$70,000 Bitcoin & Bad Employment Data: TBL Weekly #84

$70,000 Bitcoin & Bad Employment Data: TBL Weekly #84

The unemployment rate is rising in earnest as investors party like it's 1929.

Welcome to TBL Weekly #84—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.

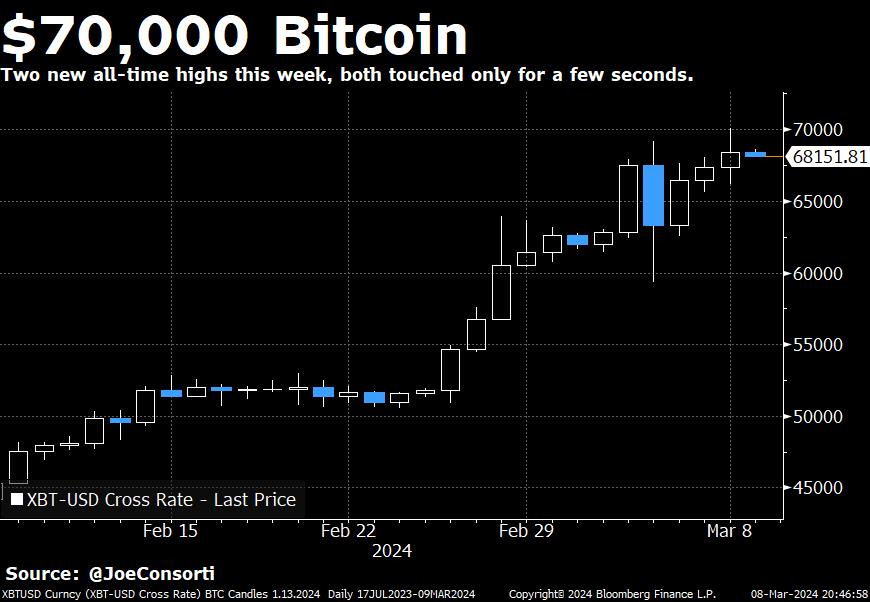

Good morning everybody, happy Saturday! Bitcoin briefly touched $70,000 on Friday after a failed run at it on Thursday, while Coinbase reportedly crashed both times that bitcoin’s price was at or around this level:

On the derivatives front, heightened activity is still present relative to historical averages, but that is to be expected for the beginnings of what is shaping up to be a raging bull market. There were $106.5 million in long futures liquidations in the past 24 hours, and there has also been a reduction of $900,000 in open futures contracts since bitcoin wicked up to $70k. Each of bitcoin’s all-time high breaks this week was fueled in part by leverage, which was subsequently wiped clean before moving higher in mostly spot-buying. This is exactly what we want to be seeing:

Outflows from Grayscale’s bitcoin trust have not slowed down as previously expected as GBTC has shed an average of ~$300 million in bitcoin every day for the past two trading weeks—bitcoin’s price performance despite this structural selling is remarkable. All 10 spot ETFs now have $54.8 billion in assets under management, with BlackRock’s iShares vehicle and Fidelity’s FBTC vehicle in the lead, the latter of which has had record-breaking days this week in terms of volume traded. Institutional interest in bitcoin continues to grow as its year-to-date and cyclical outperformance becomes too apparent to ignore. This cycle will undoubtedly draw in financial advisors who may have previously been on the fence as the demand for bitcoin grows from a niche interest into a serious allocation for large-scale players:

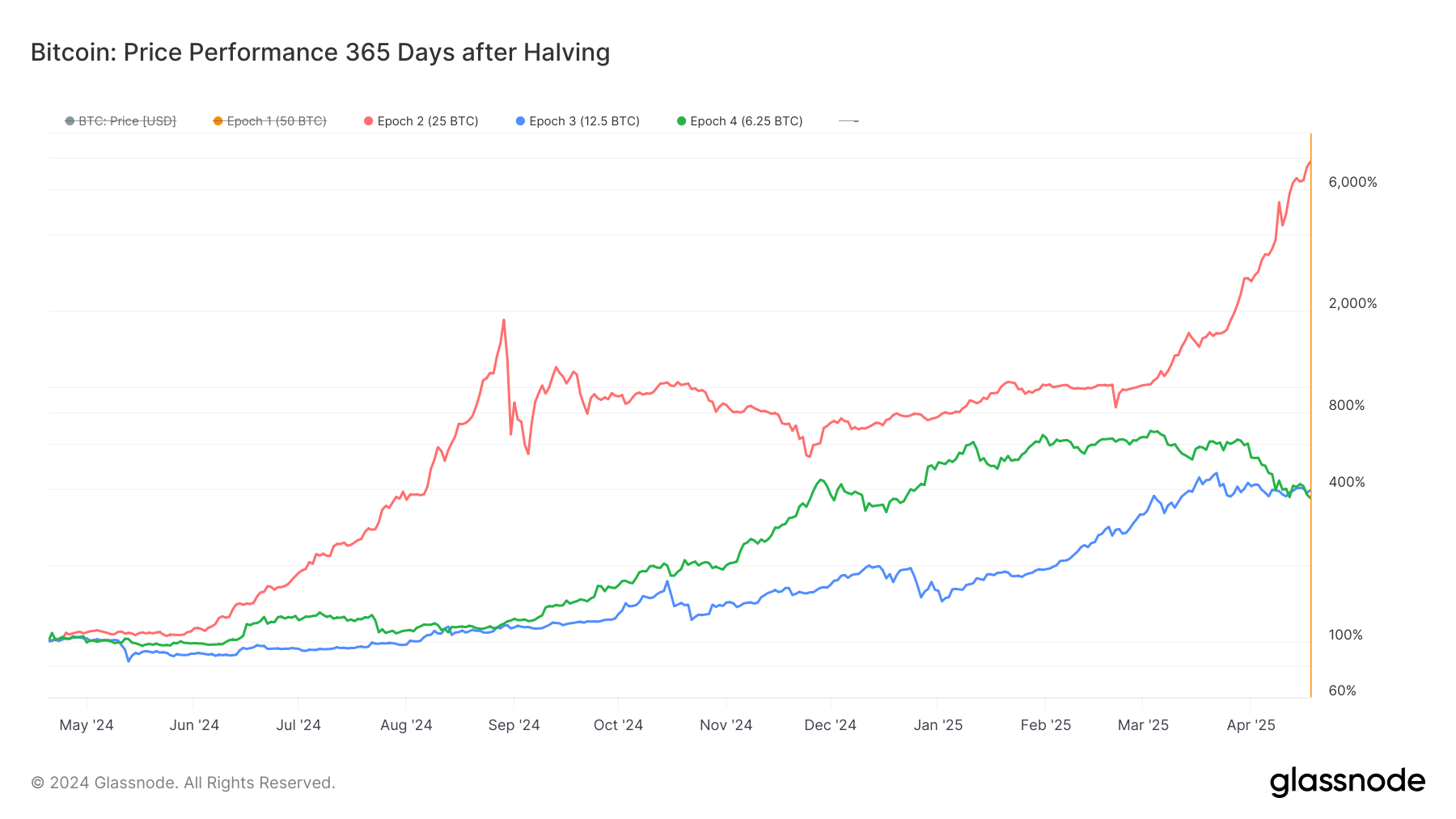

We continue to believe bitcoin stands to soar even more post-halving. In the year following bitcoin’s first, second, and third halving, it rose 7,745%, 393%, and 366% respectively. Ignoring the first epoch when bitcoin had a market capitalization lower than most penny stocks, if bitcoin were to rally 350% in its first year after the halving as it did in its second and third halvings, it would reach ~$315,000 by April of 2025. This is certainly not financial advice and not even a price prediction, but simply a fun thought experiment using prior cycles and extrapolating out into the near future:

It’s not only bitcoin on a recent tear, Wall Street has been in a raging bull market for several months. Despite what pundits expected, Powell’s 2-day remarks on Capitol Hill contained little to no hawkish commentary—some thought he would engage in an effort to cool off asset prices and aid his fight to tighten financial conditions given how highly he prioritizes the price level in setting monetary policy. He didn’t, meaning he likely feels that financial conditions will tighten soon enough on their own, without the need for him to ramp up the HawkTalk to encourage it.

