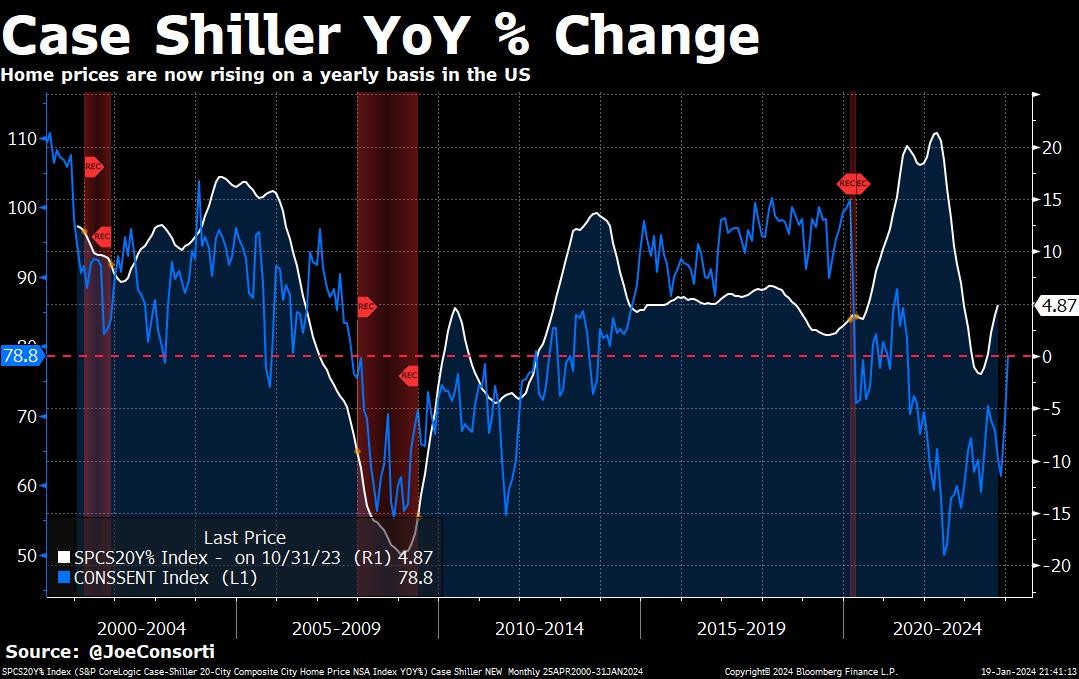

This disparity could also be due to asset prices, which consistently move in line with consumer confidence. See this displayed in the Case-Shiller year-over-year home price changes with consumer sentiment laid on top of it. With the S&P 500 hitting its first all-time high in two years and national average home prices on the rise after briefly deflating, it’s no wonder that consumer wariness is easing. Let’s also not forget that GDP remains well in expansion territory:

The wealth effect is positively reinforcing, too. As people’s perceived wealth rises via rising asset prices, they spend more, driving asset prices up further, rinse and repeat—a helpful process if it helps to soften Powell’s tight financial conditions, but a hurtful process if it undoes those tight financial conditions and reignites price inflation.