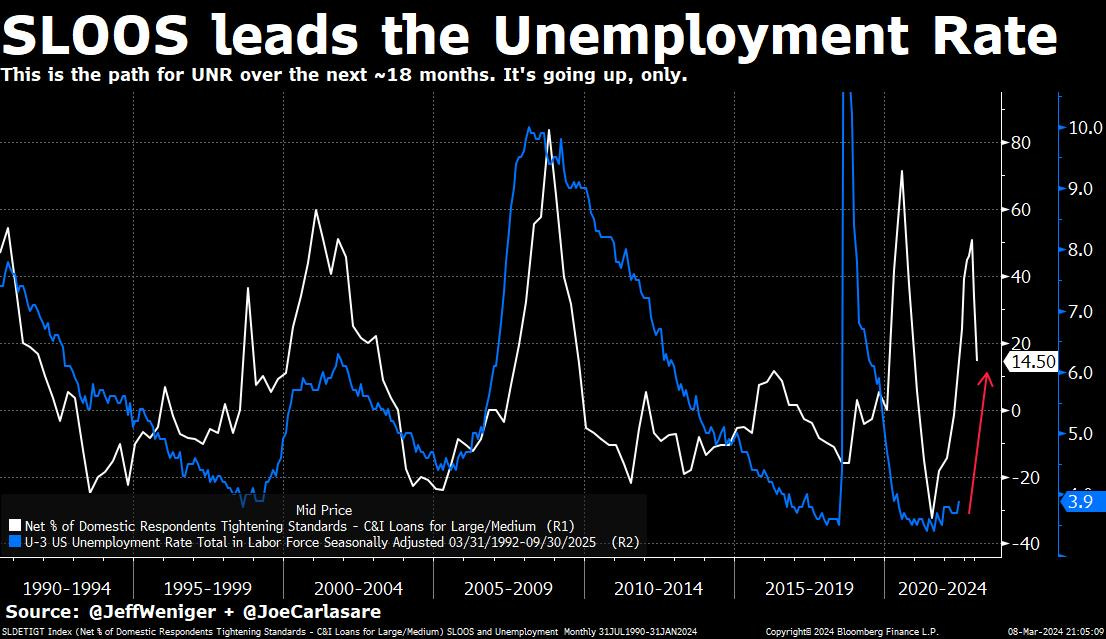

And he may be onto something if this is the case, as bad employment data on Friday foretells of the labor market finally starting to loosen. The unemployment rate rose to 3.9%, marking its highest level since January 2022 and the first material increase above the ~3.7% range since August of last year. Major firms have ramped up their layoff announcements, with Fidelity slated to cut 700 jobs in its first headcount reduction since 2017. Judging by past cycles, this looks like the beginning of the end for the labor market. Overlaying the senior loan officer’s survey for loan standards, set back by 18 months, with the unemployment rate there’s only one way this is going:

Payrolls were revised down by 140,000 jobs last month from 353k to 229k, keeping with and adding to the trend of 10 of the last 15 months' payroll reports being revised down after the fact—the propaganda has never been more in-your-face. We’ve discussed how a higher frequency of downward revisions relative to upward revisions is indicative of early-stage economic contraction, and that’s exactly what we’re seeing here. Market pricing for maintenance rate cuts from the Fed makes more sense as important labor market data continues to soften:

Congress passed a $460 billion funding package for government, adding to the horrendous fiscal situation Nik discussed on Thursday and Friday. Yet another assertion of fiscal dominance in the face of an increasingly floundering Fed, and a measure that certainly won’t help sticky price inflation fall back to target.

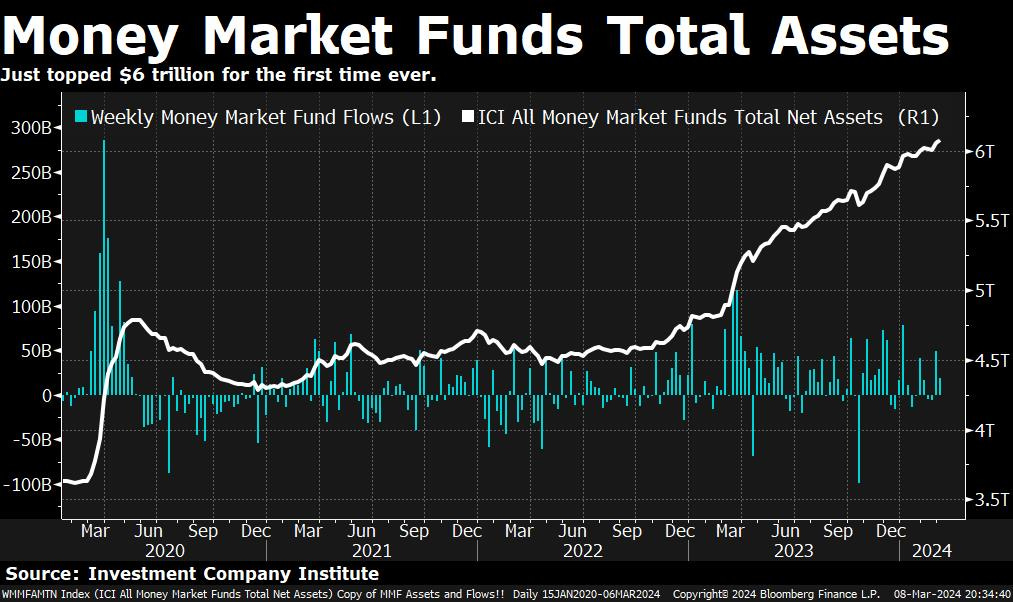

Investors are putting roughly $25 billion into money market funds every week providing a steady bid for US Treasury bills, but not nearly enough to meet all of the Treasury’s funding requirements:

With $444 billion remaining in the Fed’s overnight RRP facility, it is now a matter of weeks before the Treasury’s bill auctions will be a net liquidity drag on markets. The degree to which it acts as a headwind for the on-fire S&P 500 and the new kid on the block in bitcoin is still to be seen, but we will be watching and giving you the latest as it happens, as always.

Lastly for this week, we have regionals once again in crisis. NYCB, who acquired the failed Signature Bank last March, is facing failure; it was just revealed that the embattled bank was left off of the FDIC’s list of problem banks. With the Fed’s clearly behind the curve once again, what other embattled banks are they unaware of? This is the question lingering at the forefront of our minds as the Fed nonchalantly ends its BTFP emergency facility just two days from now—we hope everybody that needed it got a fresh 1-year term before the buzzer.

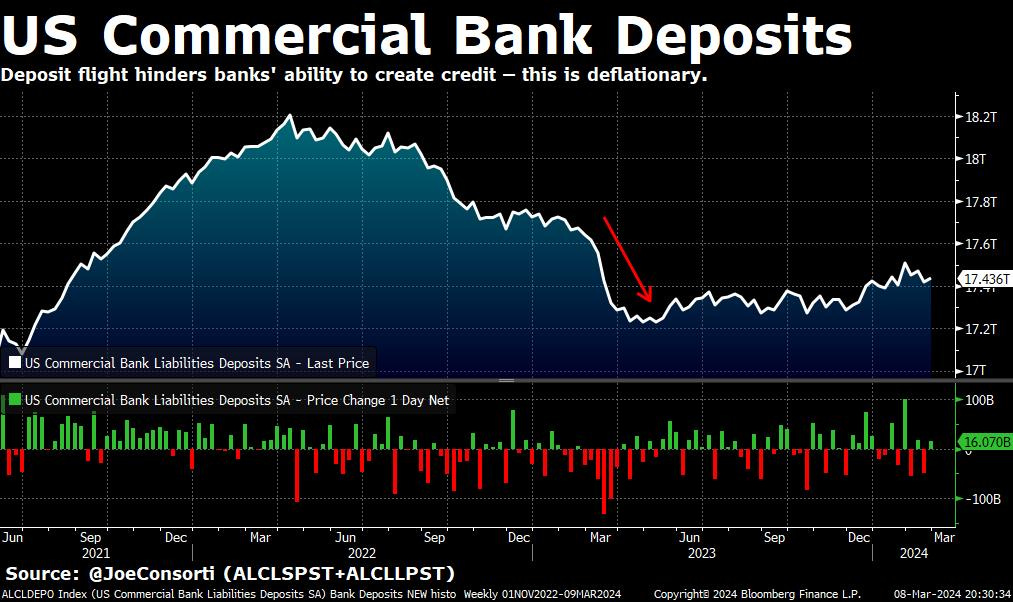

Deposits have not recovered their post-March 2023 crash outflows, making them all the more fragile in the face of bank runs, which we know now can happen overnight:

For a more detailed breakdown of the risks facing regional banks, check out our post here. We leave you with one final strike of this chart before BTFP ends on Monday, cash reserves at small banks as a % of total assets, with (blue) and without BTFP (red). As you can see, without BTFP, banks will be left without the sweetheart lifeline that kept them anonymously afloat for a full year:

Still, larger banks seem totally insulated from this event and markets seem to have mostly moved on, with JPMorgan’s stock soaring recently. If the price action during March 2023’s banking scare compared to now says anything, it’s that markets aren’t anticipating larger banks to be affected, if any material weakness comes about with regionals at all:

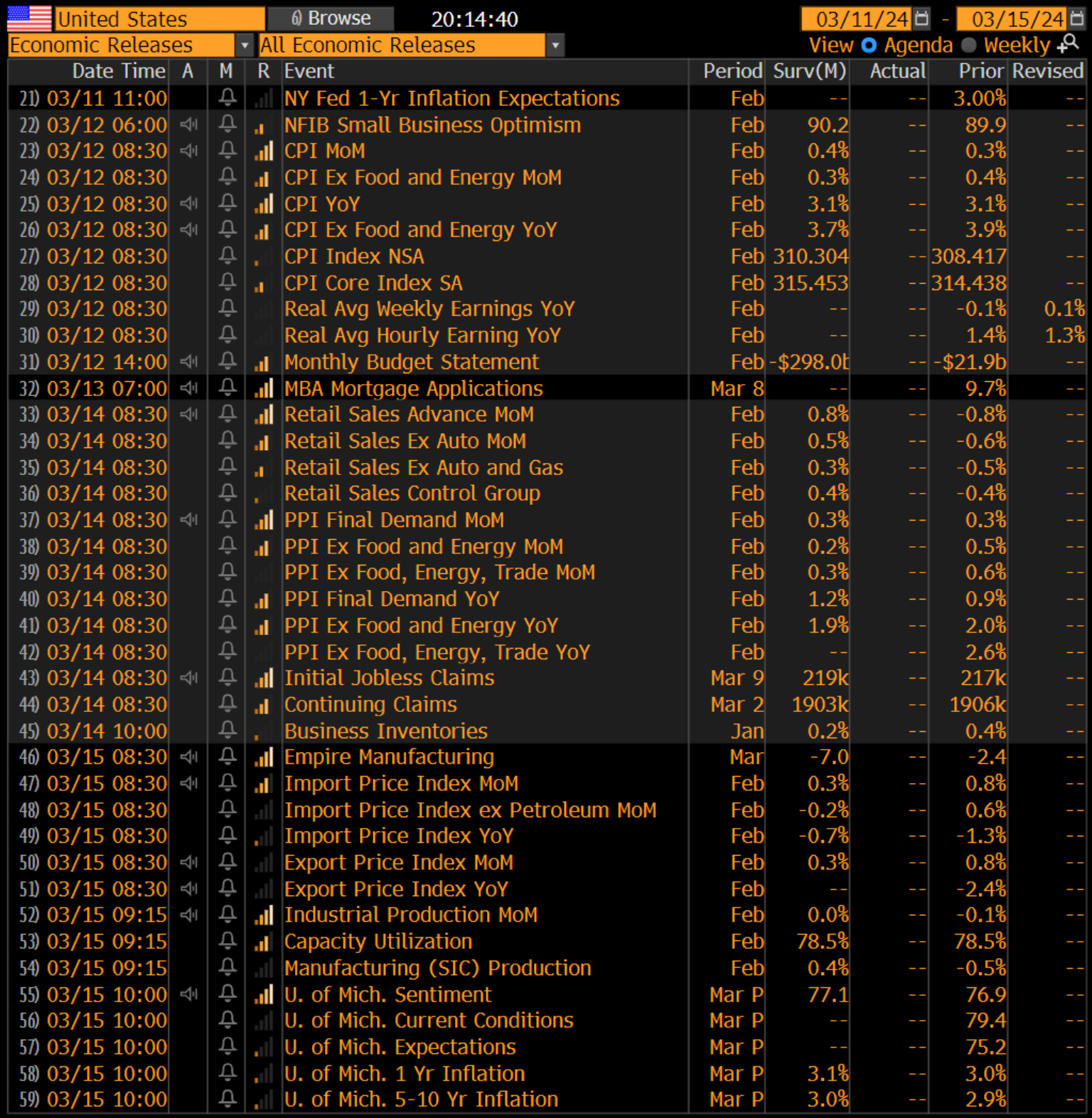

Next Week

In the week ahead, CPI inflation will grab the most headlines, but there are several noteworthy events to anticipate. Treasury investors will process CPI, PPI, and retail sales for February while taking down 3-, 10-, and 30-year notes and bonds in gargantuan size. More important for us than how the auctions go during the week is how they settle on Friday—with more and more Treasuries hitting the balance sheets of primary dealers, the amount of repo financing required increases, and with T-bills flooding the market and RRP running out at the same time, dealer funding is where we would look for any troubling signs. And the signs might be minuscule: a basis point or two higher in SOFR might be a tell. Settlement day on Friday also means a QT day, meaning more Treasuries for dealers and their customers in lieu of the Fed. Economic news might have most peoples’ attention, but the aspiring financial plumbers at The Bitcoin Layer have different ideas for the week of March 11th:

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops.

Here are some quick links to all the TBL content you may have missed this week:

Monday

In this episode, Nik is joined by real estate investor Kelly Lannan. Kelly breaks down the trouble brewing across the commercial real estate sector, including how new multifamily properties are unable to receive financing, existing properties are struggling to refinance due to reduced occupancy and higher rates, and whether the sector can survive until rates are lower in 2025. TSMC, Taiwan's semiconductor giant, and its new chip production facility in Arizona is also discussed.

Check out—TROUBLE BREWING In Commercial Real Estate

Tuesday

Paradox (noun) - a seemingly absurd or self-contradictory statement or proposition that when investigated or explained may prove to be well-founded or true.

A paradox is what markets have seemingly found themselves in during this cycle. All previous narratives constructed about market cycles have been violated in one way or another. Bank failures occurred mid-bull run, which persisted without a hitch. Every US stock index has breached new highs, corporate credit has not slowed down, and corporate earnings remain strong, all after the Fed increased its policy rate from ~0% to 5.5%. We’ve been calling for a Fed pause rally for the past 18 months now, but no honest investor predicted bitcoin would be inches away from blasting past its previous all-time highs after the Fed reached peak monetary tightness.

The contradictory apparent tightness of monetary policy yet extreme ease in financial markets has baffled many and likely left many portfolio managers severely underperforming after foolishly battering down the storm hatches for what turned out to be a sunny, cloud-free day. But is any of this contradictory? Not necessarily. We need to dive deeper into the fiscal side of affairs to understand why markets are behaving as they are, and when we do, uncover how this is just the beginning of what could prove to be a regime change in markets. The US fiscal train is barrelling down the tracks and the only entity that can sustain it is the one with the money printer.

Check out—

The 2024 Paradox: High Interest Rates & The Bitcoin & Tech Stock Boom

Wednesday

In this episode, Nik is joined by bitcoin researcher Jamie Coutts to discuss his thesis on nation states adopting bitcoin via domestic mining operations, including the United Arab Emirates (UAE). Jamie explains his bitcoin research process, including how he looks at perpetual futures funding markets, on-chain metrics, and ETF flows. Jamie has the Chartered Market Technician designation, a markets charter he shares with Nik. He previously built Bloomberg Intelligence's cryptocurrency research product and now is the Chief Crypto Analyst at Real Vision.

Check out—Nation States ADOPTING BITCOIN

Thursday

Have you been too bearish on the economy, expecting a recession to be right around every corner for the past couple of years? It’s ok to admit it—a year ago, when banks began failing, I couldn’t have imagined no recession would set in by now. In fact, I thought it was beginning at that moment. Over the past several months, however, it has become clear that the resilient US economy is instead super-extra-persistently resilient, and the reason is fiscal spending. Last year, readers insisted we read up on the 1940s and start admitting that restrictive interest rates are playing secondary to deficit spending.

As a researcher, I also admit to you today that I’ve been reading a healthy amount of financial research papers, listening to interviews with monetary experts, and overall sinking deeper into learning mode. Thankfully, I have an incredible data tool that allows me to convert my research into visualizations for you, the reader—today, we share updated views on fiscal dominance, inflation, and the monetary system, courtesy of a writer who is frankly just obsessed with trying to figure it out. Aren’t we all?

Check out—FREE POST: $10 trillion in cumulative deficits

Friday

In this episode, Nik breaks down the massive fiscal deficits of the US government over the past five years. We begin with comparing today's deficit historically, explain the numbers behind how the US has spent $10 trillion more than it has collected since 2020, and how this deficit has impacted financial markets and the economy. Nik discusses bitcoin's price increase to $70,000, the signal we are getting from realized price, and generally speaks to what we missed last year when forecasting a recession.

Check out—$10 TRILLION Deficit

Our videos are on major podcast platforms—take us with you on the go!

Apple Podcasts Spotify Fountain

Keep up with The Bitcoin Layer by following our social media!

YouTube Twitter LinkedIn Instagram TikTok

That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice.

Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients.

Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free.

Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin.

Thank you, Nik! 🙌🙏😊

Hey Nik / Joe - I’m struggling to understand Realized Price. I listening to one of Nik’s recent YouTube videos that highlighted the difference between the market/spot “Price” at exchanges whereas the Realized Price is marked by on-chain movement. What I’m struggling with - and perhaps other subscribers as well - is how Realized Price is vastly lower (~$26k as of this post) when compared to the spot Price (~$68k). Can you provide some clarity for those of us following along? 🙏🙏