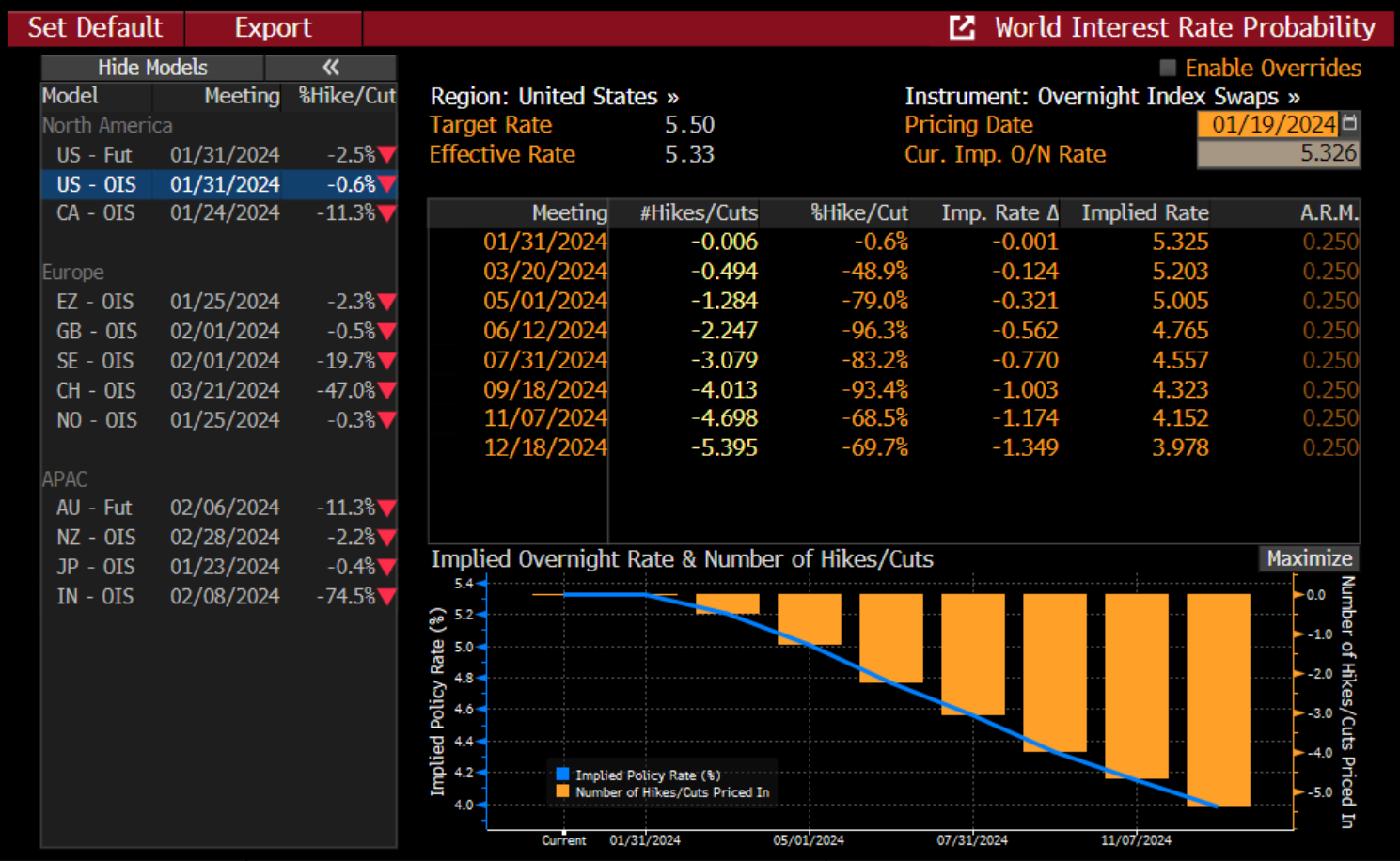

Another reason for the confidence surge is the expectation of rate cuts, which has been fully digested by market participants who see effective Fed Funds below 4% by the end of the year:

This is good, as it provides Powell with room to push back against the expectation of overly loose conditions while still delivering cuts to not scare the market about overtightening. A sweet spot of ~100 bps worth of cuts should do the trick here, in our view.

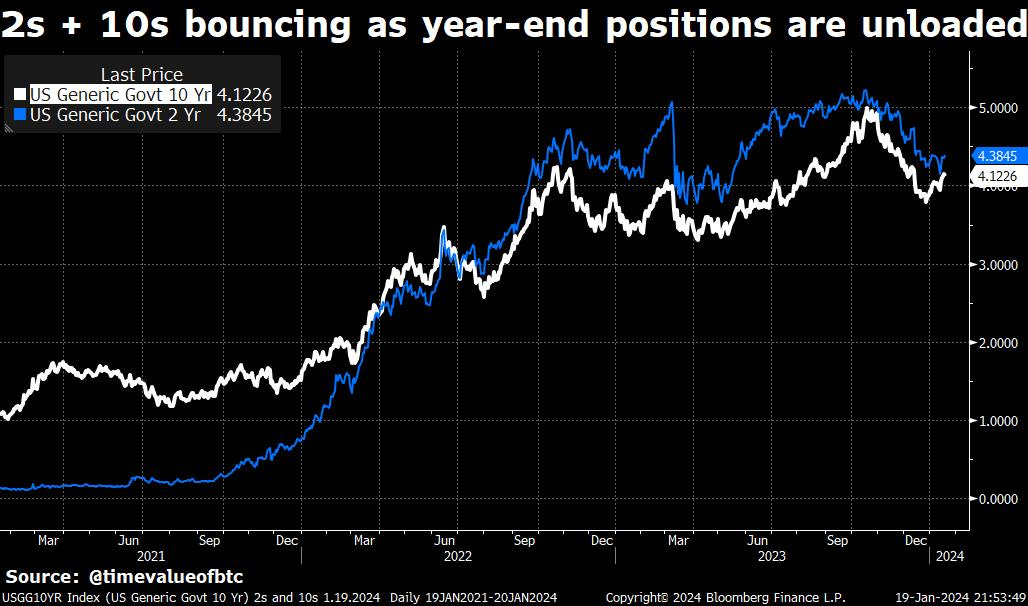

US Treasury yields bounced this week in a minor selloff, with 2s up 24 bps and 10s up 18 bps. It has little to do with policy or economic expectations though, in our view, and is more likely a result of institutions unloading their year-end Treasury allocations, as Nik explained in Thursday’s research post. The expectation for financial conditions to loosen remains intact, as indicated by Fed Funds futures and further confirmed by what we believe to be a cyclical downward trend in Treasury yields, at least in the front end of the curve:

Loan activity from US commercial banks suggests a return to normalcy. Having fallen from its pandemic-era credit expansion boom, total loans and leases outstanding have returned more or less to their long-run average without breaking below it. Perhaps this paired with anchored inflation expectations points to Powell’s move to forecast rate cuts as more prudent than premature, incorporating easing language as the plane’s landing is a little bit smoother. Still nowhere near blistering loan demand/supply:

On the other hand, in an absolutely baffling 2008-esque move, Powell and the powers that be seem to want to normalize banks with impaired balance sheets; or at the very least hide them among the healthy ones.

The US is preparing a rule that would force banks to tap the Fed’s discount window for emergency loans, even if they don't need one:

It is aimed to "reduce stigma and ensure lenders are ready for troubled times.” That stigma is how other banks know who to avoid, and it can stop balance sheet contagion and therefore limit bank failures. Readying lenders for troubled times is the other reason cited, but is using the discount window really so complicated that it requires all US financial institutions to take out a real loan each year, even when they don’t need it?

From the outside looking in, it seems that the Fed is attempting to normalize regular usage of the discount window so when times get rough and banks start using it because they’re in a liquidity crunch, it doesn’t seem as bad and gets buried in the billions of dollars in ‘fire-drill loans’ that are forced upon healthy banks. Considering the Fed’s measures to limit panic and stop bank runs in their tracks, burying embattled banks in a slew of others following standard procedural drills is curious and has our attention.

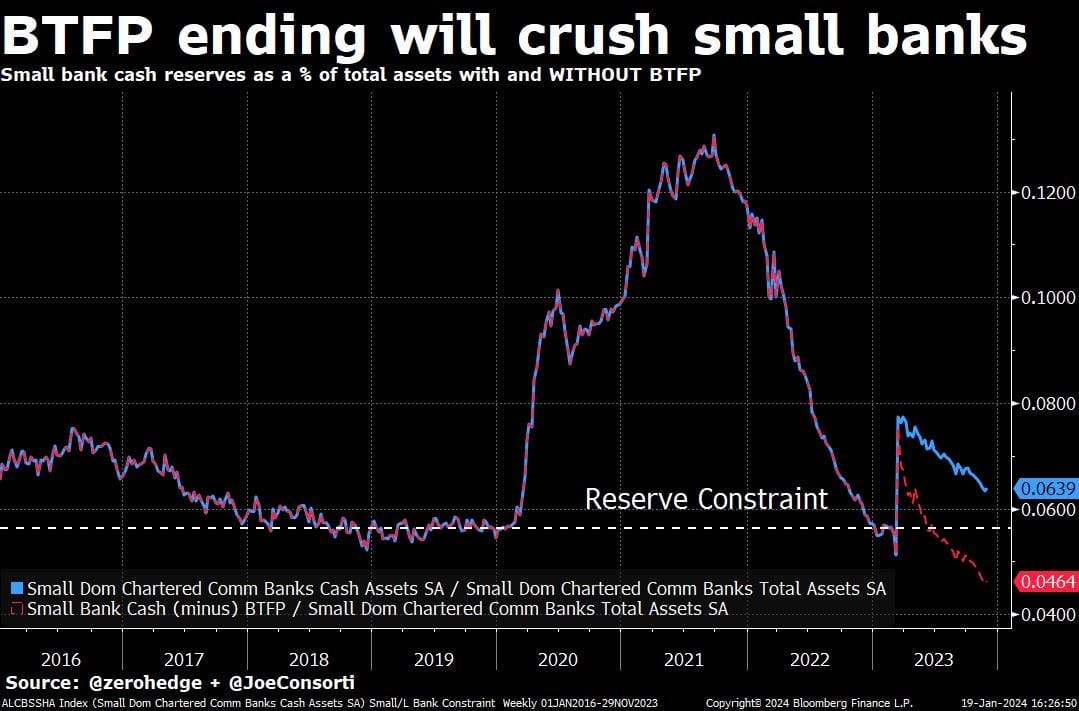

Won't this only lead to more recklessness in lending standards? Probably. The Fed has already given banks a sweetheart facility in BTFP, which is being abused and arbitraged by healthy banks looking to make money in the Fed’s overnight facilities. Total loans are accelerating, now at $161.5 billion this week:

Our longshot guess is when BTFP ends on March 11, 2024, the Fed is bracing for discount window usage, where troubled banks are not anonymous, to potentially rise substantially as poorly managed mid-size and small banks rush to it as their reserve constraint level is breached. Instead of letting banks avoid the junkies by knowing who they are, they're forcing everyone to take a hit. We are still waiting to see how BTFP loans are either extended, removed in favor of discount window loans, or eliminated without alternative:

As per usual, you don’t get access to these liquidity backstops. You will endure monetary tightening whether you like it or not, and there’s no central entity waiting at the ready to socialize your losses for you.

Next Week

In the week ahead, we will thankfully be in the middle of the Fed’s quiet period before its January 31st FOMC meeting. That means no jawboning for markets to digest—instead, there is plenty of economic data to chew on, including our first look at Q4 GDP, more housing data, and a very closely watched PCE inflation reading for December. Weak PCE prints, which have pushed rate cut expectations forward, are expected to continue and basically forecast 3-month inflation readings closer to 1% than 4%. Friday’s PCE number should be a market mover. We are basically looking to the money markets to see if cut dates are shifted around. Currently, the market expects no March rate cut, and we agree there. May and June are both leaning to the 50bp+ side of things, leading us to believe that’s when we’ll see the first reduction in policy rates. In order for that happen, the Fed must continue to hint at less restrictive policy on January 31st, including perhaps an indication that QT will become more mild. This would set the table for a March announcement of a May likely rate cut. For the week ahead, we’ll remain focused on how to balance weak business sentiment with strong consumer sentiment:

Treasuries will be auctioned in the front end of the curve next week and settle the following week into the market. Our newfound obsession with Treasury settlement days has to do with QT, reserve constraint, and repo rate instability. And to be completely honest, the obsession isn’t brand new—in 2019, when the Fed was unwinding its balance sheet before it created several trillion after the pandemic began, QT days (when the Fed’s balance sheet physically shrinks as securities mature such as the upcoming January 31st settlement date) would correspond with notable risk market activity. This will be a 2024 story as well, so we are doing our diligence by alerting you now. With the Fed telling us that QT must end early, we might be on to something.

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are some quick links to all the TBL content you may have missed this week:

Tuesday

When the dust clears after an extremely eventful week like the last, one in which several months’ worth of progress for bitcoin was jammed into Thursday and Friday alone, we like to take a step back and regain our bearings.

Today, we’re taking a look at liquidity, derivatives, volatility, and the GBTC fee arbitrage trade to get an accurate lay of the land as we head into the halving just three short months from now. We also end with a stern warning.

Check out—Spot Buying & Hoarding Dominate The Market Heading Into The Halving: Bitcoin Analysis

Wednesday

In this episode, we are joined by technology entrepreneur and author Jeff Booth to discover why bitcoin makes the world a better place. Jeff helps us through understanding why bitcoin is the only global solution to a broken money system, including providing a history of Internet protocols and explaining how government currencies steal our time.

Check out—Why Bitcoin Makes The World Better

Thursday

Investing is mostly about managing blind spots. That’s why the general tendency is to lean towards diversification: spreading money across assets and asset classes just in case something goes wrong with one. By nature, blind spots are not visible, making identifying them infinitely more difficult. Nevertheless, I believe we should be identifying what we think and what we don’t know—it helps us realize how little we actually do know about the future and provides the proper humility for making global macroeconomic and financial market prognostications. Today, we can offer some humble yet bold predictions, with a side of hedged language.

Check out—What I think & what I don’t know

Friday

In this episode, we are once again joined by Glassnode's lead on-chain analyst, Checkmate. He gives us a masterful overview of bitcoin markets heading into and post ETF approval, including a breakdown of the latest in futures and options market structure, what is happening on-chain with various cohorts of investors, and how to interpret all the data now available as bitcoin matures as an asset class.

Check out—Bitcoin DEEP DIVE: On-Chain, Futures & Options, and Market Dynamics

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.